RISK MANAGEMENT

The idea of risk management is not to increase the premiums but rather to optimize portfolios and minimize the losses under stress conditions. As we saw, defaults of higher rated borrowers result in higher losses than those of lower rated borrowers.

Risk mitigation only through diversification across loan grades can look different from what we might expect. Higher- paying, lower-rated contracts are essential to buffer investors against unexpected losses.Ideally, a portfolio under stress would have no losses. Yet, in the real world, even the carefully constructed portfolios of large banks incur losses under unexpected circumstances.

Contract Number

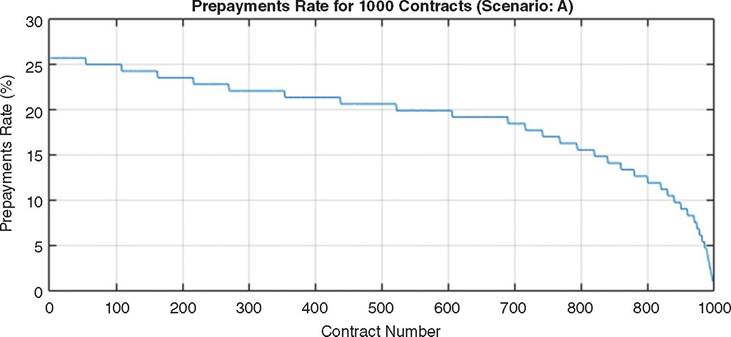

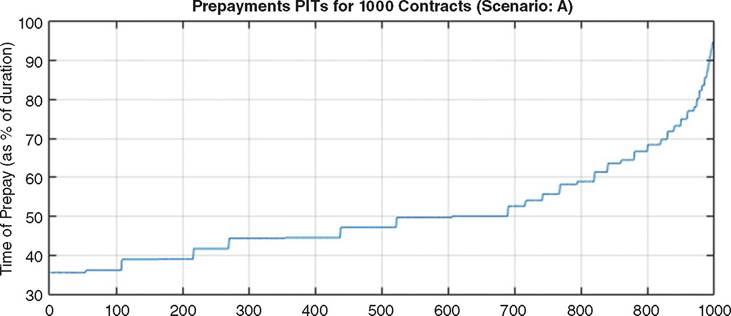

FIGURE 13.11 Prepayment rates as percentage of the remaining principal amount and prepayment point of times as percentage of individual contracts’ duration, applied for Scenario A, to each group, classified from A1 to G5 ratings, of the 1,000 contracts constructing the simulated portfolios

We learned this painfully in the financial crisis of 2007/8. Banks thought they had perfectly mitigated all risk, but their assumptions turned out to be wrong. To use this as an excuse to forgo risk modeling of marketplace loan portfolios would be missing the point. Sure, banks used models and they still incurred losses in the end. However, they overestimated the value of the assets on their books, they overestimated the performance of high-rated assets under stress, and they underestimated the impact of market and counterparty risk on their portfolios. Their models were too optimistic in their expectations, which required the intervention of the central bank to bail out many banks. In a nutshell, banks used the wrong models and they used them in the wrong way.

As the saying goes: “A fool with a tool is still a fool.” Underestimating risk using advanced models and systems with poor parameters is unsustainable. We can learn from past mistakes to construct and understand better the risk models and take into account

