THE HYBRID FINANCIAL SECTOR: THE OPPORTUNITY TO BUILD A HEALTHIER FINANCIAL SYSTEM

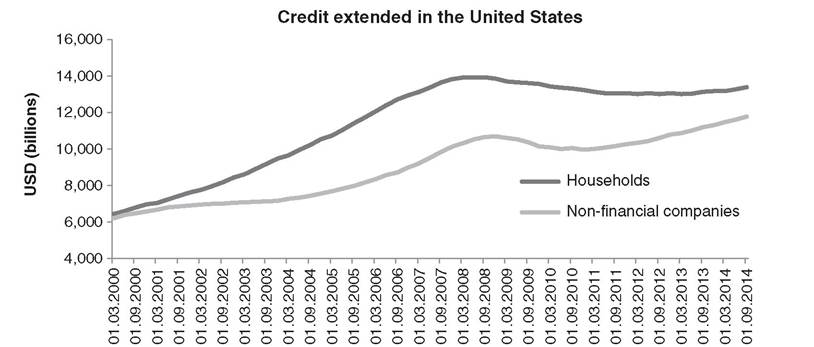

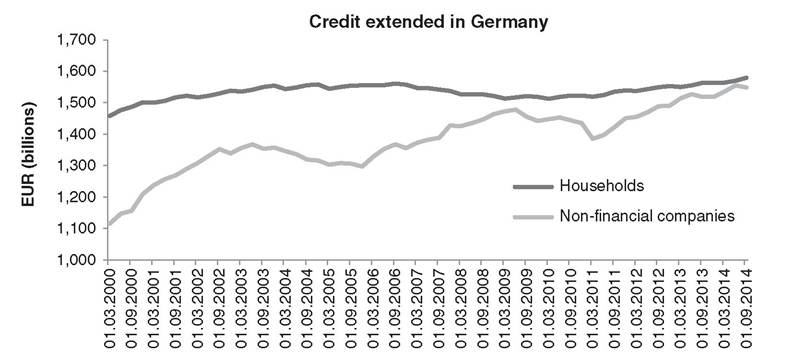

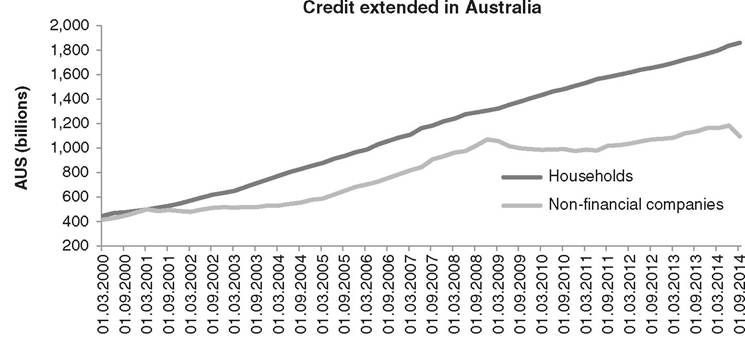

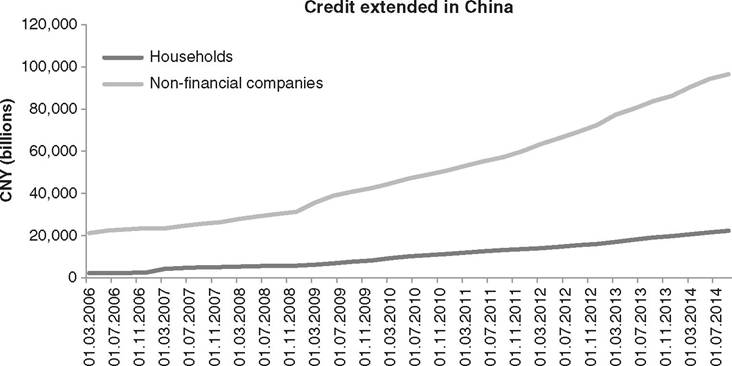

The financial crisis of 2007/8 has been an undoubted shock in terms of credit, both for lenders and for borrowers. Despite the crisis, nominal amounts of credit outstanding to households and non-financial companies have mostly been going up, as the figures show for the United States, the United Kingdom, Australia, Germany and China (Figure I.2, Figure I.4, Figure I.6, Figure I.8, and Figure I.10).

