Issuing gilts

The UK government issues most gilts through auction via the Debt Management Office (DMO) and each issue receives a unique identification number, an ISIN (International Securities Identification Number).

Gilts are issued with a par (face) value of £100. This is the amount guaranteed to be paid on maturity to the holder, who may or may not be the original purchaser. Their maturity can be 5, 10, 30, 40, 50 and recently 55 years, and during the time to maturity they pay a twice-yearly coupon, the amount of which reflects the current and expected future rates of interest at the time of issue.Most are conventional bonds, but since 1981 gilts have been issued which offset the effect of inflation; the coupons and principal paid on these are linked to the Retail Prices Index (RPI) over the life of the bond and are known as index-linked gilts. Table 2.1 gives examples of conventional and index-linked gilts.

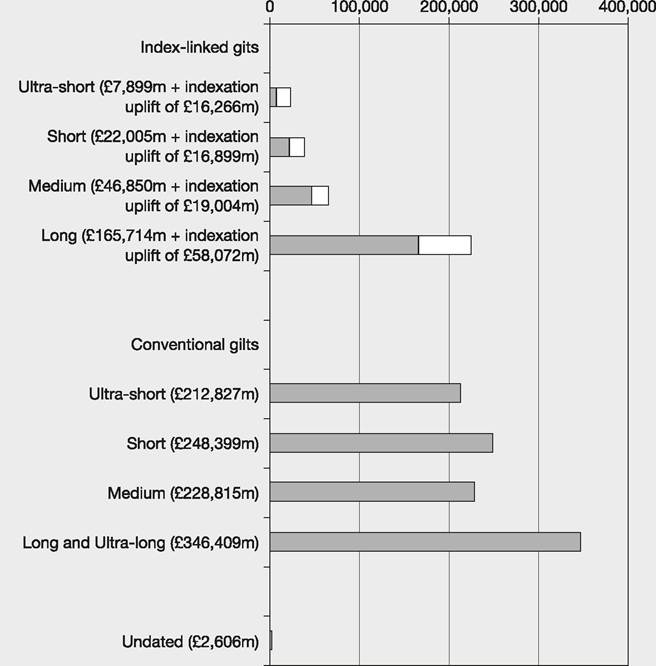

In March 2014 there were 72 gilts in issue with a total outstanding value (including inflation uplift for index-linked gilts) of about £1.4 trillion and of varying maturities - see Figure 2.5. The maturity of a gilt is measured by the remaining time left to redemption.

Table 2.1 Examples of two gilts, the 4¼% Treasury Gilt 2039 and the 2½% Index-linked Treasury Stock 2024

| Coupon amount | Name of gilt | Maturity | ISIN |

| 4¼% | Treasury Gilt | 2039 | GB00B3KJDS62 |

| £100 ? 4¼% ÷ 2. Thus £2.125 will be paid on set dates at 6 monthly intervals to the gilt holder | Those issued in recent years are called Treasury Stocks or Treasury Gilts | The gilt will mature in 2039 at which time the final coupon and the par value of £100 will be paid to the holder | The ISIN is a unique number identifying each gilt |

| 2½% | Index-linked Treasury Stock | 2024 | GB0008983024 |

| £100 ? 2½% ÷ 2. Thus £1.25 plus an increase to take inflation into account will be paid on set dates at 6 monthly intervals to the gilt holder | Those issued in recent years are called Treasury Stocks or Treasury Gilts | The gilt will mature in 2024 at which time the final coupon and the par value of £100 plus an increase to take inflation into account will be paid to the holder | The ISIN is a unique number identifying each gilt |

Source: www.DMO.gov.uk

The UK authorities define the maturities of gilts as:

| • ultra-short conventional | up to 3 years |

| • short conventional | 3-7 years |

| • medium conventional | 7-15 years |

| • long conventional • ultra-long conventional • undated | 15-50 years over 50 years |

| • index-linked | various |

An analysis of the 72 gilts in issue is as follows:

• 40 conventional, with more than £1 trillion of nominal value.

• 24 index-linked, with over £300 billion of nominal value (including the inflation uplift). Of that total, 19 are subject to an inflation uplift in the coupon with a three-month inflation indexation lag (a coupon payable today is raised by inflation that occurred up to a date three months ago) and 5 (issued before 2000) subject to an inflation uplift lagged by eight months. The coupon and principal payment of these is increased according to the

Figure 2.5 UK gilts in issue 12 March 2014, in millions of pounds

Source: DMO, Quarterly Review January-March 2014

change in the RPI. The RPI is published monthly by the Office for National Statistics and measures the change in price of a representative basket of retail goods and services.

• Eight undated older gilts issued between 1853 and 1946 with no redemption date. They pay their coupons in perpetuity, but can be redeemed at the discretion of the government - see Article 2.1. Most pay semi-annual coupons but some pay interest each quarter. Their nominal value is £2.6 billion.

• More than 170 STRIPS of gilts (discussed later in this chapter).

More on the topic Issuing gilts:

- Article 2.2 Hard times force UK seller of gilts on a globe-trotting journey

- [The International Monetary] Fund should focus its surveillance on the systematically important countries issuing major reserve currencies.

- Article 2.3 Europe on track to sell record amounts of inflation-linked debt

- Article 2.1 UK to repay tranche of perpetual war loans

- Article 3.3 Investors be warned: the bond market must turn some time

- The size of the bond markets

- INDEX

- Banker's acceptances

- Sovereign bond risk and return

- Open market operations