Pressures for Depreciation and Appreciation Since 1994

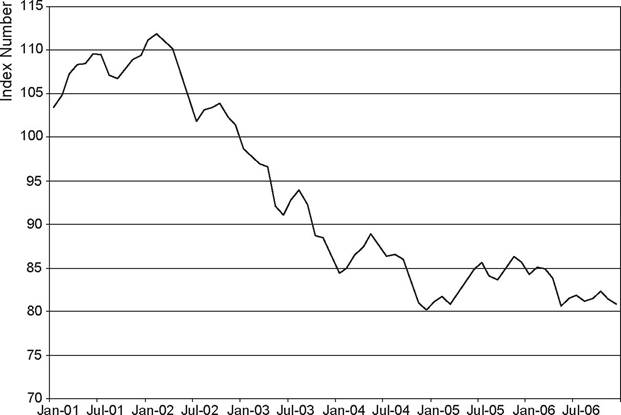

Even after the dollar began weakening against other world currencies in 2002 (see Figure 1.1), China kept the exchange rate between the renminbi and the dollar in the close range maintained since the major devaluation of January 1, 1994.

After the initial adjustment to 8.62 RMB/$US in 1994, thep. 43). Going beyond current account transactions, though, the official rate assumed more importance given that “the coverage of transactions at the official exchange rate [was] considerably wider, and include[d] debt service payments and all the central government imports that [were] financed from foreign loan proceeds, the draw down of reserves, or foreign exchange earnings from the exports of invisibles” (World Bank, 1994, p. 42).

6 See Lin and Schramm (2004, pp. 87-89) for further details of the operation of the new interbank market.

Figure 1.1. US Dollar Trade Weighted Exchange Index: Major Currencies (Index March 1973 = 100). Sources: Board of Governors of the Federal ReserveSystem, Federal Reserve Bank of St. Louis.

exchange rate was allowed to gradually strengthen to 8.28RMB/$US by 1998 but then remained fixed at this same 8.28 level for seven years. Although the exchange rate policy adopted in 1994 always allowed for daily fluctuations of up to 0.3%, the permitted range of fluctuation was, in practice, quite limited and the effective bands were tightened over time as the People’s Bank intervened more and more in order to minimize volatility. By late 2004, the permitted range of fluctuation approached zero and “Chinese practice was virtually indistinguishable from a full outright fixed exchange rate” (Anderson, 2006b, p. 5). On an annual basis, the renminbi/$US dollar exchange rate had remained near constant since 1995, varying only from 8.35 RMB/$US to 8.28 RMB/$US and consistent with the maintenance of a very rigid dollar peg over this whole period preceding the July 21, 2005 revaluation.

Pressure for adjusting a pegged exchange rate with the US dollar emerges if China’s goods’ prices do not keep pace with US prices. If, for example, China’s price level doubled while the US price level remained constant, China’s exports would become twice as expensive in the United States. In reducing China’s sales abroad this would also reduce the demand for the renminbi needed to purchase such goods, and in turn put pressure on

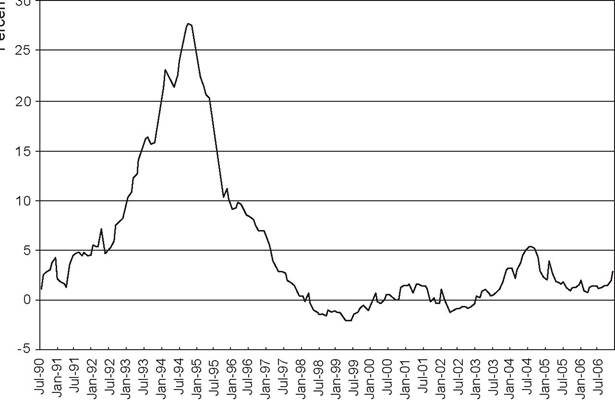

Figure 1.2. China's Real Eflective Exchange Rate Index (2000 = 100). Source: International Monetary Fund.

the (now unwanted) renminbi to fall in value against the US dollar. If the People’s Bank of China sought to maintain a fixed exchange rate under this scenario, the central bank would have to buy back its own currency to support its value, thereby reducing the rate of domestic monetary expansion. This situation would represent a constant nominal exchange rate but a rising real exchange rate that reflects the rising world price of Chinese goods. Moreover, a rising real exchange rate implies increasing pressure for currency depreciation that the central bank must try to forestall by buying back its own currency if the fixed nominal exchange rate is to be maintained.