Contract Number

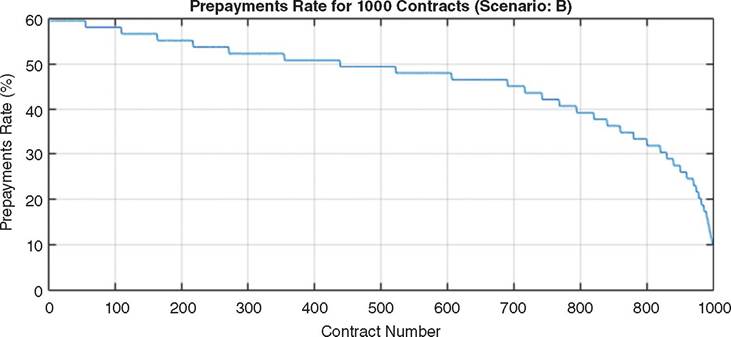

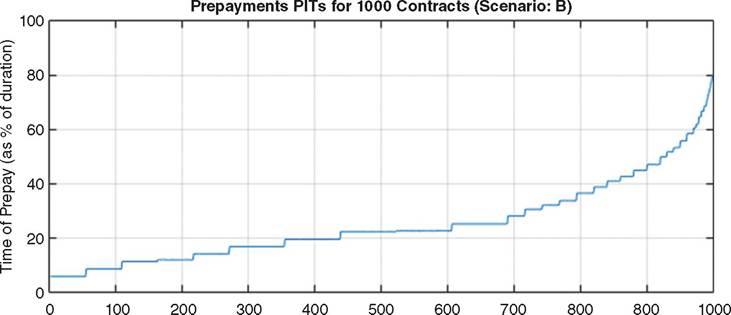

FIGURE 13.12 Prepayment rates as percentage of the remaining principal amount and prepayment point of times as percentage of individual contracts’ duration, applied for Scenario B, to each group, classified from A1 to G5 ratings, of the 1,000 contracts constructing the simulated portfolios

more severe stress scenarios. The credit sector can only profit from this. This is true for the credit sector beyond marketplace lending, including the entire financial system.

When regulators look at credit exposure today, they mainly request use of determinist stress scenarios rather than relying on VaR models. Because the central bank and tax payers bear the losses of financial institutions in the end, regulators want to avoid unexpected losses. Regulators want to see portfolios with no losses, even in stormy markets.

It is true that it is not the lending platforms but the individual lenders who hold this exposure on their books. Nevertheless, if the asset class at large suffers, the originators should at least know the extent of the losses that the loans they sold to investors might incur.

As we pointed out in Chapter 11 about concentration risk and systemic exposure, regulators will want to understand the cumulative losses of the asset class to accurately model the impact they could potentially have on the economy at large. If regulators looked at the asset class

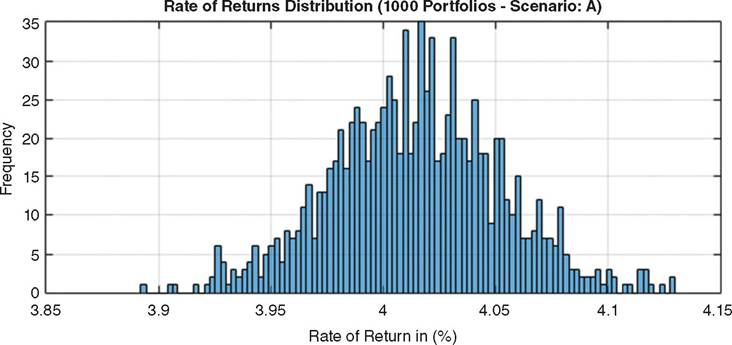

FIGURE 13.13 Distribution of the rate of returns under stress Scenario A: Stressing the spreads one notch

with the same microscope they apply to banks, they will want to know that risk-free rates and spreads can absorb expected losses.

Regulators could also inquire into how lenders structure their current and future operations to survive in times of increased stress. Unless lenders have enough capital to remain liquid under stress conditions, they are vulnerable.13.5.1 Operational risk

Even though it is not part of the analysis, marketplace platforms have operational risk. Platforms follow regulations for operational risk, which ensures they follow know-your-customer (KYC) procedures to verify the identity of borrowers and lenders. However, lenders cannot rely on deposit insurance for their loans. At the same time, the larger platforms have safeguards in place where an independent party takes over the servicing of the loans in case something

