SOCIAL FACTORS

Next to technological factors, social factors play an equally important role in the rise of FinTech and online lending in particular. The acceptance of digital connectedness and friendships, the impatience with the traditional know-your-customer (KYC) process, and an overall sentiment against the established financial sector are the social factors that empower online lending.

3.2.1 Digital connectedness and friendships

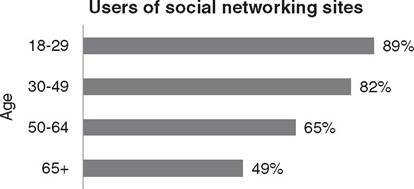

Author Sherry Turkle points out that today's young people have grown up with a digital network in a fully tethered life. They see robots and digital avatars no longer as inferior to real-world interaction as they take the power of online connectedness for granted. For today's digital natives, seeing the location of all their acquaintances within a ten-mile radius is a given.9 With this strong sense of digital connectedness, introducing financial services into the relationship is a small step, especially when it promises direct interaction between online friends. Trusting someone you have never seen face to face would have seemed strange a few years ago, but today, it is perfectly acceptable. Most people, and millennials in particular, take online communication at face value. Figure 3.4 shows the proliferation of social networking across different age groups.10 This is a strong enabler for online lending, where trust is essential.

FIGURE 3.4 Social networking site use by age group (January 2014)

Data source: Pew Research Center

3.2.2 Impatience with the know-your-customer process

As a counterpart to increased openness in online interactions, the know-your-customer process (KYC) of many banks has tightened in the years since the financial crisis of 2007/8. Standard protocol still demands a customer’s presence in the bank branch when interviewing for a loan.

Some banks offer online applications for potential borrowers to apply online. Regardless, at some point or other, the bank requires the borrower to step into a branch. Most banking documents require a handwritten signature. Many banks even record statements made by customers during the application process as digital audio files. Even opening a simple savings account can take hours this way, not counting the trip to and from the bank branch and time spent waiting for an account manager to be available. Such demands are in stark contrast to the way most people use the internet and their smart phones today, and they seem like relics from a time long gone. Author Brett King writes that banks fail to sell well online because of their onerous compliance and KYC processes. While banks always point toward regulations that require such practices, almost always the actual regulations around KYC require no physical distribution. Otherwise, online financial platforms such as Square and PayPal would simply not have been allowed to do what they did.113.2.3 Sentiment against the established financial sector

The perceived duplicity of banks galls many customers, young and old. Since the financial crisis of 2007/8, the sentiment against established large banks has soured even more. The ensuing global Occupy Movement against the 1 percent, including so-called “fat cat banks,” has hardly helped the image of the financial sector, which has lost much goodwill in the process. It is therefore relatively easy for new entrants to play on the misgivings of customers towards banks. This has helped the popularity of online lenders, who often come across as the “better, fairer banks.” Whether such claims are true is another question. Still, online lenders and marketplace lending platforms are careful to distance themselves from the established financial sector in their communications and corporate identity.

3.3

More on the topic SOCIAL FACTORS:

- An evolutionary analysis of multilevel governance mechanisms for SHD at the local level

- Experiences, Situations, Representations

- Agrawal M.. Textbook of Pediatrics. 3rd ed. — CBS Publishers,2025. — 973 p., 2025

- Fundamental causes of income differences

- The Three Pillars of Income Security

- Introduction

- Cattle Movement Networks in Uganda

- FIVE COMPONENTS OF LEGAL COMPETENCIES

- Somalia