TECHNOLOGICAL FACTORS

Cheap and ubiquitous computing power, a revolution in Big Data and analytics, faster technology adoption, the rapid expansion of the internet, the boom in mobile screens, and software platforms that jump-started network effects, are the main technological factors that enable online lending.

Let's examine each of them a little more closely.3.1.1 Cheap and ubiquitous computing power, coupled with

a revolution in Big Data and analytics

The oft-cited Moore's Law—the fact that the performance of computer chips doubles approximately every eighteen months, which decreases their relative cost2—is well documented, so

| TABLE 3.1 Technological, social, and structural factors that empowered online lending | |||

| Technological factors | Social factors | Structural factors | |

| ■ | Cheap and ubiquitous computing | ■ Digital connectedness | ■ Stricter banking |

| power, coupled with a revolution | and friendships | regulation | |

| in Big Data and analytics | ■ Impatience with the | ■ Mergers lead to | |

| ■ | Faster technology adoption | traditional | disappearance of smaller |

| ■ | Internet proliferation and | know-your-customer | banks, with decreased |

| acceptance, security and | process | access to credit for | |

| comparability of services | ■ Sentiment against the | consumers and SMEs | |

| ■ | The boom in mobile screens, | established financial | ■ Low interest rate |

| ■ | open architecture, tracking of mobile users Network effects, intermediary platforms that connect lenders and borrowers | sector | environment |

we just touch it on the surface here.With teraflops of computing power available at bargainbasement prices, machines can do what seemed impossible a few decades ago.

Author Ray Kurzweil extended the law of accelerating returns to any information technology. Kurzweil states that at the core of accelerating returns is information. Once information powers an industry, its price/performance doubles approximately annually without stopping.3 We have already learned that peer-to-peer networks thrive on information. Additionally, computers have a long history in finance. It is only natural that exponential increases in cheap computing power have the potential to usher in a new era for financial services across the board.3.1.2 Faster technology adoption

Concurrent with exponential growth, adoption rates of technology have accelerated. Author Michael DeGusta points out that electricity needed 30 years to reach 10 percent adoption. Telephones took 25 years for the same adoption rate. However, tablet devices achieved it in less than 5 years. It took another 54 years until telephones became widely adopted, with 40 percent penetration. Smartphones, on the other hand, accomplished a 40 percent penetration rate in just 10 years, assuming that the first smart phones were PDAs that could make phone calls, which emerged in 2002.4 Networked devices in the hands of nearly everyone are new in the history of humankind. They are the great enablers of our time. Smartphones give users access to a portable computer anywhere they go. Better yet, the operating systems of smartphones have a plug-in architecture that allows anyone with coding skills to program apps that users can download onto their devices. Smartphones thereby create global open networks that allow their owners to interact with each other easily and inexpensively. They are ideal for painless interaction between peers. With faster adoption of technology, consumers unlock network effects faster.

3.1.3 Internet proliferation and network effects

The exponential growth in adoption rates of new technology has given rise to powerful network effects: the more people use a technology, the more benefits they derive from it.

Instead of

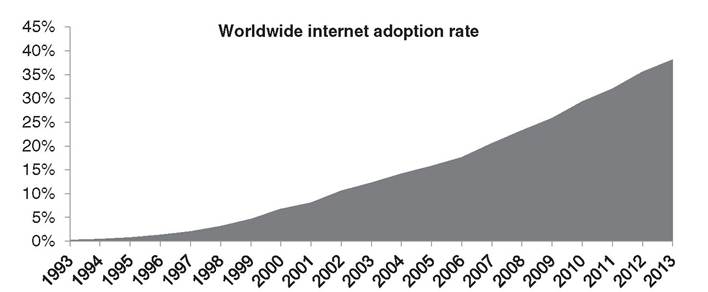

FIGURE 3.1 Worldwide internet adoption rate

Data source: World Bank

increasing linearly, the value of networks rises exponentially, as Metcalfe’s law describes. The law is more a rule of thumb that states that the value of a telecommunications network is proportional to the square of the number of users of the system (v ~ n2).5 This rule describes the network effects of networks such as the internet and social networking. Just imagine there was a group of twenty people of whom only two owned a smart phone with a chat app. They were the only ones who could chat with each other. However, if all twenty people had the app on their phone, you have a marketplace in the making. The greater the number of connected users in the network, the more valuable the service becomes to the community.