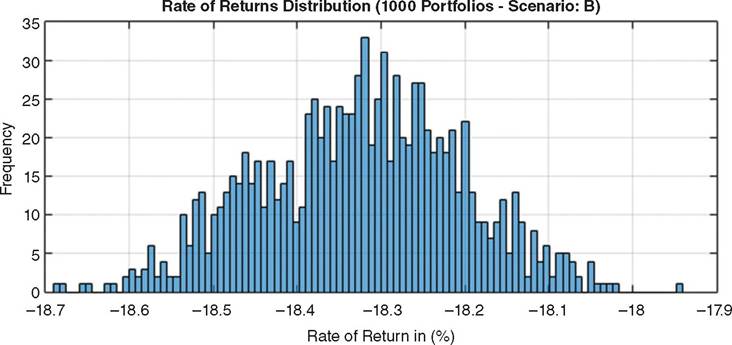

FIGURE 13.14 Distribution of the rate of returns under stress Scenario B

should happen to the platform. Regardless, in case of bankruptcy of a platform, lenders will have no recourse against the platform. Operational risk is less of an issue today because the larger platforms have proven their worth. Lending Club, for example, trades on the NYSE and is valued at roughly $8 billion. Such an operation will hardly disappear overnight. Bankruptcy is not around the corner for the well-established marketplace lenders, but a financial crisis could change that. Lenders should be aware that some operational risk persists. Operational risk can cause high losses with a low probability, which could impact the value of the whole portfolio.

13.5.2 Likely overestimation of borrower quality

in marketplace lending

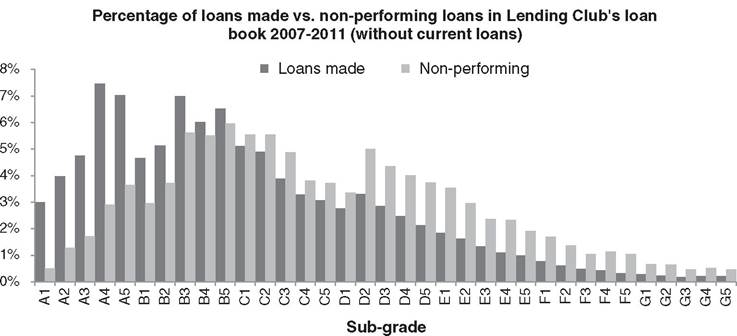

An analysis of the expected probability of default in Lending Club's loan book of 20072011 indicates that the credit scoring algorithm used by the platform slightly overestimates

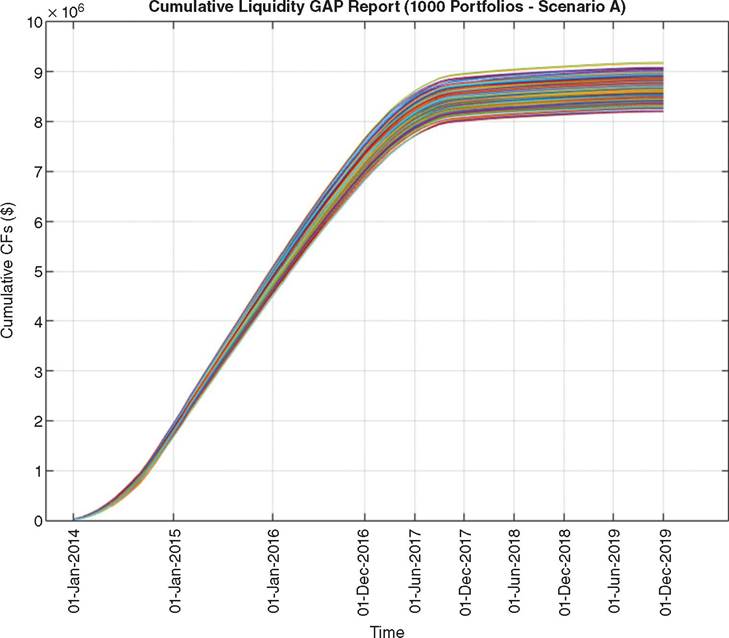

FIGURE 13.15 Distribution of cumulative liquidity GAP reports under Scenario A

borrowers of the lower loan grades.

