AN OVERVIEW OF A UNIFIED ANALYTICS PLATFORM

Unified analytics would make the marketplace lending sector safer and more transparent. However, analytics come with a high price tag. Banks spend millions of dollars annually to keep their analytics current and to push the envelope on making their algorithms smarter.

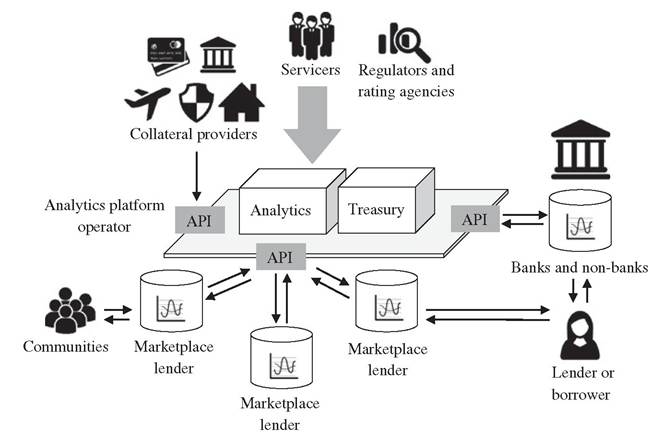

The reason we point out that analytics should be unified is that it will then also be platformindependent. A third party could offer robust and transparent analytics for the entire sector as a service instead of every single platform reinventing the wheel with a proprietary analytics package. Many service providers already specialize in analytics software for banks, but they customize their solutions for each customer, running independently from the rest of the market. Third-party analytics solutions in the banking sector still have a long way to go towards unified analytics. Yet, with marketplace lending, a unified approach is doable because the market is still nascent and relatively small in size.Individual marketplace lending platforms can pipe their data into a central analytics engine with an API. In return, they will receive the output of the analytics, in the form of data or charts. They can then use this output internally for their underwriting and risk management, or they can let borrowers and lenders use the engine to analyze their portfolios of loans. Figure 17.1 shows what a unified analytics engine might look like.

FIGURE 17.1 Unified analytics platform for marketplace lending with different stakeholders

Figure icons designed by Freepik

Let's now zoom in on the individual stakeholders of a unified analytics platform, their functions and direct benefits. We have already discussed some of these benefits in the previous paragraphs. Table 17.1 summarizes them and adds a few additional benefits.

Part Two of the book introduced most of the functions of the computational engine underlying a unified analytics platform. Repeating them here at length would therefore be redundant. The list below summarizes the most important functions of the analytics engine.

■ Capability to securely plug in to multidimensional marketplace lending systems and platforms

■ Get all information in regarding

■ Financial risk factors (market, counterparty, behavior) linked to individual contracts

■ Peers (counterparties)

■ Map all contract agreements

■ Structuring portfolios

■ Calculate the value of all contracts, e.g., loans

■ Identify and estimate all expected in and out cash-flows of all contracts to identify the

■ Market liquidity

■ Funding liquidity

■ Calculate the value and liquidity at risk based on real world probabilities

■ Calculate the income (i.e., P&L)

■ Calculate the concentration risk in the level of

■ Counterparties, i.e., all types of Peers

■ Exposures

■ Know the Systemic Risk in regards to

TABLE 17.1 Stakeholders, functions, and benefits of a unified analytics platform

Stakeholders Functions Direct benefits

| Marketplace | Stream data into the | ■ World-class interactive analytics for a |

| lenders | platform and receive | fraction of the cost of developing and |

| processed analytics via | supporting a solution in-house | |

| APIs | ■ Introduction of standards for financial | |

| data and analytics regarding risk and profitability analysis. This would make investments robust against risk and potential losses and ensure optimal profitability | ||

| ■ Interoperability across platforms helps | ||

| understanding of hard-to-quantify risks and systemic concentration | ||

| ■ High standard of transparency | ||

| Lenders | Adjust variables on a | ■ Strong risk and profitability analysis |

| customizable interface on | portfolios and loans | |

| the marketplace lender's | ■ Compare and combine investments | |

| website | across platforms and investment products from formal sector | |

| Borrowers | Analyze existing contracts | ■ Clarity about their ability to service loans |