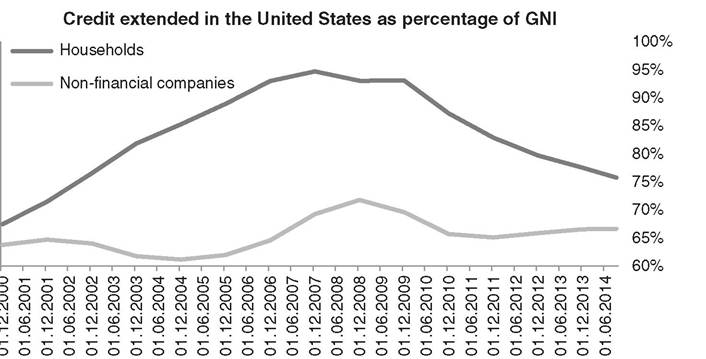

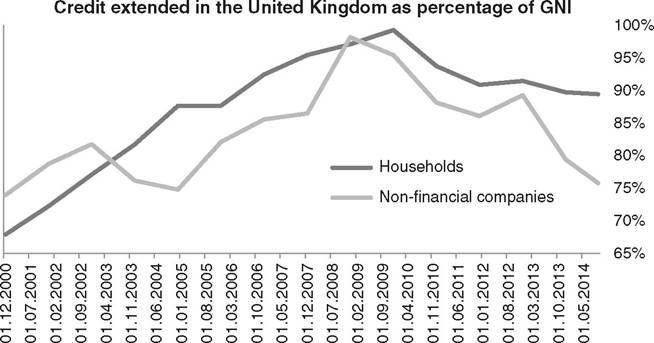

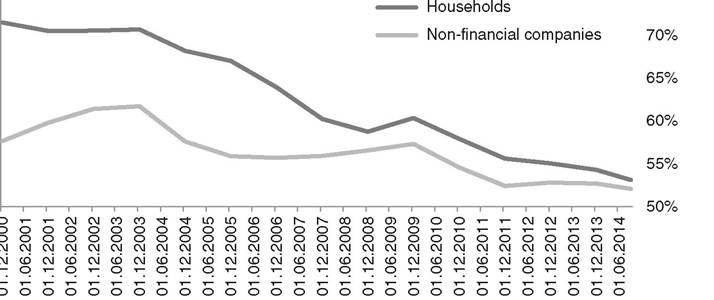

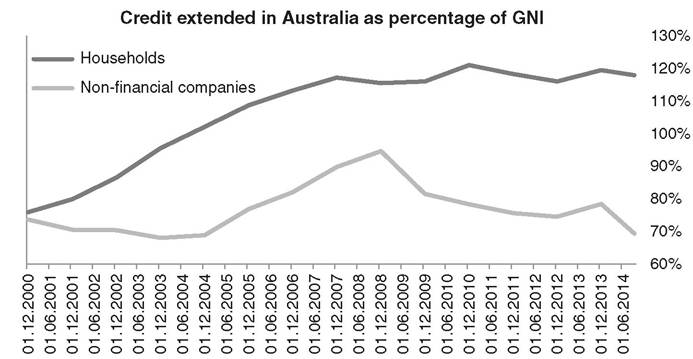

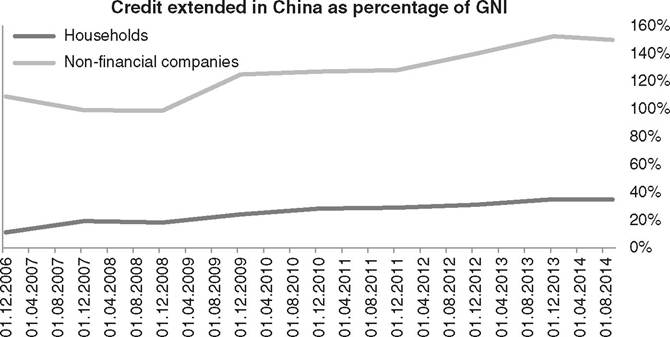

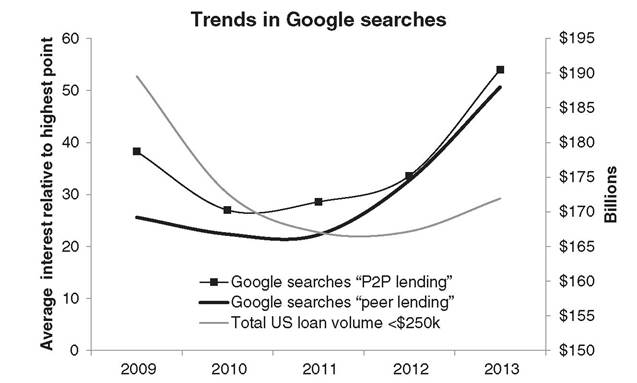

When we compare the amount of credit outstanding to the gross national income (GNI) of these countries, things look less promising: For all countries, with the exception of China, credit outstanding as a percentage of GNI has gone down across the board (Figure I.3, Figure I.5, Figure I.7, Figure I.9, and Figure I.11). It is certainly a good idea for countries to keep their debt in check, but at the same time, if firms and households cannot borrow, this will hamper growth in the longer term. Finding sources of credit for borrowers outside of the established channels therefore makes sense, as long as it will introduce no additional risk into the system.At the same time as tech startups began to stake a claim in the financial sector and small business loans have decreased, more people have searched for “P2P lending” and “peer lending” on Google (Figure I.12). One trend need not be a cause for the other, but it is clear