This is especially true in social networks and similar platforms. Once everybody uses them, their utility mushrooms. The space of online payments and transactions is no exception. The more people use and accept such payments, the more useful the service. As a result, the sector signals high profitability, which attracts new entrants into the market and drives down costs for customers. This jump starts a virtuous cycle that speeds up change and adoption and improves services. Of course, a prerequisite for online services to take off is a high proliferation of stable and secure internet service. Figure 3.1 shows the worldwide internet adoption rate with close to 40 percent of the world population online—a market of around 2.6 billion people who are accessible with one inexpensive distribution channel.6

3.1.3.1 Online security and trust Nexttotheproliferationoftheinternetandnetwork effects, its acceptance as a secure communication channel is just as much a requirement for customers to use it for financial transactions. While security was an early concern with online banking, most banking platforms today use industrial-strength encryption and proprietary safety features.

In the case of a security breach, they are relatively quick to respond. The risk to customers of using internet banking today is minimal. The same applies to financial services provided by (reputable) third parties. Sure, cybercrime is a serious concern, and some internet investment schemes or alternative currencies have turned out to be scams. But so have some reputable New York hedge funds that were beyond reproach until they unraveled. The technology to make an online service secure certainly exists today. And customers trust it all the same—whether a reputable bank, credit card company, or large brand name stands behind it.3.1.3.2 Comparability and transparency Using the internet to look for banking services brings many advantages to customers. Search costs decline because services and rates are instantly comparable with free information. Transaction costs go down as technology automates processes in the back office. Banks today are in direct competition against each other and other players. When a bank offers the ability for online loan applications, customers of other banks will demand the same. Otherwise, they are free to vote with their feet and switch to the more accommodating bank. This has increased transparency, which is much to the disadvantage of the traditional financial sector. A significant factor in the banks' business model was the undisclosed fees, which appeared nowhere else than in the fine print of an application that the customer had to sign right there in the branch. Very few customers read the fine print in any contract they sign, but today they no longer have to take the word of their banker at face value. There is always a blogger or journalist who has compared different offers and has written about it for all to see. For those who know how to use information available online critically, research has become much easier, and financial products have gained in transparency.

3.1.4 Theboominmobilescreens

The next liberating technology factor for the consumer was personal mobile computers.

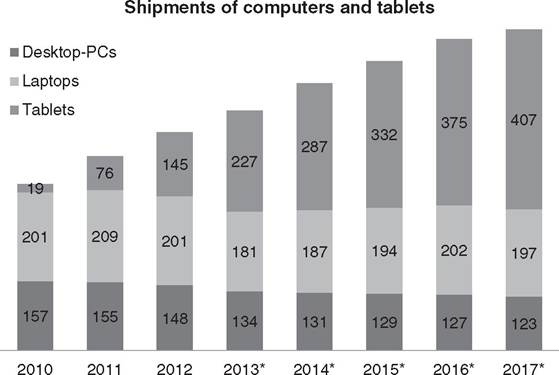

Tablets and smartphones are a boon in several ways for the consumer. Mobile computing has brought several advantages, mainly location independence, open software architecture, and the ability to generate user data. The first advantage of mobile screens is the ability of users to connect to information anywhere they may find themselves. While internet users of the past had to sit in front of a stationary desktop computer that connected to the internet through a cable, mobile devices can connect via wireless networks in public places or through a data plan. Internet surfing has become as convenient as phone calls. More and more people use the internet through mobile devices, and the number of shipments of mobile screens is forecast to surpass the number of desktops and laptops in 2015, as can be seen in Figure 3.2.7

