LINK OF COUNTERPARTIES VIA MARKETS

As already mentioned, counterparties are linked to markets. This is important to remember because, in this case, counterparties are not only exposed directly to each other, but they are also exposed to markets.

The main markets that financial institutions consider for such analysis are the currencies and the region(s) where the counterparty is trading; moreover, to the stock, indices and commodities referring to counterparty's business sector.Obligors can be linked to each other via the underlying “systematic” market risk factors that they are exposed to, i.e., market index of the sector that they belong to. Thus, the correlation and volatility of the risk factors define the corresponding correlation and volatility of the regions and sectors and consequently of the linkages among obligors.

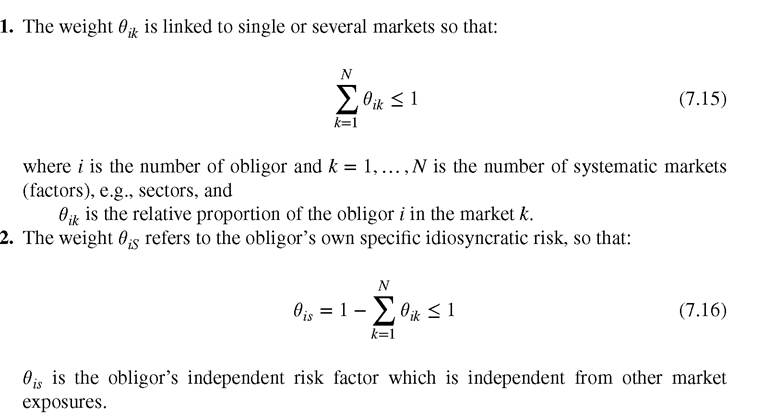

The set of k markets at time t and the associated risk factors must be defined. For example, a market could refer to a sector, e.g. tourism, which is associated with corresponding sector stock indices. As obligors are allocated (linked) to markets, a risk allocation weight θik of each obligor to the sector(s) must be defined.

There are two types of risk allocation weights:

Given the different possibilities for allocating the obligors to different market risk factors, one has to define their structure and weights. The assumption in such analysis is that markets have an influence on the performance of the participating obligors. This also drives the correlation8 of defaults between the obligors.

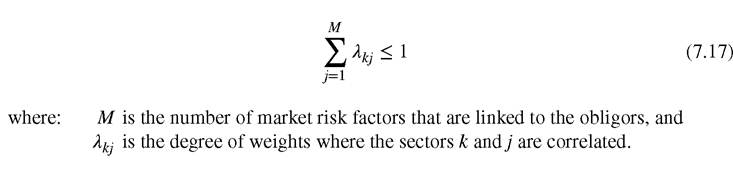

Markets that are linked to obligors can also be correlated. A general equation for defining such a correlation λ weight is:

The systematic markets (factors) can also be assumed independent (based on the applied model).

Note that a model employing correlated factors, e.g., indexes of the same sector and geographic factors, interest rates, etc., could be transformed into one that is using independent factors; this can be done simply by linear transformation.The performance of the markets can also be volatile. Such volatility σk can be defined via the volatility of the underlying market risk factors σk = aRF(k).

Based on market volatility the correlation volatility between the obligors and the allocated markets σθ can also be considered and defined; a simple approach is by considering the standard deviation of obligors, i weights θik to market volatility of σk, i.e.,

The evolution of the markets will also impact the correlation between the obligors (linked to these markets).

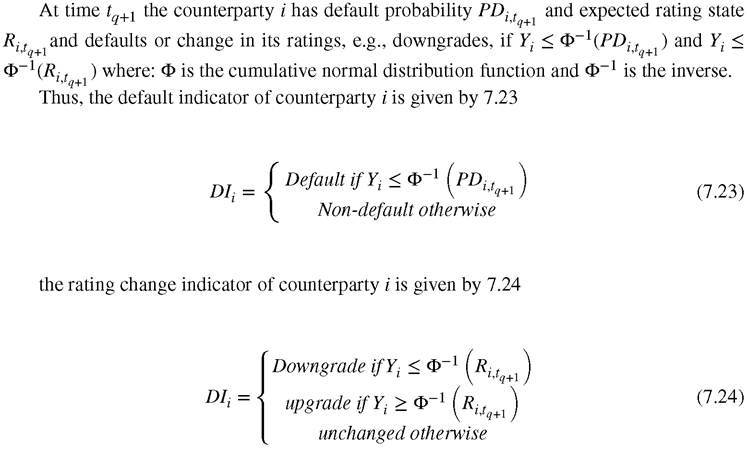

At given counterparty the default or creditworthiness index is defined in 7.19.

