Semi-annual interest

The example of Bluebird is based on the assumption of annual interest payments. This makes initial understanding easier and reflects the reality for many types of bond, particularly internationally traded bonds.

However, many companies and governments around the world issue domestic bonds with semi-annual interest payments. The rate of return calculation on these bonds is slightly more complicated.Example 13.5

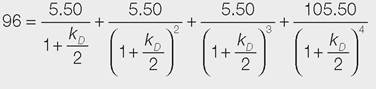

Redwing has an 11% bond outstanding that pays interest semi-annually. It will be redeemed in two years at ˆ100 and has a current market price of ˆ96, with the next interest payment due in six months. The yield to maturity on this bond is calculated as follows:

Cash flows

| Point in time (years) | 0.5 | 1 | 1.5 | 2.0 |

| Cash flow | ˆ5.50 | ˆ5.50 | ˆ5.50 | ˆ5.50 + ˆ100 |

Taking the capital gain (ˆ100 - ˆ96 over two years) as about 2% per year, the IRR/2 would be roughly 5.5% plus 1%, 6.5% for six months. To obtain a more accurate yield to maturity figure we need to solve for kD allowing for the semiannual compounding of interest received:

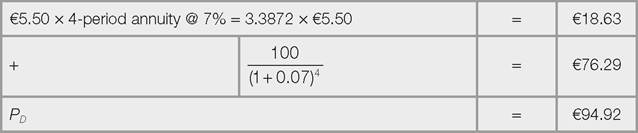

More precisely, at a rate of 7% for kD/2, Pd equals ˆ94.920:

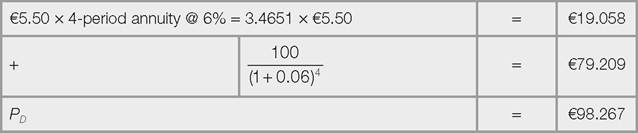

At a rate of 6% for kD/2, Pd equals ˆ98.267:

The IRR of the cash flow equals:

The IRR needs to be converted from a half-yearly cash flow basis to an annual basis (an effective annual yield).

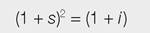

The relationship between semi-annual interest and annual interest is:

where s is the semi-annual rate and i is the annual rate, i.e. interest received at the half year is compounded.

Thus:

In the case of Redwing: