UK gilts

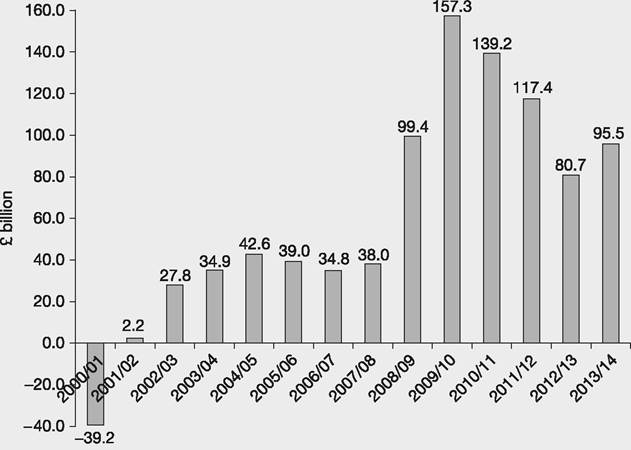

In most years, in common with other countries in the world, the British government does not raise enough in taxes to cover its expenditure - see Figure 2.3, which shows the amount the UK public sector (central and local government) had to borrow between 2000 and 2014 to make up this deficit and to maintain stability and restore confidence.

Note the significant rise following the 2008 financial crisis as the government borrowed to cover falling tax receipts, boost aggregate demand and bail out the banks.In addition to these ‘net borrowing' amounts the UK government issues new debt instruments to raise money simply to repay old debts that become due. Thus, the gross borrowing (gross issuance) is actually much larger - of the order of an extra £50-60 billion per year.

Figure 2.3 UK public sector (central and local government) net borrowing 2000-2014 (the difference between expenditure and revenue)

Source: ONS Public Sector Finances, March 2014 www.ons.gov.uk/ons/dcp171778_360531.pdf

While most of the gap between UK government receipts and expenditure is covered by selling bonds to investors, the government may also borrow via its National Savings and Investments arm, such as through premium bonds, and raise income from selling off assets, e.g. Royal Mail shares, Lloyds Bank shares.

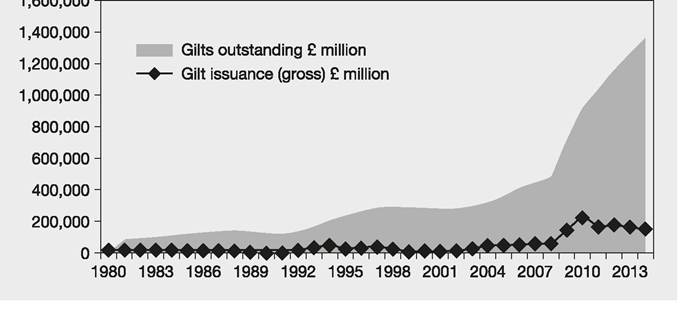

UK government bonds are called gilts because in the old days they were very attractive certificates with gold-leaf edges (gilt-edged securities). Lending to the UK government by buying gilts is one of the safest forms of lending in the world; the risk of the UK government failing to pay is inconceivably small - it has never done so, although a few doubts did creep in following the high government spending during 2010-2011 when the volume of gilts outstanding grew enormously - see Figure 2.4. There are so many gilts held by investors and financial institutions that they equal more than 75% of the amount of output that UK citizens produce in one year (GDP).

Figure 2.4 The amount of UK government gilts in issue up to 2014 and gross issuance (includes gilts sold to replace maturing gilts being redeemed)

Source: Debt Management Office www.DMO.gov.uk

More on the topic UK gilts:

- Sovereign bond risk and return

- Article 16.2 India cuts interest rate to revive growth

- Inflation

- INDEX

- Pax Americana: war and peace across the globe

- INDEX

- BRIEF CONTENTS

- CHAPTER FIVE A Meaningless Fragment: Chernivtsi