Compared to the number of loans issued, the platform incurred a disproportionate amount of losses in 2007-2011 from borrowers with medium grades, and19 the probability of default is inconsistent with their grading system of borrowers. Perhaps this has to do with the fact that marketplace lenders never downgrade a borrower, even if his loan becomes delinquent. Figure 13.20 shows how the frequency of ratings diverges with the frequency of defaults.In Part One of this book, we raised the question as to whether marketplace lending platforms serve as a storefront for subprime loans that hedge funds and banks are more than happy to take off their hands. Lenders like to point out that they mainly lend to borrowers with high credit scores. Regardless, almost 40 percent of all new loans for autos, credit cards and personal borrowing in the U.S. went to subprime customers during the first 11 months of 20 1 4.20 This is the highest level since 2007, when subprime loans represented 41 percent of consumer lending outside of home mortgages. Somebody must be underwriting these loans. For instance, online lending resource Biz2Credit underwrote roughly half of its loans to subprime borrowers in 2014.21 Credit bureau Equifax defines subprime borrowers as those with a credit score below 640 on a scale that tops out at 850. Some marketplace lenders accept only borrowers with higher scores, others accept subprime borrowers.22

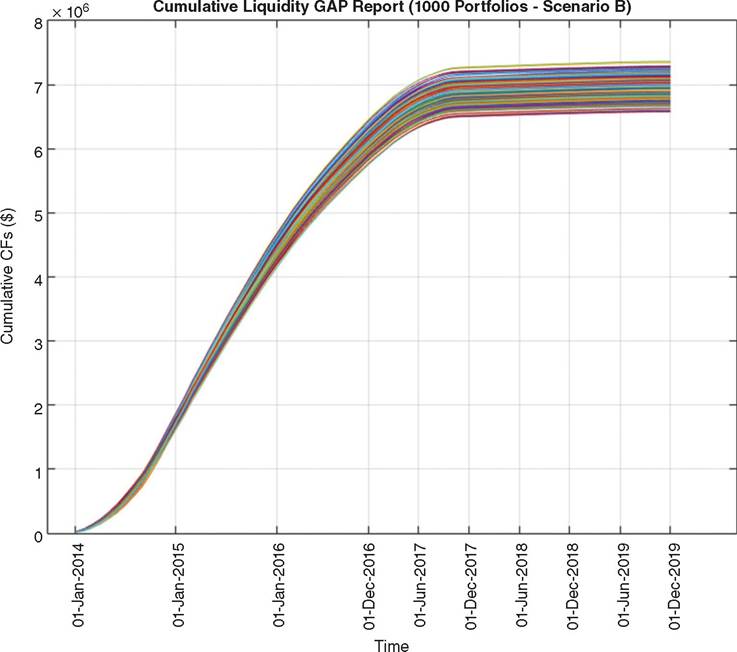

FIGURE 13.16 Distribution of cumulative liquidity GAP reports under Scenario B

Even though marketplace loans—like any other investment—come with certain investment risks, the comparison with subprime loans that stood at the center of the financial crisis 2007/8 is not entirely fair. The largest amount of credit that borrowers can get on a marketplace lending platform is $35,000 at the time of this writing.

This is relatively modest compared to the average subprime loan in the run up to the financial crisis. It is also important to remember that marketplace loans only make up a tiny fraction of the credit markets.Regardless, most marketplace borrowers use their loans to refinance their credit card balances at better rates. Marketplace lenders do check borrowers’ credit scores and update their credit scoring algorithms often. Additionally, they use alternative data—such as consumers’ monthly bill payments—and so-called fringe alternative data—posts and connections on social networks—to determine borrowers’ credit worthiness. Even though the predictive value and fairness of fringe alternative data are up for debate, fringe alternative models attempt to fill in the gaps that freeze some consumers out of the credit markets, reaching even further than mainstream alternative models. These underwriting standards are a long way from what banks demand from their creditors, but they are a step up from those of the fly-by-night stall in the mall that sold subprime loans by the dozen.

