Article 2.1 UK to repay tranche of perpetual war loans

By Elaine Moore

Financial Times October 31, 2014

One of Britain's oldest and most unusual national debts is to be repaid, marking the end of an era for a government bond that can trace its lineage back to the 18th century.

As Europe marks the centenary of the Great War, the Treasury has announced it will redeem bonds issued in 1927 by then chancellor Winston Churchill to refinance money borrowed to fund it.

Around 11,200 investors hold the 4% Consolidated Loan, the vast majority of whom are individuals with less than £10,000. Now the government is seeking to take advantage of falling borrowing costs on global capital markets by refinancing the debt at a time when long-dated gilt yields are at a 60-year low.

The ‘4% Consols', as the bonds are known, are perpetual gilts which have no fixed redemption date, giving the government the right to repay them at any time.

On February 1 all investors will be repaid their principal, marking the first time in almost 70 years that the British government has repaid a perpetual bond.

‘This is a great example of pragmatic and attentive debt management on the part of the UK government. I hope that this move is the first of many to cut the interest bill and save taxpayers money,' said Toby Nangle, head of multi-asset allocation at Threadneedle Asset Management, who has argued that the UK could save £300m by exercising its right to call the larger £2bn perpetual ‘War Loan'. Threadneedle is the second-biggest holder of the bond.

The government said it was looking into the practicalities of repaying the loan, which has a 3.5% coupon and trades below face value.

‘Some investors had doubted whether the 3.5% coupon war loan would ever be bought back by the Treasury but this is now clearly on the table,' said Michael Riddell at M&G Investments, which also holds the bonds.

The UK has one of the world's oldest government debt markets and the consolidation of bonds over the years means that the debt redeemed has its origin in the South Sea Bubble crisis of 1720 and the Napoleonic and Crimean wars.

On Twitter, George Osborne, the chancellor, wrote: ‘We'll redeem £218m of 4% Consols, including debts incurred because of the South Sea Bubble. Another financial crisis we're clearing up after.'

FT

Source: Moore, E. (2014) UK to repay tranche of perpetual war loans, Financial Times, 31 October.

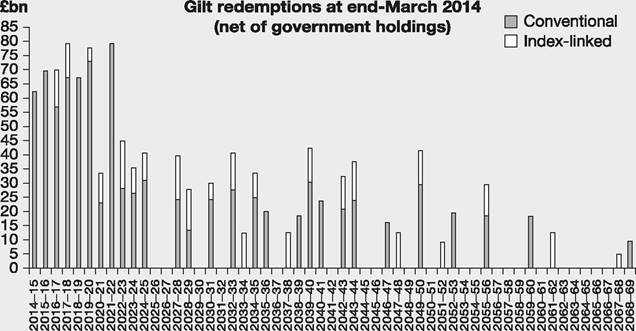

Figure 2.6 When gilts will be redeemed

Source: DMO, Quarterly Review January-March 2014 www.dmo.gov.uk/documentview. aspx?docname=publications/quarterly/jan-mar14.pdf&page=Quarterly_Review

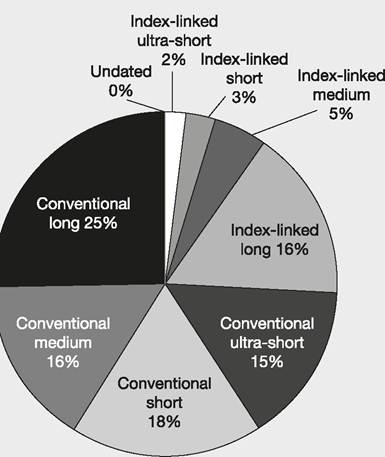

The average maturity for conventional gilts currently outstanding is about 15 years, and for index-linked is 21 years - see Figures 2.6 and 2.7.

When gilts are sold by the government with a nominal value of £100, only the 20 Gilt-edged Market Makers (GEMMs)[5] can submit competitive bids at the auction. They may do this for themselves or for their clients. For conventional gilts, all those who bid above the minimum needed to sell the bonds pay the price they bid (a multiple price auction). For index-linked gilts the pricing at the conclusion of the auction is different: all bidders pay the same lowest accepted price rather than each paying the price at which they bid (a uniform price auction).[6] In return for exclusive access to auctions GEMMs must commit

Figure 2.7 Gilts in issue 12 March 2014

Source: DMO, Quarterly Review January-March 2014

to making a secondary market for gilts by providing continuous prices at which they will buy or sell for the gilts in which they deal.