| and exposure | and borrow under stress |

■ Clarity about available options to prepay and the consequences of executing these options on borrowers, correlated counterparties, and the entire platform or the wider credit system

| Communities | Stream data into the | ■ Low overhead with on-demand add-ons, |

| operating a closed | platform and receive | such as analytics |

| lending platform | processed analytics via APIs | |

| Operator of the | Develop, operate, and | ■ Revenues from platforms, banks, |

| unified analytics | support the unified | governments (regulators) |

| platform | analytics platform | |

| Collateral providers | Stream data into the | ■ Real-time feedback for changes in |

| and servicers | platform and receive | collateral |

| processed analytics via | ■ Digitization of operations: central record | |

| APIs | keeping, central data standard | |

| Regulators and | Adjust variables on a | ■ Real-time stress testing |

| rating agencies | customizable interface | ■ Real-time compliance checks ■ Digitization of operations, central record |

keeping, central data standard

| TABLE 17.1 | (Continued) | |

| Stakeholders | Functions | Direct benefits |

| Banks and non-banks | Stream data into the platform and receive processed analytics via APIs or Banks could develop a unified analytics platform for marketplace lenders and other online lenders | ■ Banks could spearhead a unified analytics platform with their existing experience and talent ■ Provide and use world-class interactive analytics for a fraction of the cost of developing and supporting a solution in-house ■ Introduction of data and analytics standards ■ Stewardship of best practices in the industry ■ Promoting transparency in the credit asset class ■ Interoperability across platforms helps understand hard-to-quantify risks (concentration) ■ High standard of transparency ■ Integration of the formal and informal financial sector |

■ Correlated (linked) counterparties, i.e., all types of peers

■ Correlated exposures

■ Capability to restructure a portfolio to

■ Increase (real) profitability

■ Optimize the exposure to different financial risks

■ Minimize losses

■ Manage the exposure to risks

■ Mitigate risk (by structuring credit enhancements)

17.2.1 Standardizing financial data and analytics

A big step forward—and a feasible one in the short-term—would be uniform data standards for marketplace lenders. A data standard needs agreement on conventions to meta tag the data they collect and report on counterparties and loans on their system.

It may be difficult for individual platforms to agree on standards at the current time when they are still driving a fragmentation strategy, hoping to capture market share from each other. Therefore, introducing data standards and analytics opens up a huge market opportunity for third parties who can provide this service. If a company focuses exclusively on providing risk analytics and financial reporting for loans, and manages to get the dominant marketplace lending platforms on board, its services will be very useful for all stakeholders.Some platforms already offer services and analytics for institutional investors to invest across several platforms in the U.S. They might just as well go the other way and perform the same service in the other direction, where they offer a data standard into which all underwriters of marketplace loans plug in. Unified analytics would be available by platforms via an API. The platform would standardize and process the data and return outputs that marketplace lenders could then make available interactively on their sites. Unified analytics that let investors compare loans in the entire asset class would be a boon and a huge step forward. By the same token, unified standards for data reporting and analytics need hardly stop at marketplace lenders. Other alternative lenders with online operations could also benefit from this service, and so could banks, eventually. Imagine investors objectively comparing the risk of loans, originated on different online platforms, with more traditional investments from banks or non-banks. What a quantum leap forward this would be from the opacity and guesswork that the current investment process in some financial products entails.

However, wrangling financial data from reluctant institutions and reporting financial analytics can be an expensive endeavor for a startup or online lending platform. This is a specialist domain within the financial services industry, with the available talent firmly concentrated in established financial institutions.