In the following paragraphs, we examine how we can allocate obligors to markets. This helps financial institutions to identify the correlation among counterparties.

Marketplace lending may also have as high a degree of complexity as the banking credit portfolios, in regards to counterparty links and correlations. For this reason, investors in peer- to-peer loans may underestimate the risk of loans, because this risk is uncertain and difficult to quantify. When we think about applying the analytics that banks use for their loans to marketplace loans, we will need to think along the same lines for counterparty exposure in marketplace lending to specific markets.

The practice of marketplace lending platforms to reduce all risk management to the scoring of borrowers, and the advice for lenders to diversify, is hardly doing justice to the complexity of the asset class.7.6.1 Allocating obligor to its own specific risk

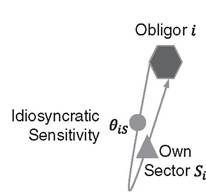

We may link obligors—or borrowers—to their own specific risk factors, such as to their own business. Thus, it is assumed that the fortunes of an obligor are affected by its own idiosyncratic factors specific to the obligor's characteristics, which are responsible for the possibility of the obligor's default rate. Although such a case is rather rare, it can exist for some counterparties; a typical example is Apple Inc. which has rather strong idiosyncratic specific risk characteristics that gives it a very low credit spread compared with other corporations in the IT sector. Even when other IT stocks perform badly, Apple has in the past outperformed. It seems to exist in its own universe with its own rules, which is to say that it has a high idiosyncratic sensitivity and a low sector sensitivity.

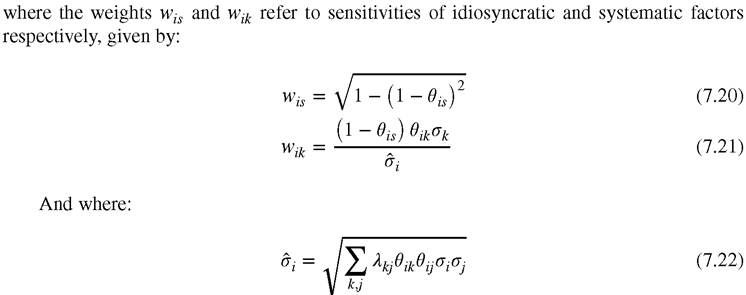

Such a model requires a market risk factor, i.e., spread, to identify the obligor's “idiosyncratic” i specific risk with a degree of weight θi0. Since such factor is driving the specific risk for a given obligor it affects that obligor only. Figure 7.4 shows such a model.

FIGURE 7.4 Allocating an obligor to own specific sector

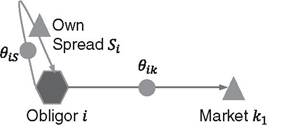

7.6.2 Allocating obligor to specific market

In such cases, the obligor i is allocated not only to its own specific risk but also to specific market sectors, and the underlying market risk factors. The degree of weights θik defines the sensitivity of the obligor to the market. Thus, the underlying factors of both its own specific sector and market k are responsible for the uncertainty of the obligor's default rate. Such allocation provides diversification benefit of obligors whose fortunes are affected by independent systematic factors.

Most counterparties fall into such allocations. For instance, most individuals and corporations belong to a specific region and corresponding currency. Figure 7.5 illustrates this case.

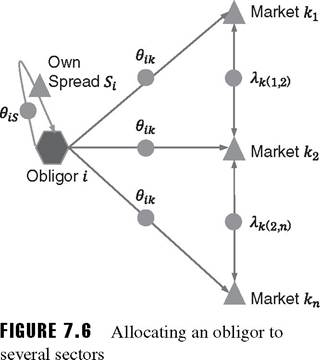

7.6.3 Apportioning obligors across several markets

In such cases, the obligor i is allocated to certain degree to several markets k with a degree of weights θik. Thus, it is assumed that on top of the factors referring to its own specific risk, a number of underlying market risk factors also affect an obligor. These factors can also be responsible for the obligor's default rate.