FIGURE 3.2 Forecast for global shipments of tablets, laptops and desktop

PCs from 2010 to 2017 (in million units)

Data source: Statista

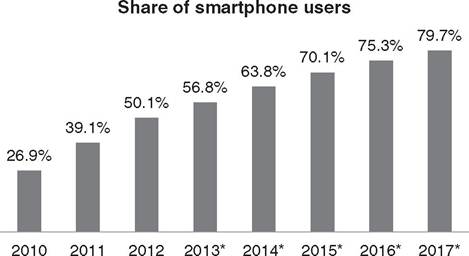

FIGURE 3.3 Smartphone users as a percentage of all mobile users in the U.S.

Data source: Statista

While a customer is sitting in a bank, looking over the loan documentation, she can compare the terms with other offers right there in the branch on her tablet. If there is a better loan on offer next door, she can get up and take her business elsewhere—a nightmare for every banker. There are more uses of smartphones we have not even imagined yet, and the adoption rate of smartphones is forecast to continue, as Figure 3.3 shows.8

3.1.4.1 Open architecture of mobile operating systems A second advantage of mobile devices is their open architecture. Anybody can code an app that is instantly available for download on a variety of mobile devices. Whilst previously it was expensive and lengthy to develop software, app development has driven this cost down to a few thousand dollars.

There are still backend costs to consider but, even so, mobile first startups can realistically launch competitive services that rival a large international bank for a few hundred thousand dollars. When the idea is strong and enough people are interested in using the service, the barriers to entry are lower than ever before.3.1.4.2 Tracking of mobile users The third advantage of mobile computing is that it generates a lot of personal data. Most devices have a GPS sensor embedded, which means every step its owners take can be recorded and tracked. The operating systems of mobile devices also transmit user data to the operator of an app. For example, some apps collect information about location, serial-number-like identifiers for the phone, and personal details such as gender and age. Marketing companies are collecting massive amounts of data on phone users, always teetering right at the brink of respecting the privacy of users. For financial service providers these data are extremely valuable. While it was difficult in the past to assess whether a borrower told the truth on a loan application, cross referencing between organically collected data may be helpful to verify such claims in a fraction of the time.

3.1.4.3 The next step: goodbye gatekeepers When we discussed peer-to-peer networks, we learned that they need a central administrator or Infomediary who organizes the information that peers need to transact. We then contrasted this with a supermarket that buys from sellers and sells to buyers, in the process marking up products and controlling access. The supermarket is an example of a network that is the opposite of peer-to-peer; a monopoly that controls interactions and is often the only way for people to trade in an economy. Of course, when an intermediary-oriented platform corners the market and pools information about most potential counterparties, it may become a monopolist just like the only supermarket in town. This has happened online, where powerful infomediaries are controlling the flow of information. Facebook, for example, makes little user data available to individual users, and Amazon will not disclose the identity of buyers to sellers on its marketplace. These are the monopolies of the digital age: their heavy use of technology and automation has driven transaction costs, but they still dictate terms and squeeze buyers and sellers to maximize their margins. While processes and data in online networks often still go through a central gatekeeper, the next step is to break down that barrier as well.

As soon as users connect directly to each other on a platform, with the data they are creating freely available to anyone, there is little need for a gatekeeper other than to keep the platform up and running. Marketplace lending platforms promise to be such intermediaries, and they might be the next generation of intermediary-oriented platforms. When we introduced peer-to-peer networks, we saw that it is in the nature of people to connect directly with each other in commerce. Platforms that facilitate this interaction globally have only become possible in recent years with all the technological factors in place at scale. In this sense, we are still in the early stages of business models that build on network effects and direct marketplace interaction. However, it is already clear that the peer-to-peer way of doing business is a course change from our current economic model. An omnipotent matchmaker who calls the shots and thrives on incomplete information between buyers and sellers will soon be a thing of the past. More and more challenges to the economic model of the gatekeeper at the center of transactions will arise in the near future. The disruption in financial services is just one of them.

3.2