Would Renminbi Appreciation Really Help the US Trade Balance?

The deficits that mainland China has consistently run with its Asian partners reflect China’s role as “final assembler” of many products made elsewhere in the region. Hufbauer, Yong, and Sheth (2006) point out that approximately 55% of China’s total exports, and as much as 65% of China’s exports to the United States, have represented goods assembled from imported parts and components.

Owing to China’s position in Asian production networks, “the US bilateral trade balance with China rises as its trade imbalance falls with other Asian countries, especially Hong Kong, Taiwan, Korea, and Japan” (Hufbauer, Yong, and Sheth, 2006, p. 6). This would naturally tend to make unilateral renminbi appreciation an unlikely solution for overall US trade imbalances. The more probable outcome would be to “shift Asian countries’ assembly plants to other low-cost Asian countries, not back to America” (Jin and Li, 2007). Past growth of the US bilateral trade deficit with China itself includes substantial gains at the expense of other developing economies. A case in point is the way in which a rise in Chinese textile sales to the United States was largely offset by reduced imports from other countries after import quotas ended in December 2004 (Stiglitz, 2005).The nature of China’s exports to the United States is another factor working against the scope for renminbi appreciation reining in the US trade deficit. With US imports from China being concentrated among basic necessities and low-tech products, the elasticity of substitution is likely considerably lower than for high-tech and high value-added products imported from elsewhere.[22] Zhang, Fung, and Kummer (2006) suggest that volumes of Chinese imports may not decline sufficiently to prevent the dollar value of Chinese imports from actually rising in the face of a renminbi revaluation that drives up the US price of Chinese goods.

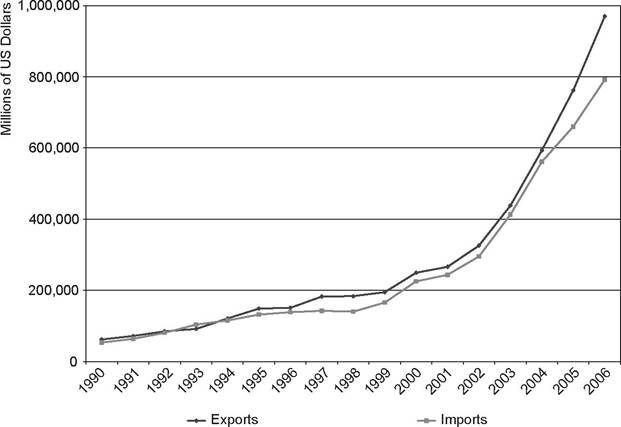

Their computational general equilibrium model actually implies continued deterioration in the US bilateral trade deficit when allowing for renminbi revaluation of up to 12%. Meanwhile, Barrell, Holland, and Hurst’s (2007, p. 10) recent examination of the effects of a simulated 10% appreciation in the renminbi within their world model suggests only a very short-lived reduction in China’s overall trade surplus - leading the authors to conclude that “the policy driven structural factors that have given China a current account surplus are largely independent of the exchange rate regime.”[23] Lardy (2005b, p. 136), in considering a more drastic 15% to 25% revaluation of the renminbi against the US dollar, suggests that even a move of this magnitude would do no more than slow the rate of increase of the bilateral US-China trade deficit.9According to US statistics, China’s overall current account surplus reached $US 238.5 billion in 2006, rising from $US 160.8 billion in 2005 and representing approximately 9.1% of its total economy, up from 7.2% in 2005, but still not the largest in the region in relative terms. Elsewhere within Asia, Singapore’s current account surplus was 27.5% of its economy in 2006, for example, whereas Malaysia’s was 15.8%, and the Hong Kong SARweighed in at 10.2% (International Monetary Fund, 2007). The tremendous growth in China’s imports has, in fact, generally not lagged far behind the more-widely-noted surge in export performance since the 1990s - although the gap did widen over the 2004-2006 period (see Figure 2.3). China’s overall trade surplus in 2006 actually combined an increased $US 232.5 billion surplus with the United States with a mere $6 billion surplus with the rest of the world. If all the imbalances were on the Chinese side, it would be hard to explain why the United States has continued to run large deficits with the rest of the world as well as China, whereas China’s “excess” surplus essentially disappears once US imports from China are removed from the equation.