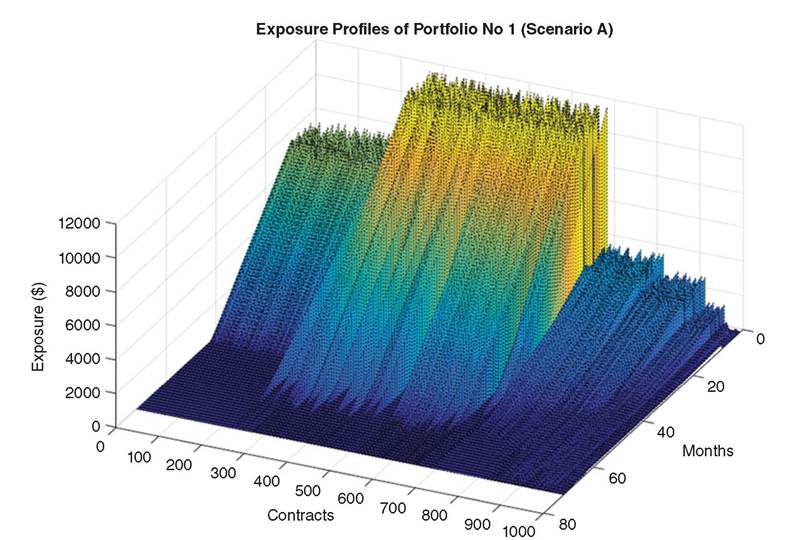

FIGURE 13.17 PortfolioexposureforScenarioA

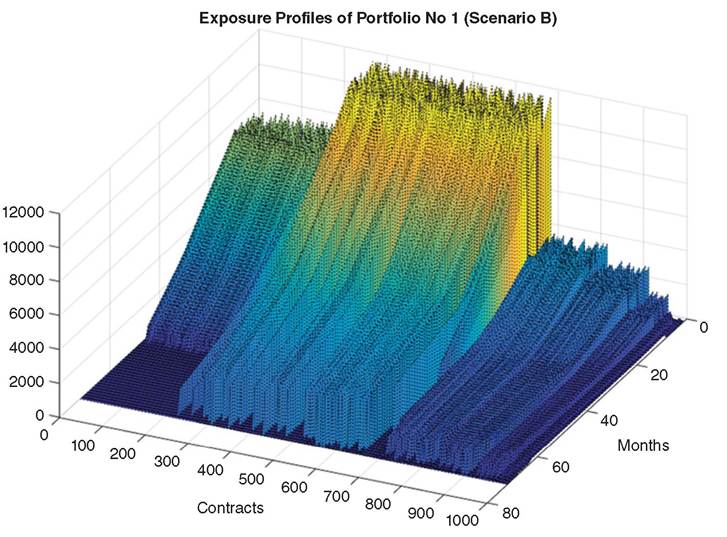

FIGURE 13.18 Portfolio exposure for Scenario B

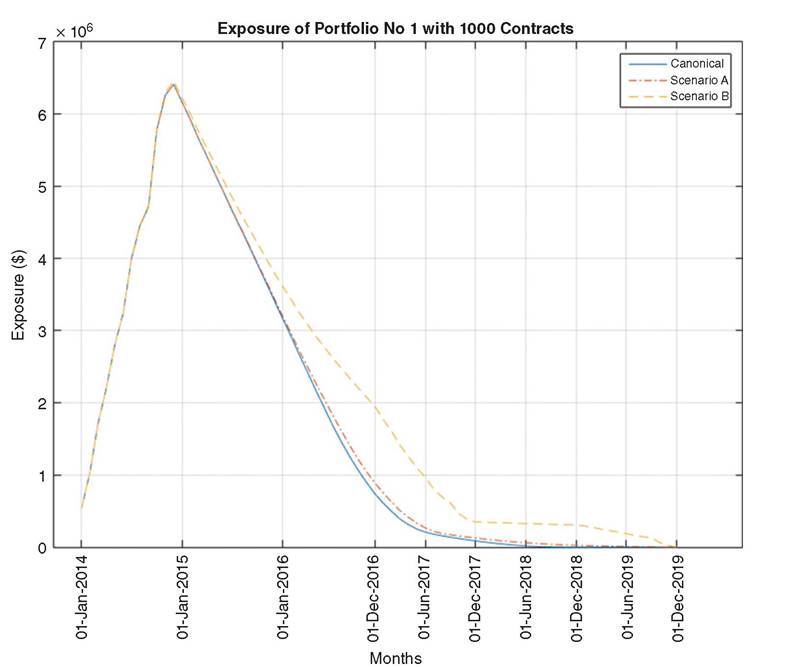

FIGURE 13.19 Evolution of the portfolio exposures under three scenarios: Canonical, A and B

Regardless, the fact that marketplace loans are uncollateralized makes them risky, and predictions about the actions of borrowers under stress are difficult to make. Even the pioneers among the marketplace lenders have only lived through one recession so far. How the business model of marketplace lenders will fare in future financial crises is unknown.

