Reserve Accumulation and the InternationalRole of the Dollar

Limiting the renminbi’s appreciation against the increasingly weak US dollar has required large-scale central bank purchases of dollars that induce more rapid expansion in the domestic supply unless these purchases can be “sterilized” through offsetting withdrawals of currency from circulation (see Chapter 4).

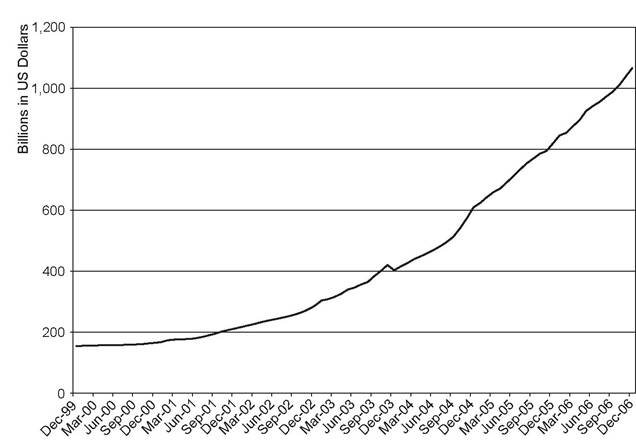

Expansionary pressures were further augmented by “hot money” flowing into China with a renewed surge of capital inflows following the new exchange rate policy announced in July 2005 that was widely seen as setting the stage for further renminbi revaluation over time. The rate of increase in consumer prices in China initially remained relatively benign, with the inflation rate only briefly exceeding 5% in the third quarter of 2004 before dropping back below 2% in 2005-2006.11 Nevertheless, the rate of accumulation of foreign reserves continued at an ever-accelerating rate over the post-2000 period (see Figure 2.4). In addition to speculative capital flows, other factors in the recent surge in China’s foreign exchange reserves include ongoing steps toward capital account liberalization and the dollar

Figure2.4. China's Foreign Exchange Reserves (inbillions ofUS dollars). Source: People's Bank of China.

purchases required to maintain the managed exchange rate bands (see also Zheng and Yi, 2007). As discussed in Chapter 8, almost certainly some of the liquidity influx was being channeled into the stock market and housing market.[26]

The reserve accumulation and accompanying growth in the US current account deficit with China is itself part of a worldwide trend toward larger current account surpluses among emerging economies. In 2006, for example, China's balance of payments surplus of US $238.5 billion was almost matched by a $212.4 billion surplus in the Middle East (International Monetary Fund, 2007, p.

251). Elsewhere, Russia enjoyed a $95.6 billion surplus and there has also been an increasing move to current account surpluses in Latin America, reaching an aggregate $48.7 billion in 2006. The trend toward US current account surpluses being matched primarily by emerging market current account surpluses has been emphasized by Bernanke (2005, 2007), who points to reserve accumulation in East Asian and Latin American countries since the financial crises of the late 1990s as well as the effects of rising oil prices in boosting surpluses in the Middle East, Russia, and other oil-producing nations such as Nigeria and Venezuela. Between 1999 and 2006, a $534.8 billion increase in the US current account deficit was countered by a $501.8 billion swing in the collective current account position of emerging market economies from a collective $21.2 billion deficit in 1999 to a $544.2 billion surplus in 2006.[27]John Lipsky (2007), First Deputy Managing Director of the International Monetary Fund, recently acknowledged the Fund’s worry that “rather than shrinking as anticipated [with the post-2002 recovery in global growth], global payments imbalances reached a record high, leading to growing concerns about the threat of impending economic and financial instability.”[28] The Fund’s Multilateral Consultation on Global Imbalances was launched in 2006 to address these developments, with participation from China and other major surplus countries such as Saudi Arabia and Japan in addition to representation of the euro area and the United States. Based on Bernanke’s (2005, 2007) view, the imbalances primarily reflected high savings growth abroad combined with the attraction of US financial markets as a destination for this saving. Bernanke (2005) points to foreign capital inflows being drawn, first by rising US equity prices in the 1990s and then by a booming US housing market after the 2000 market crash - as well as the ensuing post-2003 stock market recovery.

With the sophisticated US financial system essentially intermediating savings originating in China and elsewhere, Dooley, Folkerts-Landau, and Garber (2004) see the United States serving as the de facto center country in a “Revived Bretton Woods System.” If their “portfolio balance” view of global imbalances is correct, such capital flows are the result of portfolio optimization and not indicative of any need for drastic exchange rate adjustment (cf. Xafa, 2007).The dollar’s role as the major international reserve currency has certainly played a major part in drawing foreign funds into US assets. The total inflow from foreign central banks reached $498 billion in 2004, financing as much as 75% of the 2004 trade deficit. The willingness of other central banks to, thus far, continue accumulating dollar assets goes a long way toward explaining why, even in the face of such large trade deficits, the dollar did not fall further over the 2002-2007 period. Mainland China, in fact, became the second largest foreign holder of US Treasuries after Japan in 2006, with its holdings of US Treasuries more than doubling since June 30,2004 (when China’s holdings stood at $341 billion). As of June 30, 2006, US Treasury figures assessed mainland China’s reserve accumulation of US Treasuries at $699 billion, up from $527 billion on June 30, 2005 (US Department of the Treasury et al., 2007).

