Mathematical tools for finance

The purpose of this section is to explain essential mathematical skills that will enhance understanding of finance. The author has no love of mathematics for its own sake and so only those techniques of direct relevance to the subject matter of this book are covered.

When there are time delays between receipts and payments of financial sums we need to make use of the concepts of simple and compound interest.

Simple interest

Interest is paid only on the original principal. No interest is paid on the accumulated interest payments.

Example 12.1

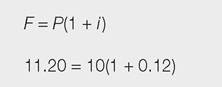

Suppose that a sum of £10 is deposited in a bank account that pays 12% per annum. At the end of year 1 the investor has £11.20 in the account. That is:

where F = Future value (or terminal value), P = Present value, i = Interest rate.

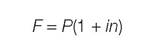

The initial sum, called the principal, is multiplied by the interest rate to give the annual return. At the end of five years:

where n = number of years. Thus,

Note from the example that the 12% return is a constant amount each year. Interest is not earned on the interest already accumulated from previous years.

Compound interest

The more usual situation in the real world is for interest to be paid on the sum that accumulates - whether or not that sum comes from the principal or from the interest received in previous periods.

Example 12.2

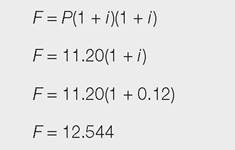

An investment of £10 is made at an interest rate of 12% with the interest being compounded. In one year the capital will grow by 12% to £11.20. In the second year the capital will grow by 12%, but this time the growth will be on the accumulated value of £11.20 and thus will amount to an extra £1.34.

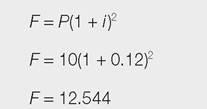

At the end of two years:

Alternatively,

Over five years the result is:

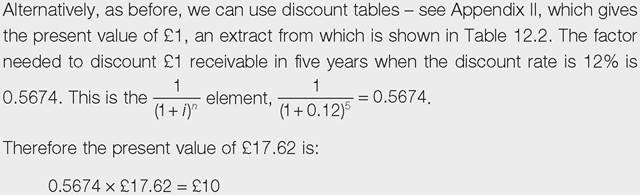

While these calculations are not overly difficult, they can become cumbersome and time consuming, requiring the use of a calculator and accurate pressing of buttons. It is common practice to use tables for the solution. Table 12.1 shows an extract from Appendix I to this chapter, which gives the future value of £1 invested at a number of different interest rates and for alternative numbers of years.

This gives the results we have worked out above. From the second row of the table in Table 12.1 we can read that £1 invested for two years at 12% amounts to £1.2544. Thus, the investment of £10 provides a future capital sum 1.2544 times the original amount:

and from the fifth row, the investment of £10 after five years provides a future capital sum 1.7623 times the original amount:

Table 12.1 The future value of £1

| Year | Interest rate (per cent per annum) | ||||

| 1 | 2 | 5 | 12 | 15 | |

| 1 | 1.0100 | 1.0200 | 1.0500 | 1.1200 | 1.1500 |

| 2 | 1.0201 | 1.0404 | 1.1025 | 1.2544 | 1.3225 |

| 3 | 1.0303 | 1.0612 | 1.1576 | 1.4049 | 1.5209 |

| 4 | 1.0406 | 1.0824 | 1.2155 | 1.5735 | 1.7490 |

| 5 | 1.0510 | 1.1041 | 1.2763 | 1.7623 | 2.0114 |

The interest on the accumulated interest over five years is therefore the difference between the total arising from simple interest and that from compound interest:

£17.62 - £16.00 = £1.62

Present values

There are many occasions when you are given the future sums and need to find out what those future sums are worth in present-value terms today.

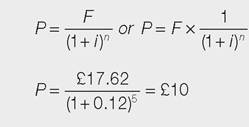

For example, you wish to know how much you would have to put aside today that will accumulate, with compounded interest, to a defined sum in the future; or you are given the choice between receiving £200 in five years or £100 now and wish to know which is the better option, given anticipated interest rates; or a bond gives a return of £1 million in three years for an outlay of £800,000 now and you need to establish whether this is the best use of the £800,000. By means of a discount calculation, a sum of money to be received in the future is given a monetary value today.Example 12.3

If we anticipate the receipt of £17.62 in five years' time we can determine its present value. Rearrangement of the compound interest formula, and assuming a discount (interest) rate of 12%, gives:

Table 12.2 The present value of £1

| Interest/discount rate (per cent per annum) | |||||||

| 1 | 5 | 10 | 12 | 15 | 17 | ||

| Periods | 1 | 0.9901 | 0.9524 | 0.9091 | 0.8929 | 0.8696 | 0.8547 |

| 2 | 0.9803 | 0.9070 | 0.8264 | 0.7972 | 0.7561 | 0.7305 | |

| 3 | 0.9706 | 0.8638 | 0.7513 | 0.7118 | 0.6575 | 0.6244 | |

| 4 | 0.9610 | 0.8227 | 0.6830 | 0.6355 | 0.5718 | 0.5337 | |

| 5 | 0.9515 | 0.7835 | 0.6209 | 0.5674 | 0.4972 | 0.4561 | |

| 20 | 0.8195 | 0.3769 | 0.1486 | 0.1037 | 0.0611 | 0.0433 | |

Examining the present value of £1 in Table 12.2 you can see that as the discount rate increases, the present value goes down.

Also, the further into the future the money is to be received, the less valuable it is in today's terms. Distant cash flows discounted at a high rate have a small present value; for instance, £1,000 receivable in 20 years when the discount rate is 17% has a present value of £43.30 (£1,000 ? 0.0433). Viewed from another angle, if you invested £43.30 for 20 years it would accumulate to £1,000 if interest compounds at 17%.Determining the rate of interest

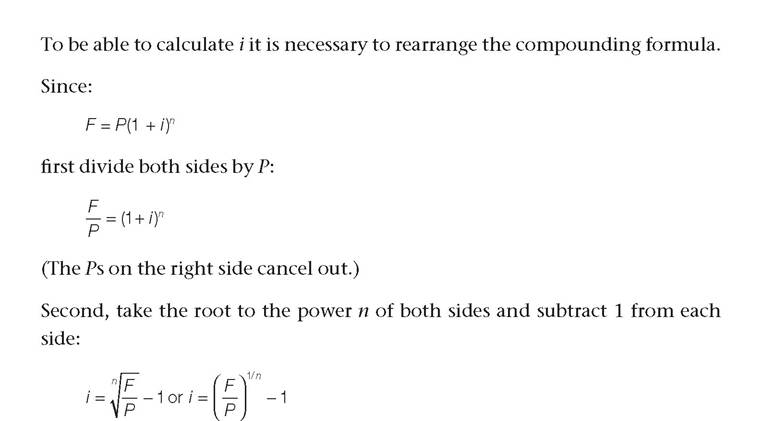

Sometimes you wish to calculate the rate of return that a project is earning. For instance, a bond may offer to pay you £10,000 in five years if you deposit £8,000 now, when interest rates on similar bonds are offering 6% per annum. In order to make a comparison you need to know the annual rate being offered. Thus, we need to find i in the discounting equation.

Example 12.4

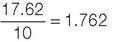

In the case of a five-year investment requiring an outlay of £10 and having a future value of £17.62 the rate of return is:

The rate of interest being offered by the bond mentioned above is:

A more straightforward alternative is to use the future value table (Appendix I), an extract of which is shown in Table 12.1. In our example, if the return on £10 is £17.62, then the return on £1 worth of investment over five years is:

In the body of the future value table look at the year 5 row for a future value of 1.762.

Read off the interest rate of 12%.

Annuities

In financial calculations, quite often there is not just one payment at the end of a certain number of years, there can be a series of identical payments made over a period of years.

For instance:• bonds usually pay a regular rate of interest

• individuals can buy, from savings plan companies, the right to receive a number of identical payments over a number of years

• a business might invest in a project which, it is estimated, will give regular cash inflows over a period of years

• a typical house mortgage is an annuity.

An annuity is a series of payments or receipts of equal amounts. We are able to calculate the present value of this set of payments.

Example 12.5

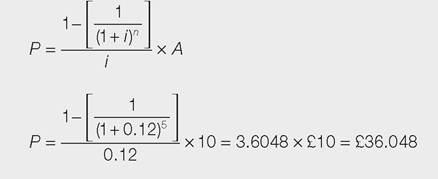

For a regular payment of £10 per year for five years, when the interest rate is 12%, we can calculate the present value of the annuity (P) by three methods.

Method 1

where A = the periodic receipt.

Method 2

Using the derived formula:

Table 12.3 The present value of an annuity of £1 per annum

| Year | Interest rate (per cent per annum) | ||||

| 1 | 5 | 10 | 12 | 15 | |

| 1 | 0.9901 | 0.9524 | 0.9091 | 0.8929 | 0.8696 |

| 2 | 1.9704 | 1.8594 | 1.7355 | 1.6901 | 1.6257 |

| 3 | 2.9410 | 2.7232 | 2.4869 | 2.4018 | 2.2832 |

| 4 | 3.9020 | 3.5460 | 3.1699 | 3.0373 | 2.8550 |

| 5 | 4.8534 | 4.3295 | 3.7908 | 3.6048 | 3.3522 |

Method 3

It is useful to understand Methods 1 and 2, but the calculations can be prolonged. Method 3 is recommended, where the relevant figures are looked up using the ‘present value of an annuity' table.