As well as GEMMs submitting competitive bids at the auction, they can take up the post-auction option facility (PAOF), which enables successful bidders to acquire up to an extra 10% of their allocation at the average accepted (strike) price at conventional auctions and at the single clearing (strike) price at index- linked auctions.

Following an auction GEMMs can trade in the secondary market directly with investors, making available advertised prices between 8am and 5pm every business day in all those gilts in which they are recognised as market maker. They quote two prices: the bid price is the price at which they will buy, the offer price is their selling price. The difference between the bid price and the offer price is known as the dealer's spread, i.e. their potential profit. They are also able to trade gilts anonymously with each other through interdealer brokers (IDBs), who act as intermediaries for GEMMs. IDBs are required to post deals done on their screens for all other GEMMs to see. Below is the list of GEMMs and interdealer brokers at the time of writing.

| GEMMs | Interdealer brokers |

| t Barclays Bank plc | BGC Brokers L.P. |

| BNP Paribas (London branch) | BrokerTec Europe Limited |

| Citigroup Global Markets Limited | Dowgate |

| Credit Suisse Securities | GFI Securities Limited |

| Deutsche Bank AG (London branch) | ICAP WCLK Limited |

| Goldman Sachs International Bank t HSBC Bank plc * Jefferies International Limited JPMorgan Securities plc Lloyds TSB Bank plc Merrill Lynch International Morgan Stanley & Co. International plc Nomura International plc Royal Bank of Canada Europe Limited t Royal Bank of Scotland Santander Global Banking & Markets UK Scotiabank Europe plc Societe Generale Corporate & Investment Banking * The Toronto-Dominion Bank (London branch) UBS Limited | Tullett Prebon Gilts |

t STRIPS market participant

* Retail GEMM

Table 2.2 shows details for the gilts issued over a one-month period.

Note a strange phenomenon in 2014: index-linked issues could be sold at a yield of less than zero before taking into account the inflation uplift, e.g. while the '⅛% Index-linked Treasury Gilt 2019' has a nominal coupon yield of positive one- eighth of 1% per year, it sold at a price of £105.83. The capital loss of £5.83 over the five years (because it will be redeemed at £100 (plus inflation)) means that the yield will be negative 0.918% per annum before inflation uplift. This is an indication that investors were so desperate to invest in ‘safe-haven' assets with both high default protection and some inflation protection that they accepted returns guaranteeing a real-terms reduction of capital value. Bid to cover ratio means the amount investors offered to buy relative to the amount offered for sale.

Table 2.2 Examples of the results of gilt auctions

| Auction date | Gilt name | Indexation lag for index-linked gilts | Amount issued (£m nominal) | Bid to cover ratio at auction | Average accepted price (£) | Yield at average accepted price (%) |

| 12 June 2014 | 0⅛% Index- linked Treasury Gilt 2019 | 3 months | 1,469.76 | 2.78 | 105.830 | -0.918 |

| 10 June 2014 | 2¾% Treasury Gilt 2024 | 3,250.00 | 2.04 | 99.383 | 2.820 | |

| 3 June 2014 | 1¾% Treasury Gilt 2019 | 4,028.42 | 1.61 | 99.095 | 1.936 | |

| 28 May 2014 | 0¼% Index- linked Treasury Gilt 2052 | 3 months | 1,209.97 | 2.56 | 112.068 | -0.065 |

| 15 May 2014 | 4½% Treasury Gilt 2034 | 2,181.56 | 2.00 | 118.591 | 3.243 |

Source: www.dmo.gov.uk

Primary market for retail investors

As well as being able to buy gilts in the secondary market through GEMMs, individuals may bid at auctions providing they have applied for and been accepted into the Approved Group of Investors.[7] The DMOs auction calendar is published up to a year in advance (see www.dmo.gov.uk), but greater details of the gilts to be offered for sale are announced a week or so beforehand. Approved Group investors can then obtain a prospectus and application form.

They may make one non-competitive bid per auction between £1,000 and £500,000 (nominal prices) and they pay the average price set by the successful competitive bidders for conventional gilts and the lowest accepted price for index-linked gilts. Each bid must be a multiple of £1,000. Buyers send payment large enough to more than cover the cost - the exact amount will not be known beforehand as this depends on the results of the competitive auction. After the auction refunds are made for the difference between the amount sent and the amount actually paid.Investors wishing to bid for more than £500,000 nominal in a competitive bid must submit their bids through a GEMM stating the price they wish to pay. If the bid is below the price required to sell the gilts available they will receive no bonds, or only a proportion of those bid for.