Observers such as Eichengreen (2007) have questioned whether the dollar will remain such a dominant reserve currency of choice in the future, however, suggesting that this role will be increasingly shared with other currencies like the euro. There is also the question of the dollar’s role in pricing, and settling trades in, most internationally-traded commodities such as oil. Were oil invoicing to switch from the dollar to the euro, for example, the “petrodollar” recycling of the surpluses enjoyed by the oilproducing nations could well be transformed into “petroeuros” instead (Rajan and Kiran, 2006).

Some signs of a limited move away from the dollar emerged in 2006 as a number of central banks, ranging from Italy, Russia, and Switzerland to the United Arab Emirates, announced plans to reduce the proportion of dollar holdings in their reserves (see Garnham, Giles, and Brown-Humes, 2006, p. 11). In addition, in May 2007, Kuwait elected to delink its currency from the dollar as the combination of a weakening dollar and a strong domestic economy produced increasing inflationary pressures. This not only shows that China is far from the only economy facing difficulties in dealing with the downward trend in the dollar, but also could potentially be an early sign of more widespread retreat from foreign central bank dollar purchases.Kerr (2007, p. 13) points out:

If Kuwait’s oil-rich neighbours also dropped their dollar pegs, the impact would be felt way beyond the Gulf. Countries in the region could buy fewer dollars and put less of their booming foreign exchange reserves into US assets such as Treasury bonds.

Possible effects of flight from the dollar likely include higher yields on Treasury securities if foreign central bank purchases declined, but there is little consensus as to how important this effect would be. Recent estimates as to the impact of central bank reserve accumulation on US Treasury yields have

Table 2.1. China’s New Foreign InvestmentAgency and Other Sovereign Wealth Funds

| Country | Sovereign Wealth Fund | Estimated Size* | Year Begun |

| United Arab Emirates | Abu Dhabi Investment Authority | $625.0 billion | 1976 |

| Norway | Government Pension Fund | $322.0 billion | 1990 |

| Singapore | Government Investment Corporation | $215.0 billion | 1981 |

| Kuwait Investment Authority | $213.0 billion | 1953 | |

| China | China Investment Corporation (CIC) | $200.0 billion | 2007 |

| Russia | Stabilisation Fund | $127.5 billion | 2004 |

| Singapore | Temasek Holdings | $108.0 billion | 1974 |

| Qatar | Qatar Investment Authority | $60.0 billion | 2005 |

| US State of Alaska | Permanent Reserve Fund | $40.2 billion | 1976 |

| Brunei | Brunei Investment Authority | $30.0 billion | 1983 |

* As of October 2007.

Source: Larsen (2008, p. 2).

ranged from zero to 200 basis points (see European Central Bank, 2006, pp. 23-25). Warnock and Warnock (2006) subsequently suggested that, after controlling for other factors, foreign official purchases of US securities exerted an approximate 90 basis point effect on 10-year Treasury yields over the 1984-2005 period. However, future surpluses may not translate so automatically into reserve holdings of US Treasuries. A growing array of sovereign wealth funds has been created by a number of surplus countries, including the United Arab Emirates (whose Abu Dhabi Investment Authority is considered the largest such fund, weighing in at perhaps US $625 billion), as well as Norway, Singapore, Kuwait, and China (see Table 2.1).[29] Sovereign wealth funds appear to be on track to surpass total official reserve holdings as early as 2011, with Stephen Jen of Morgan Stanley predicting growth from a total estimated size of $2,510 billion in early 2007 to perhaps $6,500 billion by 2011 and $12,000 billion by 2015 (Jen, 2007).

China’s own sovereign wealth fund, China Investment Corporation (CIC), was formally inaugurated on September 29, 2007, with initial registered capital of $200 billion. It actually commenced operations earlier in the year, with a relatively aggressive investment stance suggested by the May 2007 move to invest $3 billion in the initial public offering (IPO) of the Blackstone Group, a major US private equity firm. This is likely to form part of a potentially major move away from surplus countries’ emphasis on US Treasuries, although, as the Blackstone purchase implies, not necessarily a move away from US assets altogether.[30] In fact, China’s Premier Wen Jiabao stated that the establishment of CIC would “not have any adverse impact on U.S.-dollar denominated assets.”[31] However, it is still possible that new funds accumulated via China’s ongoing current account surpluses with the United States could be invested on a more diversified basis than has been the case in the past. Should funds be reallocated to the euro, as the most viable alternative major currency, the higher demand may well boost the euro’s value - but also have the rather less welcome effect of furthering the loss of competitiveness vis-a-vis the United States already experienced by the euro-zone countries in the post-2001 period. Blanchard, Giavazzi, and Sa (2005, p. 39) characterized the old status quo as follows:

The trade deficits of the United States with Japan and the euro area imply an appreciation of both the yen and the euro against the dollar. For the time being, this effect is partly offset by the Chinese policies of pegging and keeping most of its reserves in dollars. If China were to give up its peg or to diversify its reserves, the euro and the yen would appreciate further against the dollar.