Markets may also be correlated to each other with a degree of certain weight λkj. High degree of λkj implies that the obligor has lower degree of allocation into the correlated markets. In many cases counterparties could be linked, e.g., operate, to more than one correlated regions/currencies, or/a sector, e.g., tourism and aviation sectors. Figure 7.6 depicts this sort of correlated relationships.

FIGURE 7.5 Allocating obligors to one or several sectors

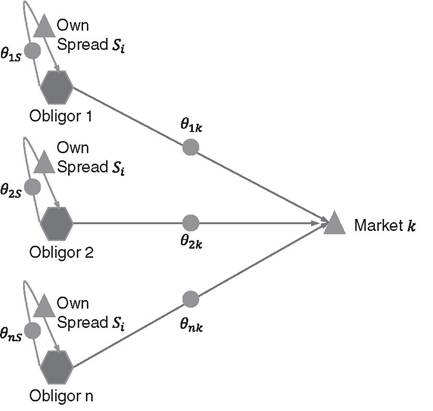

7.6.4 Allocating several obligors to a single market

This is the case where several obligors i = {1,2,..n} are allocated to a single market k with a degree of weights θik; thus, it is assumed that a single systematic factor affects the individual default rate of each obligor. In this case, a sector can be thought of as a collection of obligors having the common factor of being influenced by the same single systematic factor. A typical example is the fact that many obligors belong to the same region/currency or the same business sector.

Such allocations capture all of the concentration risk within the portfolio and exclude the diversification benefit of the fortunes of individual obligors being subject to a number of independent systematic risk factors.

It also generates a prudent estimate of extreme losses. Figure 7.7 shows these types of cases.7.6.5 Allocating obligors to several correlated markets

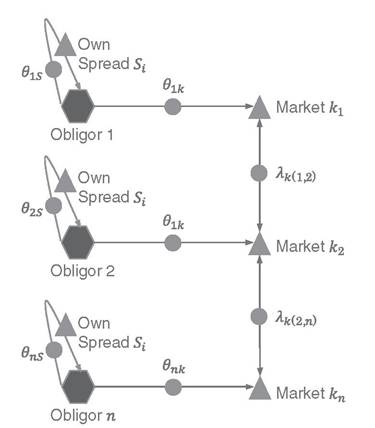

When obligors are allocated to several markets the possible correlation between the markets must be considered. Thus, as illustrated in Figure 7.8, a degree of weights between the market correlations should also be defined. In fact such a correlation is defined by considering the correlation of the market's underlying (market) risk factors. Thus, the correlation of obligors' default probabilities is identified by considering a) the degree of weights θik where obligor i is allocated to one of several sectors k and b) the degree of weights λ(α b)k where the sectors a and b are correlated.

This type of allocation is the most challenging as both degrees of weights θik and λ(α b)k need to be considered.

The above allocations' analyses are the basis for identifying the correlations among counterparties who are linked to specific and/or correlated markets. They are also significant in systemic and concentration risk analysis discussed in Chapter 11. In addition, they are applied in stochastic credit risk measurements, i.e., Credit VaR approaches. Concentration and systemic risks are big unresolved issues in marketplace lending where many borrowers and lenders connect to each other directly. It is very difficult to keep an eye on such risks when it is

FIGURE 7.7 Allocating all obligors to a common single sector

unclear how individual counterparties are directly and/or indirectly linked to each other. At the same time, because the loan market in marketplace lending is nascent, it might be possible to collect enough information about individual exposures directly from platforms to understand concentration risk better. More research in this area is still necessary.

FIGURE 7.8 Allocating obligors to several markets that are correlated to a degree of weights λ

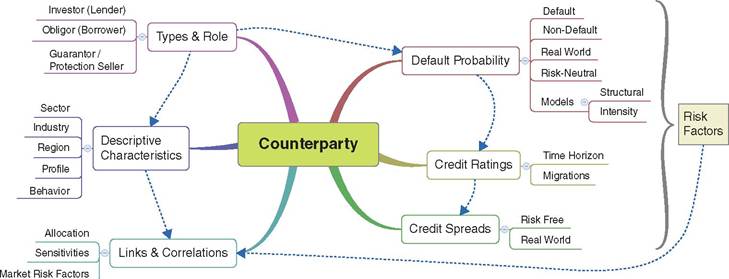

FIGURE 7.9 Main detailed elements considered in counterparty risk analysis

7.6