Yield to maturity versus rate of return

It is important to understand the difference between yield to maturity and rate of return.

The yield to maturity is the return that would be received given the current rate of coupon and market price, and assuming the bond is held until maturity.

The rate of return is the rate that an investor actually receives between the purchase and when their bond is sold before maturity, or on reaching maturity.

Yield to maturity and rate of return are only the same if the time to maturity is the same as the holding period.

We can illustrate this as follows.

Example 13.6

Assume that Tom has just bought four bonds. The maturity dates are 1 year from now, 5 years from now, 10 years from now and 20 years from now. For the sake of simplicity assume that all the bonds are trading in the secondary market at ˆ1,000, which is also their par values to be paid at maturity, and that they each offer a yield to maturity of 6% (annual coupons are ˆ60).

Tom is planning to sell all of the bonds in a year from now. The question is, what rate of return will he receive if between now and then the yield to maturity that investors demand in the secondary market on these bonds rises from 6% to 10%, or falls to 2%? (Again, assume for the sake of simplicity that the yield to maturity of 10% or 2% is the same regardless of whether the bond has a short or a long time until maturity - there is a ‘flat yield curve' as discussed later.)

We'll concentrate on the 10% interest rate level first.

One-year bond

In the case of the one-year bond Tom does not have to sell in the secondary market; the issuer redeems the bond at its par value of ˆ1,000. Tom also receives the coupon of ˆ60, so the rate of return he gains is 6% (60/1000). This is the same as the yield to maturity when he bought the bond.

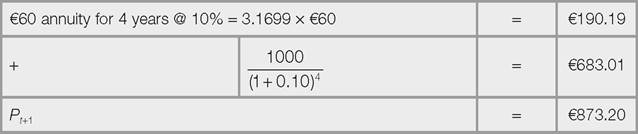

Five-year bond

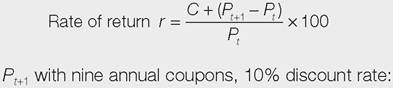

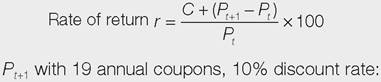

where C = coupon rate

Pt+1 = price of bond after one year

Pt = price of bond at the start.

To calculate Pt+1:

Pt+1 = four annual coupons discounted to time t + 1 (ˆ60 ? annuity factor for four years at 10%) plus the redemption amount discounted back to t + 1:

So, while the yield to maturity at time t was 6%, the rate of return over the one-year holding period was -6.7% because of the large capital loss on the bond.

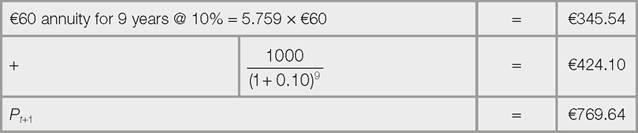

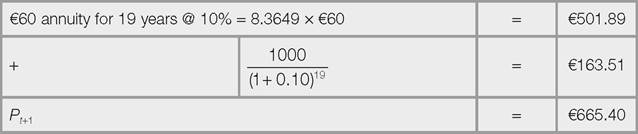

It is even worse for the 10-year and 20-year bonds. If yields to maturity rise from 6% to 10% over the holding year then these bonds can be sold for only ˆ769.64 and ˆ665.40 at time t + 1:

Ten-year bond

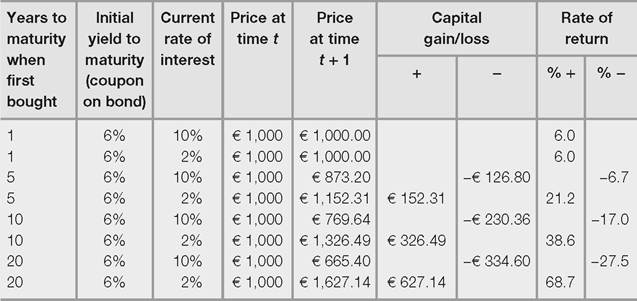

So far, poor Tom. Because interest rates have risen, the value of all his bonds (except the one-year bond) has fallen and he ends up with a considerable capital loss, ˆ691.76 in total.

If, however, interest rates fall by 4% points to 2%, then Tom is in luck. Each of his bonds (except the one-year bond) is worth far more, giving him a gain of ˆ1105.93 on top of his coupon at the end of one year. The individual bond returns are shown in Table 13.1, for both a rise in interest rates to 10% or a fall to 2%. An interest rate change of 4% is quite dramatic; typically interest rates change by far smaller amounts, but this example demonstrates the different volatility of bond prices and how important it is to understand bond pricing.

Of course, if each of the bonds /s held until maturity Tom will receive a 6% rate of return on all of them, because they will then be redeemed at their par value.

Table 13.1 Rates of return on Tom's bonds given market interest rate changes and sale after one year

Again, we have an illustration of the inverse relationship between the price of a bond and the yield to maturity. We also have the (when first encountered) counter-intuitive result that a rise in interest rates results in a poor bond investment - Tom will not be happy with the return on his bonds if interest rates rise, but if they fall he will benefit.