Modeling People’s Bank of China Policymaking

The People’s Bank’s focus on money supply growth begs the question of exactly what role money supply movements have played in the Chinese

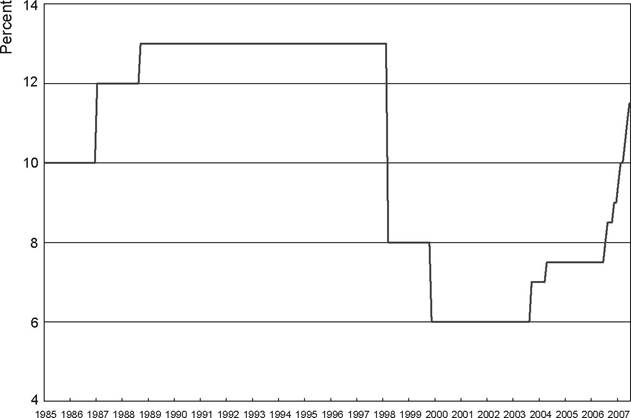

Figure 4.1.

People's Bank Required Reserve Ratios, 1985-2007. Source: Great China Database.economy in recent years. The existing evidence on this point is mixed. For example, while Sun and Ma (2004) and Zhang and Wan (2004) each identify a link between money movements and the price level, there is some ambiguity as to whether prices respond to money supply changes or, rather, monetary policy simply accommodates existing price trends - whereby it is price movements that drive money supply movements rather than the other way around.[63] However, a consistent, long-run response of inflation to different rates of monetary expansion over the 1990-2004 period is identified by Gerlach and Kong (2005).[64] In addition, Zhang and Wan (2004), while finding a key role for price expectations in influencing money, prices, and output alike, point to greater stability in the relationship between M2 (the aggregate emphasized by the People’s Bank) and both output and prices in China. They also find evidence of a long-term, cointegrating relationship among M2, prices, and output.

Potential structural breaks pose an additional complication, though. Even restricting attention to just the 1990-2002 period, Sun and Ma (2004) find that the effect of the different monetary aggregates (monetary base, M1 and M2) on prices disappears after the onset of deflation in 1998. This deflation, emerging in the midst of the Asian financial crisis, was, in fact, accompanied by a marked acceleration in savings growth relative to consumption (see Xu, 2002). The decline in the consumer price index was itself driven by a sharp drop in food prices that averaged -3.2% in 1998 and -4.2% in 1999 (Wu, 2004, p.

37). Elimination of tariffs as China joined the World Trade Organization (WTO) may also have extended the deflationary trend, as well as helping to account for the fact that wholesale prices dropped so much more than consumer prices in 2001-2002 (Dai, 2002). Meanwhile, the People’s Bank’s scope for expanding the rate of monetary expansion to ward off deflation was limited by the need to simultaneously offset downward pressure on the renminbi (Chapter 1). Supporting the currency meant selling dollars and buying renminbi, thereby tending to reduce the domestic money supply at the very time when output and price conditions would normally have called for more expansionary policy.In the empirical work discussed later, this chapter seeks to capture People’s Bank policy responses over the 1990-2006 period that surrounds the 1998-2002 deflationary episode. By far the most popular way of capturing central bank policymaking in recent years has been through estimation of the “Taylor rule” (Taylor, 1993). This approach, which appeared to be an especially good fit with US Federal Reserve policy during the Alan Greenspan era, explains central bank interest-rate setting as a function of the gap between inflation and its target value and the gap between actual real output and its potential level. Countercyclical policy suggests that the central bank will raise rates when either inflation or real output rises above target so as to cool the economy off and help move the future realizations of these variables downward. However, lack of flexibility in interest rates poses potential problems for the Taylor rule. When interest rates are already very low, falling inflation and/or output levels may well leave the Taylor rule calling for negative interest rates that cannot be delivered in practice. Moreover, in situations like mainland China, where interest rate liberalization remains incomplete, interest rates may simply not be a meaningful target variable.[65] Nor are interest rates an actual target variable in China’s case.

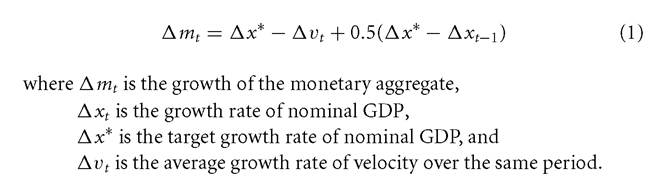

McCallum’s (1988) alternative rule, under which movements in a monetary aggregate represent the central bank’s policy variable, is therefore almost certainly more applicable to China. McCallum’s original formulation expressed monetary base growth as a function of nominal output (that is, the product of real output and the price level) and velocity growth. Given that the People’s Bank has often emphasized M2 growth rates, M2 is entered as a dependent variable in the ensuing empirical work in addition to the monetary base series originally suggested by McCallum (1988). A velocity term is included in the specification so as to allow money supply growth to adjust upward in the face of the rising money demand implied by declining velocity of circulation. Otherwise, excess money demand would put upward pressure on interest rates and likely exert deflationary effects on the economy. Such monetary expansion would not be inflationary as the central bank would simply be providing people with the extra money they want to hold and, insofar as money supply and money demand grow together, there would be no extra spending pressure. Finally, in the event that nominal output growth is exactly on target and velocity is constant, the rule allows for a benchmark monetary expansion that is one-for-one with the target growth rate of nominal output. This essentially yields Friedman’s famous x% rule for monetary policy modified to allow for responses to persistent velocity movements and deviations from the (presumed sustainable) target rate of output growth.

With nominal GDP as the output measure, the basic McCallum rule has the following form:

In applying the McCallum rule to China, we augment the specification to allow for People’s Bank responses to growth in foreign exchange reserves and the real exchange rate of the renminbi as well as a possible shift in policy following the onset of the Asian financial crisis and initial deflationary pressures. Just as the surge in M2 growth to nearly 20% in 2003 drew attention to the potential importance of exchange rate movements and reserve inflows, these same factors (in reverse) may have been important

contributors to deflationary pressures in the late 1990s.11 Meanwhile, even though we cannot fully account for such “structural” factors as WTO accession, our allowance for a parameter shift after 1997 shows this particular effect to be highly significant.[66] [67] We assess People’s Bank policy over the 1990-2006 period, thereby including the 1993-1994 inflation spike, the subsequent anti-inflationary policy, the attempts to reflate the economy after the 1997-1998 Asian financial crisis, the more recent pressures for renminbi appreciation that emerged after 2001, and the first year of the new exchange rate regime announced in July 2005.