Redeemable bonds

A purchaser of a redeemable bond buys two types of income promise: first the coupon, second the redemption payment. The amount that an investor will pay depends on the amount these income flows are presently worth when discounted at the current rate of return required on that risk class of debt.

The relationships are expressed in the following formulae:

and:

where C1, C2, C3 and C4 = nominal interest per bond in years 1, 2, 3 and 4 up to n years

I1,12,13 and I4 = total nominal interest in years 1, 2, 3 and 4 up to n years

Rn and R* = redemption value of a single bond, and total redemption value of all bonds in issue in year n, the redemption date or maturity date.

The following examples illustrate the valuation of a bond when the market redemption yield is given.

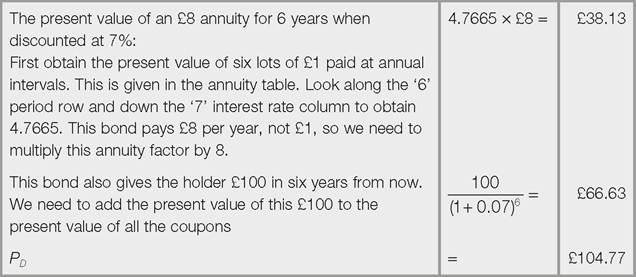

Example 13.1

Blackaby plc issued a bond with a par value of £100 in September 2014, redeemable in September 2020 at par. The coupon is 8% payable annually in September. Therefore:

• the bond has a par value of £100 but this may not be what investors will pay for it

• the annual cash payment will be £8 (8% of par)

• in September 2020, £100 will be handed over to the bond holder (in the absence of default by the issuer).

The price investors will pay for this bond at the time of issue if the current market rate of interest for a security in this risk class is 7% can be worked out as follows (computers and financial calculators will perform the task quicker, but by doing it the old-fashioned way you gain a greater understanding of what is going on inside the ‘black box' of the machine):

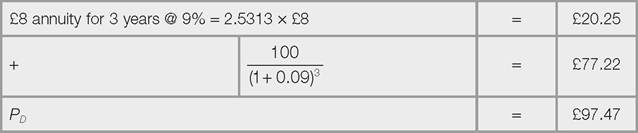

Example 13.2

It is now three years later.

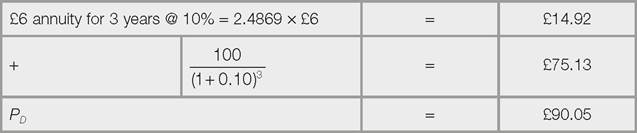

What is the value of Blackaby's bond in the secondary market in September 2017 if market interest rates rise by 200 basis points (i.e. for this risk class they rise to 9%)? (Assume the next coupon payment is in one year.)

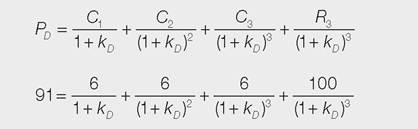

If we need to calculate the rate of return demanded by investors from a particular bond when we know the market price they are paying and coupon amounts, we can compute the internal rate of return (IRR)[27] - see Example 13.3.

Example 13.3

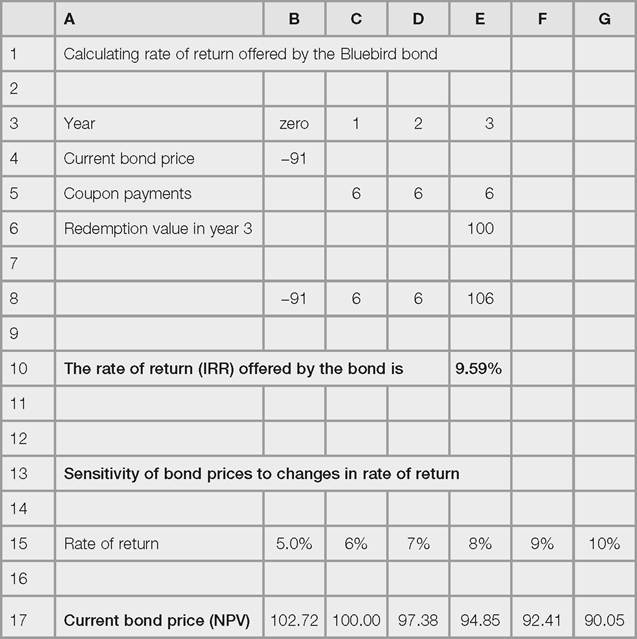

Bluebird plc issued a bond many years ago that is due for redemption at £100 par in three years. The annual coupon is 6% (next one payable in one year) and the market price is £91. The rate of return now offered in the market by this bond is found by solving for kD:

We'll solve this problem through iteration, i.e. trial and error, by trying one interest rate after another on paper. First we will try 9%, as this seems roughly right given the capital gain of around 3% per year over the three years (i.e. £9 overall) plus the 6% coupon.

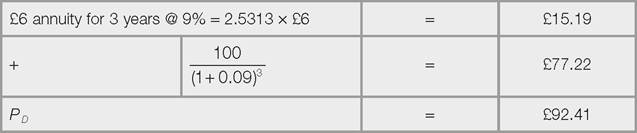

At an interest rate (kDD) of 9%, the right side of the equation amounts to £92.41:

This is more than the £91 on the left side of the equation, so we conclude that we are not discounting the cash flows on the right side of the equation by a sufficiently high rate of return. At an interest rate of 10% the right-hand side of the equation amounts to £90.05:

This is less than the £91 we are aiming at, so the internal rate of return lies somewhere between 9% and 10%. We can be more precise using linear interpolation:

We are trying to find the value of kD, where the cash flows are discounted at just the right rate to equal the amount paid for the bond (£91).

kD is 9% plus the fraction formed by the difference between points ‘a' and ‘b', that is 92.41 - 91, divided by the difference between points ‘a' and ‘c', that is 92.41 - 90.05, multiplied by the number of percentage points between a and c, that is 10 - 9, one percentage point:

Thus the cash flows offered on this bond represent an average annual rate of return of 9.59% on a £91 investment if the bond is held to maturity and the coupon payments are reinvested at 9.59% before then. This is the yield to maturity or YTM discussed in the next section.

Excel offers formulae, IRR and NPV, for these calculations - see below:

Using the above figures, format a cell (in this case E10) in Excel as a percentage and type in

=IRR(B8:E8)

and 9.59% will appear in cell E10.

To understand the sensitivity of bond prices to changes in the rate of return, type into a cell (in this case B17)

=NPV(B15,$C8:$E8)

and 102.72 will appear in cell B17, which is the market price if the rate of return is 5%. ( NPV is the net present value of all the cash inflows, ignoring the initial outflow to buy the bond.) The figures for 6%, 7%, 8%, 9% and 10% can be worked out in the same fashion, or by copying B17 and pasting in C17, D17, E17, F17 and G17.