Most governments issue bonds in their domestic currency to raise money when their tax receipts are less than their expenditure.

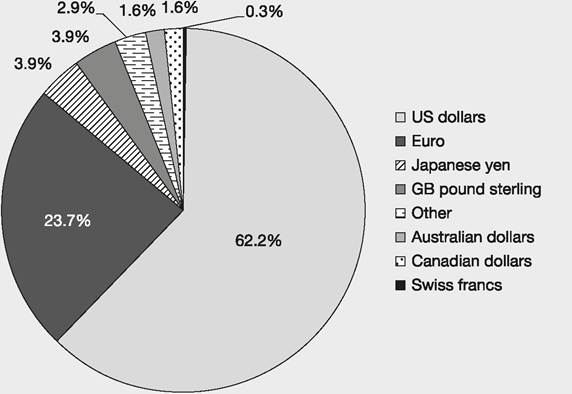

There is a robust international market for these bonds when the national currency is strong and stable, such as the currencies in Figure 2.1; this data from the International Monetary Fund (IMF) shows the percentage of foreign currencies kept in reserve by 144 reporting countries.[4] These currencies are known as hard currencies, that is, they are from countries where there is relative economic and political stability and the currencies are widely accepted in payment for goods or services.

If the national currency is unstable or weak for whatever reason the government may be able to issue bonds denominated in a foreign hard currency, usually the US dollar. This makes them more attractive to investors because they are viewed as less risky than domestic currency bonds because the government is committed to paying interest and principal in, say, the US dollar, regardless of inflation or exchange rate movement in that country. Bonds issued by a government either in the country's own currency or in another currency are usually known as sovereign bonds.

Following the round of financial crises, most governments have had to issue more bonds to permit deficit spending (i.e. not raising enough in taxes to cover outgoings to boost the economy). Statistics from The Economist from a range of countries show the enormous amount of debt some countries

Figure 2.1 Currency composition of foreign exchange reserves 2013

Source: Data from www.imf.org

owe - see Figure 2.2. For every person in Italy, the government owes more than $39,000. It is even worse in Japan, where the government owes over $98,000 per person. In both cases the debt is mostly bought domestically rather than lent by foreigners, and so the risk of a foreign lenders' strike or a major outflow of interest payments is less worrisome.

Nevertheless, that is an awful lot of borrowing.Bonds issued by reputable governments are the most secure (least risky) in the world because they are very aware of the need to maintain a good reputation for paying their debts on time. Furthermore, for countries able to issue in their own currencies, should there be a cash flow difficulty, they are able to print more money or to raise taxes, to ensure they have the means to pay the bonds' coupons or the bonds' redemption value. But if money creation is taken too far, raised inflation may be the result, putting off potential lenders in that currency.

We first look at the UK government bond market to get a feel for the workings of these markets and then, in Chapter 3, consider the US, French, German, Japanese, Chinese and emerging (underdeveloped) government bond markets.

| Canada total: $1,633bn Per person: $46,498 | UK total: $2,525bn Per person: $39,691 | Sweden total: $194bn Per person: $20,067 |

| Russia total: $202bn Per person: $1,436 | Netherlands total: $579bn Per person: $34,386 | Denmark total: $150bn Per person: $26,476 |

| Japan total: $12,331 bn Per person: $98,246 | USA total: $13,646bn Per person: $43,049 | France total: $2,423bn Per person: $37,801 |

| Germany total: $2,794bn Per person: $34,212 | China total: $1,624bn Per person: $1,212 | Spain total: $1,067bn Per person: $22,906 |

| Italy total: $2,405bn Per person: $39,289 | Malaysia total: $21Obn Per person: $7,158 | Portugal total: $279bn Per person: $26,101 |

| India total: $1,267bn Per person: $1,024 | Brazil total: $1,576bn Per person: $8,007 | Australia total: $398bn Per person: $17,038 |

| Chile total: $23bn Per person: $1,332 | Argentina total: $194bn Per person: $4,652 | N Zealand total: $76bn Per person: $16,557 |

| Global total: $53,503bn Per person: $7,643 | ||

Figure 2.2 Total public debt for a selection of countries: total amount outstanding in $USbn