Syndication and mini-tenders

Some gilts are sold by syndication, a process whereby the DMO appoints a group of investment banks to manage the sale of the bonds on its behalf. Lead managers and co-lead managers (the chosen banks) market the issue to investors. They ‘build a book', that is, they converse with potential investors and gain indications of offers for the bonds. When the size of the book (serious offers) reaches the DMO's sale objectives, the book is closed and bonds are allocated to investors at the prices previously discussed. In the period following the financial crisis the DMO increased the use of syndications significantly because it had to sell a vast quantity of gilts and the banks were capable of actively finding buyers.

Mini-tenders also take place between the major auctions. They are smaller issues which supplement the main auction sales, and are designed to tap into emerging pockets of demand for particular gilts.

Supplementary issues

If a gilt already in issue is ‘supplemented' (more issued) it keeps the same ISIN number - see Table 2.3, where we can see the details of a 3¾% Treasury Gilt with a redemption date of 2021, issued originally on 18 March 2011 with an initial issuance of £2.75 billion and paying a coupon of £3.75 annually in two equal semi-annual payments made on fixed dates six months apart; with gilt GB00B4RMG977 these payments are on 7 March and 7 September each year.

Since it was first sold, the government raised more money with this gilt, ending up with a total issuance of nearly £28 billion. The purchase (market) price of a gilt varies, depending on the coupon offered, the general level of interest rates in the markets, dealers' perception of future interest rates, and present and expected inflation rates. For gilt GB00B4RMG977 the initial price was £100.80 and the subsequent prices varied between £98.91 and £114.49. At maturity it will be worth £100 and as a gilt approaches maturity its price will become ever nearer to its par value.

Table 2.3 Issuance details of Treasury gilt GB00B4RMG977

| Gilt name | ISIN code | Issue date | Clean price at issue (£) | Yield at issue (%) | Nominal amount issued (£ million) | Cumulative total amount in issue (£ million) |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 18-Mar- 2011 | 100.80 | 3.657 | 2,750.000 | 2,750.000 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 06-Apr- 2011 | 98.91 | 3.878 | 3,807.112 | 6,557.112 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 03-Jun- 2011 | 102.88 | 3.414 | 3,603.787 | 10,160.899 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 06-Jul- 2011 | 102.03 | 3.510 | 3,572.947 | 13,733.846 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 02-Sep- 2011 | 108.59 | 2.762 | 3,000.000 | 16,733.846 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 05-Oct- 2011 | 113.37 | 2.239 | 3,574.970 | 20,308.816 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 19-Oct- 2011 | N/A | N/A | 440.000 | 20,748.816 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 02-Dec- 2011 | 111.85 | 2.382 | 3,298.400 | 24,047.216 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 12-Jan- 2012 | 114.49 | 2.084 | 3,282.568 | 27,329.784 |

| 3¾% Treasury Gilt 2021 | GB00B4RMG977 | 17-Jul- 2012 | N/A | N/A | 379.000 | 27,708.784 |

Source: www.dmo.gov.uk

From the clean price (the price of the gilt excluding any accrued interest since the last coupon was paid - see later in the chapter) and yield at issue we can gain an impression of how the prevailing rate of interest for securities with a similar risk and maturity changed over the period March 2011 to January 2012, falling 157 basis points. Indeed, interest rates usually change daily, even if usually by very small amounts.

Who buys gilts?

Table 2.4 shows that the main purchasers of gilts are outside of the UK. Also, in recent years, one buyer has gone from being quite small to being dominant: the Bank of England bought large amounts of gilts on the secondary market to lower interest rates and try to revive the post-crisis economy (see Chapter 16 for a discussion of this ‘quantitative easing').

Table 2.4 Distribution of UK gilt holders December 2013

| (£ millions) at end | Q3 2013 | Q4 2013 |

| Overseas | 393,937 | 413,104 |

| Bank of England (Asset Purchase Facility) | 373,561 | 367,486 |

| Insurance companies and pension funds | 370,019 | 365,027 |

| Monetary Financial Institutions* | 122,458 | 133,349 |

| Other financial institutions and other | 88,779 | 89,882 |

| Households | 16,882 | 12,093 |

| Local authorities and public corporations | 2,206 | 2,155 |

| TOTAL | 1,367,842 | 1,383,096 |

* ‘Monetary Financial Institutions’ replaced the ‘Banks’ and ‘Building Societies’ categories in January 2011 and excludes Bank of England holdings.

Source: DMO, Quarterly Review January-March 2014 www.dmo.gov.uk/documentview.aspx7docname= publications/quarterly/jan-mar14.pdf&page=Quarterly_Review

Article 2.2 discusses the operations of the DMO, with particular reference to the necessity to sell gilts to overseas investors.