Table 12.3 is an extract from the more complete annuity table in Appendix III. Here we simply look along the year 5 row and 12% column to find the figure of 3.6048. This is the present value of five future annual receipts of £1. Therefore we multiply by £10:3.6048 ? £10 = £36.048

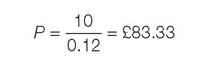

Perpetuities

Some contracts run indefinitely and there is no end to a series of identical payments. Certain government securities do not have an end date; that is, the amount paid when the bond was purchased by the lender will never be repaid, only interest payments are made. For example, the UK government issued consolidated stocks many years ago which may never be redeemed.

Perpetuities are annuities that continue indefinitely. The value of a perpetuity is simply the annual amount received divided by the interest rate when the latter is expressed as a decimal.

If £10 is to be received as an indefinite annual payment then the present value, at a discount rate of 12%, is:

It is very important to note that in order to use this formula we are assuming that the first payment arises 365 days after the time at which we are standing (the present time or time zero).

Discounting semi-annually, monthly and daily

Sometimes financial transactions take place on the basis that interest will be calculated more frequently than once a year. For instance, if a bond paid 12% nominal return per year but credited 6% after half a year, in the second half of the year interest could be earned on the interest credited after the first six months. This will mean that the true annual rate of interest will be greater than 12%. The greater the frequency with which interest is earned, the higher the future value of the investment.

Example 12.6

If you put £10 in a bank account earning 12% per annum then your return after one year is:

If the interest is compounded semi-annually (at a nominal annual rate of 12%):

In Example 12.6 the difference between annual compounding and semi-annual compounding is an extra 3.6p. After six months the bank credits the account with 60p in interest so that in the following six months the investor earns 6% on £10.60. If the interest is compounded quarterly:

Daily compounding:

Example 12.7

If £10 is deposited in a bank account that compounds interest quarterly and the nominal return per year is 12%, how much will be in the account after eight years?

Continuous compounding

If the compounding frequency is taken to the limit we say that there is continuous compounding. When the number of compounding periods approaches infinity the future value is found by F = Pein where e is the value of the exponential function. This is set as 2.71828 (to five decimal places, as shown on a scientific calculator).1

So, the future value of £10 deposited in a bank paying 12% nominal compounded continuously after eight years is:

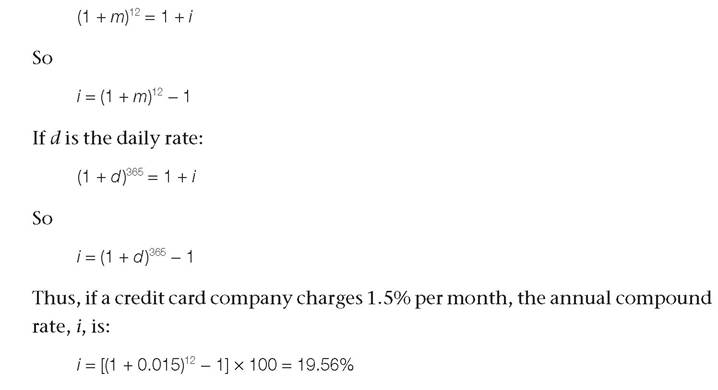

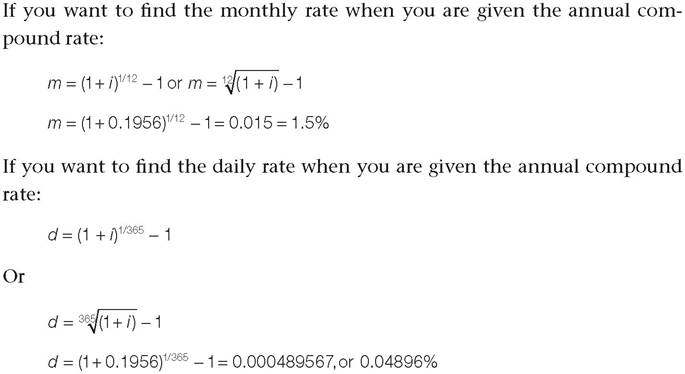

Converting monthly and daily rates to annual rates

Sometimes you are presented with a monthly or daily rate of interest and wish to know what is its equivalent in terms of annual compound rate (or effective annual rate (EAR)).

If m is the monthly interest or discount rate and i is the annual compound rate, then over 12 months:  [26]

[26]

More on the topic Mathematical tools for finance:

- Taking Stock

- This part of the book focuses on stochastic growth models and provides a brief introduction to basic tools of stochastic dynamic optimization.

- Taking Stock

- This part of the book is a preparation for what is going to come next. In some sense, it can be viewed as the “preliminaries” for the rest of the book.

- Nature11

- Final Remarks

- This part of the book is a preparation for what is going to come next.

- Some Difficulties of Contemporary Structuralism

- THE NEED FOR A METAPHYSICAL THEORY OF CAUSALITY

- Applications of Logic