Given that China trades with many countries besides the United States, a representative real exchange rate measure should take into account price movements relative to all of China’s major trading partners. The International Monetary Fund calculates such an index, known as the real effective exchange rate, that weights each foreign country by its share of trade with China. This real exchange rate measure, shown in Figure 1.2, enjoyed a steady rise from 1994-1998. Over this period, China’s price level rose more rapidly than most of its trading partners, making Chinese goods more expensive abroad. Although the renminbi was fixed against the US dollar, and the dollar remained strong against most other major currencies, China’s real exchange rate appreciated both relative to the dollar and relative to the full set of countries considered in the effective exchange rate

Figure 1.3.

China's Inflation Rate (Consumer Price Index). Source: Great China Database.measure. The pressures for devaluation peaked at the time of the 1997-1998 Asian financial crisis, when almost all Asian countries outside China and Hong Kong abandoned their own pegged exchange rates with the US dollar. As these other currencies fell against the dollar (in some cases to a dramatic degree such as the near 90% depreciation of the Indonesian rupiah), they fell against the renminbi as well. Thus China faced a sudden additional loss of competitiveness against its Asian rivals and renminbi devaluation seemed almost inevitable at the time. Indeed, the writer can attest from personal experience that the unofficial exchange rates offered for US dollars in Beijing in the summer of 1998 were significantly more generous than the official rate of 8.28.

The pressure for renminbi depreciation during the Asian Financial Crisis was forestalled by tight monetary policy, and tight credit, as the People’s Bank of China intervened and bought back its own currency to support its value. The maintenance of the pegged rate was also aided by the fact that capital controls limited foreign access to the renminbi. It was not possible for speculators to sell short (sell borrowed renminbi) against the US dollar, for example, and so the renminbi was spared the kind of speculative attack that was orchestrated against the Hong Kong dollar in 1997-1998. Nevertheless, the tight monetary policy helped push China into deflation in late 1998 as shown in Figure 1.3, which depicts China’s inflation rates over the post-1990 period. As China’s price level fell from 1998 through the beginning of 2001, China’s exports tended to become cheaper in world terms, pressures for depreciation were alleviated, and the rise in the real exchange rate started to reverse. Economic growth slowed, however, and there was marked acceleration of savings relative to consumption in the face of economic uncertainty and tight credit markets.

China certainly paid a price for warding off currency depreciation and received kudos from the US administration at the time that were apparently quickly forgotten when the pressures on the currency later reversed after 2002.[7]The fall in the real exchange rate was temporarily interrupted in 20002001 as the strength of the US dollar against other most major world currencies, including the euro, carried the renminbi upward against these same currencies. The renewed upward pressure on the real exchange rate at this time can be seen in Figure 1.2. However, after the dollar’s decline began in early 2002, China’s real exchange rate fell as well and China’s goods started to become cheaper and cheaper in non-US dollar countries. Demand for renminbi to purchase Chinese exports soared, and there was a natural pressure for renminbi appreciation in the face of all this extra demand. Offsetting this pressure required the People’s Bank to reverse its intervention of the late 1990s. The goal now was to hold the renminbi down by buying the relatively weak US dollar and issuing in exchange larger and larger quantities of renminbi. This helped make renminbi more abundant and the dollar scarcer, thereby offsetting the underlying impetus for the renminbi to rise above its pegged exchange rate with the US dollar.

Matching the post-2002 dollar depreciation not only had the effect of making the renminbi artificially cheaper in world terms, therefore, but has also induced more rapid expansion in the supply of renminbi that threatens inflation to the extent that too much money ends up chasing too few goods. Broad money supply growth accelerated to nearly 20% in 2003 before dropping back to 15% in 2004. Money supply growth then rose again to 17.6% in 2005 and remained at 16.9% in 2006 - standing at an annualized 17.3% through the first quarter of 2007 (People’s Bank of China, 2007). The People’s Bank of China has attempted to dampen the rate of credit expansion through sales of government bonds that withdraw money from circulation and by taking steps to discourage credit creation by the banking system (Chapter 4). Inflationary pressures were further augmented by “hot

money” flowing into China after 2002 as speculators bet on revaluation of the renminbi against the dollar that would yield capital gains to those exchanging dollars for renminbi at the original, cheaper pegged rate of 8.28 renminbi to the dollar. Following the limited revaluation implemented in July 2005, a renewed surge of capital inflows beginning in late 2005 led to accelerating reserve accumulation that made it increasingly difficult for the People’s Bank to contain money growth and credit creation.