FIGURE I.3 Credit extended in the United States from all sectors to households and NPISHs and non-financial companies

Data sources: Bank of International Settlements (BIS) and World Bank for GDP and GNI data (GNI for 2014 is extrapolated with average growth rate of the previous three years)

that they have diverged in opposite directions in recent years, and online lenders have steadily increased the number of loans they underwrite.

While they are steadily increasing the numbers of loans they underwrite, financial technology startups ignore a large opportunity that exists in financial markets today: to use technology to make the financial system more resilient to external shocks. What the financial system needs is less a shuffling of the deck, with more unregulated new entrants, but more an evolved system that promises rewards to all stakeholders involved. Instead of building proprietary systems,

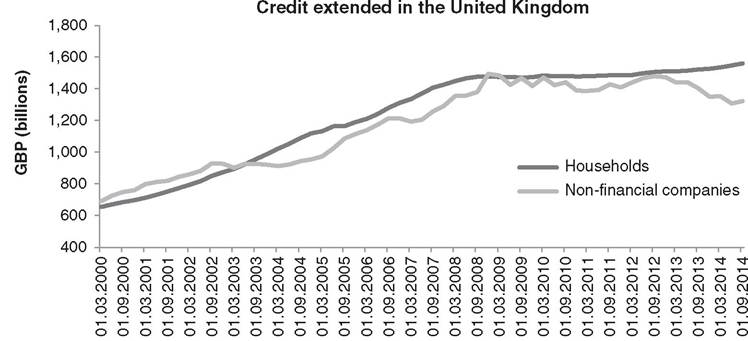

FIGURE I.5 Credit extended in the United Kingdom from all sectors to households and NPISHs and non-financial companies

Data sources: Bank of International Settlements (BIS) and World Bank for GDP and GNI data (GNI for 2014 is extrapolated with average growth rate of the previous three years)

financial technology innovators could reinvent how banking and lending are done at the core. This is hardly a question of building a better mousetrap, but of integrating systems to work together and address problems in a common language. As we saw in Figure I.10 and Figure I.11, which both show credit in China, households still hold far less credit than companies in emerging markets. This represents an enormous market potential. When FinTech startups find a new solution or a suite of new solutions that can serve the emerging middle classes of the world more efficiently than banks, the pie for all participants will expand. It is unlikely that

Credit extended in Germany as percentage of GNI

FIGURE I.7 Credit extended in Germany from all sectors to households and NPISHs and non-financial companies

Data sources: Bank of International Settlements (BIS) and World Bank for GDP and GNI data (GNI for 2014 is extrapolated with average growth rate of the previous three years)

market leadership in credit will be a question of a single bank or FinTech company cornering the market.

Investors and borrowers will most likely use a suite of services that blend into each other seamlessly. Instead of wasting time in competing against each other, banks and FinTech innovators could build the hybrid financial sector of the future together, today.An integrated view is only possible if innovation leaders understand how the financial system works. When they can integrate all existing parties and motivate them to evolve the

FIGURE I.9 Credit extended in Australia from all sectors to households and NPISHs and non-financial companies

Data sources: Bank of International Settlements (BIS) and World Bank for GDP and GNI data (GNI for 2014 is extrapolated with average growth rate of the previous three years)

system together, there will be radical change for the better. Without it, we see more walled gardens pop up that might confuse and cannibalize the existing system. Keeping in mind the evolution of the financial system and charting ways to design a more robust hybrid financial sector is the goal of this book. With this in mind, let's get started.

FIGURE I.11 Credit extended in China from all sectors to households and NPISHs and non-financial companies

Data sources: Bank of International Settlements (BIS) and World Bank for GDP and GNI data (GNI for 2014 is extrapolated with average growth rate of the previous three years)

FIGURE I.12 Google searches for “p2p lending” and “peer lending” and total volume of U.S. small loans below $250,000 outstanding

Data sources: Google, FDIC

NOTE

1. Nash, Ryan, and Eric Beardsley (2015) “The Future of Finance: The Rise of the New Shadow Bank, Part 1,” Goldman Sachs Equity Research.