US statistics on China’s bilateral trade surplus with the United States are themselves almost certainly overstated because of transshipment of goods via Hong Kong. Discrepancies arise if goods reexported from Hong Kong are mistakenly classified as if Hong Kong were their final destination. For example, US goods exported to China via Hong Kong may be erroneously reported in US customs statistics as an export to Hong Kong while also erroneously recorded in Chinese customs statistics as an import from Hong Kong. Schindler and Beckett (2005) find that most of the discrepancy between US and Chinese trade statistics is removed by correcting for such

certainly seem more justifiable than the repeated attempts to dictate the value of China’s currency.

9 The effects would admittedly be magnified if such a Chinese policy move triggered a more general upward adjustment of other Asian currencies. It is unclear whether any such widespread reaction would emerge in practice, however - with the July 21, 2005, Chinese revaluation seen by Ogawa and Kudo (2007) as having only limited and quite mixed effects on other neighboring currencies. What if Hong Kong, Korea, Malaysia, Singapore, Taiwan, and Thailand did, in fact, all follow a hypothetical freeing of the renminbi exchange rate against the dollar? Laurenceson and Qin (2006, p. 202) emphasize that even a 25% collective appreciation in their currencies could only reduce the overall effective dollar exchange rate by approximately 5%, given that their share of total US trade remains little more than 20%.

Figure 2.3. China's Exports and Imports Since 1990 (in million of US dollars). Source: International Monetary Fund.

distorting effects arising from Hong Kong’s transshipping role. Based on Schindler and Beckett’s analysis, the Chinese numbers are understated just as the US numbers are overstated. After making further adjustments for factors such as reexport markups and trade in services, Fung, Lau, and Xiong (2006) estimate that the United States’ bilateral deficit with China was $US 170.7 billion in 2005, representing approximately 85% of the official US figure of $US 201.6 billion and 149% of the official Chinese figure of $US 114.2 billion.

Broadly similar ratios are implied by Schindler and Becket’s (2005) findings for 2003 data.The actual overstatement in the US figures could be still higher, however, after considering reselling to US-based parent companies by multinational corporations operating in China. Chinese Ministry of Commerce calculations suggested the degree of overstatement could have been 30% or more in 2004, with sales by US-funded enterprises operating in China reaching US $75 billion in that year (People’s Daily Online, August 12, 2005b). This reflects mainland China’s importance as a destination for foreign direct investment. Such activities may distort the reported trade position, not only by counting US affiliate reexports to the United States as Chinese exports, but also by treating US affiliate sales in China as purely domestic output rather than as US exports. Both US affiliate reexports and US affiliate sales in China have been growing strongly in recent years (see Li, 2006, p. 64).

Although these qualifications suggest that official US figures significantly overstate the extent of the underlying trade imbalance, this would still leave a substantial US-China bilateral deficit. No matter how much China’s impact may have grown, it has, however, been far from the only driver behind the burgeoning US current account deficit and the United States’ transition to a debtor nation. The United States’ $4 trillion net debt to foreigners was accumulated over many years and did not suddenly spring from any alleged recent exchange rate imbalance with the renminbi. Moreover, China’s relatively balanced trade with the rest of the world, contrasted with the United States’ massive trade deficit with the rest of the world, begs the question of whether it is really the renminbi that is too weak or the US dollar that is too strong. From the perspective of Fan Gang, a member of the People’s Bank of China’s monetary policy committee: “[T]he real problem the world faced was an overvalued dollar, not only against the renminbi but against all the leading currencies.”[24] [25]