Because banks have the experience and talent and in fact wrote the book about industrial-strength analytics and data collection, this invites them to jump in and provide unified analytics for newly emerging marketplace lenders. Next to offering a useful service, positioning themselves at the helm of unified analytics for online lenders is an excellent opportunity for banks to hedge their bets on financial technology innovation and stay relevant with the new players in the future.17.2.1.1 Data and analytics standards Regulators, investors, and other stakeholders are urging financial institutions across different markets to provide standardized reports that are homogenous and comparative. This increases the confidence of markets in the profitability and stability of financial institutions. It also enhances the infrastructure for reporting key information to identify, monitor, and manage risks. Data standards serve the decision-making process by increasing the speed at which information is available and decisions can be made. They also improve an organization’s quality of strategic planning and the ability to manage the risk of new products and services.

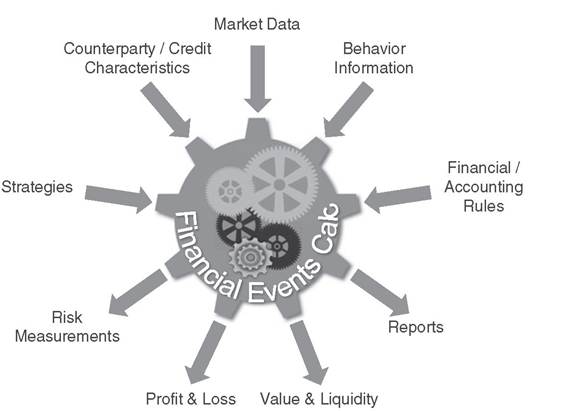

Unfortunately, financial reports are often incongruent, even though we assume that we have clean and homogenous information. This is happening because every analytics system may use similar—but not identical—algorithms and methods. Therefore, even when we use the same data for calculating financial events, the result and reports for liquidity, value, profit and loss, risk exposures and measurements may vary more than we would expect. Again, standardizing data across a relatively small segment of the credit sector, such as the marketplace lending niche, is a doable first step towards harmonization. Figure 17.2 shows the different categories of data that platforms would have to collect.

Unified analytics in the financial sector has been a dream of the analytics community for a while. The shopping list for data in unified analytics is relatively modest, yet getting the financial system to report these data accurately and on time is difficult.

Without pointing the finger, it is clear that financial institutions can use their regulatory overhead to delay publishing accurate results and obfuscating relevant information in their numbers. Banks then pass the mess to regulators with the ungrateful task of untangling it. A much more elegant solution is the unified analytics platform from Figure 17.1. To force thousands of banks onto such a platform is impossible today. However, marketplace lending would be a feasible test case. Dealing with a few hundred small platforms, and their loan books with about 200,000 contracts each, is doable today.

FIGURE 17.2 One engine providing consistent results, e.g., credit, liquidity value and their risk measurements

17.2.1.2 Who should push for unified analytics? Who should drive the strategy for unified data and analytics? Even though banks are ideally positioned to create an analytics platform, they might be blind to its benefits. Therefore, marketplace lending platforms themselves should take the lead and get to work on unified analytics. Instead of the sector anxiously waiting for the regulatory hammer to drop, marketplace lenders can take matters into their own hands and propose a solution. This could take a similar form to the payment networks that several large banks own collectively. At the same time, the young marketplace lending industry can prove that it truly cares about transparency and playing by the rules.

Honesty is the best policy, especially for those in credit provision. What a powerful signal self-imposed standards on data, analytics, and transparency would send to all players in a market that thrives on opaque information. Certainly, such an aggressive strategy comes with risks attached. At the same time, the marketplace lending sector is in a position where it can afford to take bold steps forward.

17.3

More on the topic AN OVERVIEW OF A UNIFIED ANALYTICS PLATFORM:

- AN OVERVIEW OF A UNIFIED ANALYTICS PLATFORM

- WHY DO MARKETPLACE LENDING PLATFORMS NEED UNIFIED FINANCIAL ANALYTICS?

- Akkizidis Ioannis, Stagars Manuel. Marketplace Lending, Analysis Financial, and the Future of Credit: Integration, Profitability, and Risk Management. Wiley,2016. — 344 p., 2016