Borrowers may honor their loan agreements or they may default en masse with little consequence because their loans are uncollateralized. This would be a disaster for both individual lending platforms and the entire sector.Every loan comes with investment risk. Even bank loans with the highest rating and high-quality collateral can default. Even though a certain degree of risk is necessary to have meaningful returns above the risk-free rate, banks avoid uncertainty at all costs. When they can assess risks beforehand, they can manage them. When the risks are unknown, they cannot. Marketplace lenders, on the other hand, do very little to remove the high uncertainty that exists in their loan books. Even though they like to point out that they lend to borrowers with high credit scores, they still originate a healthy number of loans with a subprime grade. Furthermore, some of the information that borrowers provide is not even verified. This adds unnecessary uncertainty into the equation. Sensible lenders will sooner or later ask marketplace lenders to improve the quality of borrowers to drive down counterparty risk and default risk. For a lender who has diversified his loan portfolio across hundreds of loans, individual defaults may not matter. Nevertheless, every default that could have been avoided by better screening borrowers is unnecessary.

13.5.3 A note on portfolio restructuring and optimization

There is a sweet spot in the number of loans in a portfolio of marketplace loans. Beyond a certain point, adding more contracts reverts performance to the mean which actually reduces the return. This is the case because large portfolios become concentrated as counterparties are acting in similar ways. The recommendation to diversify across 200 contracts with certain scales of ratings is too general; it may work under normal conditions, but if there is stress in the system, a portfolio that invested in fewer selected loans may actually outperform. Because interest rates are high, investors can make profits in good times when there are few defaults. Yet, the interest income will fail to cover losses when they occur under less than perfect conditions. If we had more information about borrowers, we could analyze the correlation between them. This would give a more comprehensive overview, and we could accurately model concentration and systemic risks. Platforms have this information, and they can easily investigate how and where credit exposure concentrates. Ideally, we would have this information from more than one platform, so we could stress the entire market of online loans in general.

The ability to restructure portfolios is the most straightforward solution to making marketplace loans more resilient in times of market stress. If platforms perform good analytics, they can allow different durations for contracts; by simulating the performance under different assumptions, they can play with the duration and the loan amount to optimize the performance of a loan. When the market is likely to come under stress, platforms should shorten the duration of loans and readjust their interest rate. Platforms should define the rules under which loans perform best. To leave this up to the investor fails to take into account that most retail investors have no means to accurately model and understand marketplace loans. Yet for platforms, additional analytics like the ones we outline in Part Two of this book are relatively straightforward to implement. Loan originators should make sure that contracts are profitable under various conditions that go beyond ideal circumstances.

13.5.4 A note on collateral and hedging exposure

When defaults occur that exceed what originators expect under normal conditions, loan portfolios are at a high risk of performing badly. In our analysis, we used interest income as collateral. However, marketplace loans could benefit from other forms of collateral as well. Especially when they lend to small businesses, several ways to collateralize exposure are possible. Some marketplace lenders already move into auto loans, others offer refinancing of student loans. It will only be a matter of time before marketplace lenders fund the first mortgage. Having collateral in the mix would drastically improve the performance of loan portfolios under stress.

For medium-term high fixed-interest uncollateralized contracts, the default probability will almost always be too high, even when the slightest sign of stress in the market appears. Under stress, lenders can either increase interest or hedge their exposure. It would be relatively straightforward to design a derivative to cover the losses for lenders in stress conditions, and this would make the most sense when we have achieved secondary market liquidity of marketplace loans. Originators could add the premium for this insurance to the interest rate that borrowers pay, or they could offer the insurance as a service to lenders for a fee. In any event, adding insurance should hardly increase interest too much, but it could potentially transform the asset class. Increasing the interest rate for loans is a fine balance: too high an interest rate will result in the same situation that bank lending imposed on marginal borrowers. However, if platforms do nothing and simply wait for the first crisis to occur, they risk tarnishing the sector before it can develop its full potential. If platforms do nothing and pursue a business-as-usual strategy, lenders will suffer losses under stress with certainty.