TREASURY AND FUNDS TRANSFER PRICING (FTP)

So far in this chapter we have discussed value, liquidity, income, risk and the development of new businesses. The question now is who is coordinating them, managing the different types of financial risks and is responsible for the profit and loss of the institution? A key role in the financial institution is played by the treasury department.

In a sense the treasury department is a bank within a bank or, in other words, the heart of the bank which pumps liquidity to different business entities managing the value and income, balancing the assets and liabilities and mitigating financial risks. Let us explore now the main principles of the treasury.Just as a bank classifies deposits and loans differently in their balance sheet, from an accounting perspective, loans can be considered from the position of the lender and the borrower:

■ For the lender the loan is an asset where an income is received from the expected interest payments or trading activities.

■ For the borrower the loan is a liability that defines the obligation to pay interest expense.

In the banking system, liabilities represent the majority14 of capital, which the institution borrows from the markets and thus an obligation of future expense is defined. On the other hand, in lending this capital back to the market it becomes an asset where income is expected to be generated. Based on this model, assets cannot exist without liabilities and, therefore, both sides of the balance sheet have to be considered at the same time.

Regarding its loan business, the bank must make sure that:

■ It has access to capital markets to borrow funds to fulfil future expense obligations.

■ It lends capital to trustworthy borrowers in the market who will fulfil the loan obligations until the maturity of the loan agreement.

■ Assets and liabilities are balanced, over time, in a way that:

■ the value of the assets is higher than the liabilities,

■ the cash-inflows are higher than the cash-outflows, and

■ the expected income is higher than the expenses, which allows profitable operation.

■ Any losses can be absorbed and thus the financial system is stable and robust despite any risky conditions.

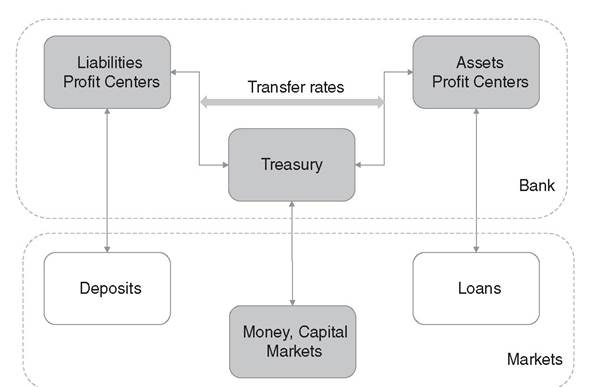

Links between financial contracts placed in the liability and asset sides are obtained via the funds transfer pricing system. To see how such a system works, assume a bank has three profit centers and FTP framework as illustrated in Figure 12.6, which has the following functions:

1. The liability profit center which is responsible to get deposits from the market.

2. The asset profit center which provides loans to the market.

3. The treasury department which acts as a bank within a bank.

One of the main functions of the treasury department of a bank is to manage the bank's balance sheet and to ensure that all departments in the bank can access the capital they need for their daily activities. As mentioned above, the goal is to maximize margins, manage risk and provide the necessary liquidity of funds. The management of risk especially has a high priority. The treasury is also responsible for the securitization of assets to free up equity capital. It may also interact with regulators who set rules, e.g., regarding capital requirements and liquidity.

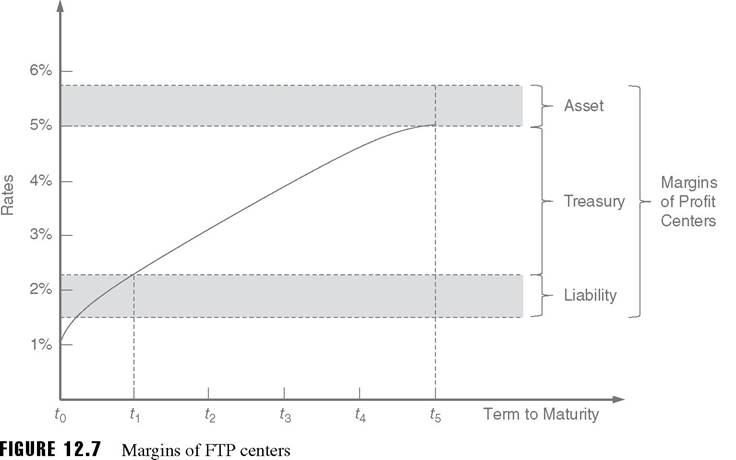

FIGURE 12.6 Profit centers and FTP framework

12.4.1 Funds transfer pricing (FTP) and transfer rates

The treasury buys the loans from the liability side, and it is connected to the outside world via the money and capital market. It finances the asset side with credit, where the different transfers of capital among profit centers have certain rates called transfer rates. Once transfer rates are determined, these rates should be used to split income; however they cannot impact, add or deduct, the total income.

A simple example, illustrated in Figure 12.7, shows how such transfer rates are set. Let's say at time t0 the liability profit center borrows for one year a deposit at a rate of 1.5% whereas the asset profit center is lending a five-year loan at a rate of 5.8%.

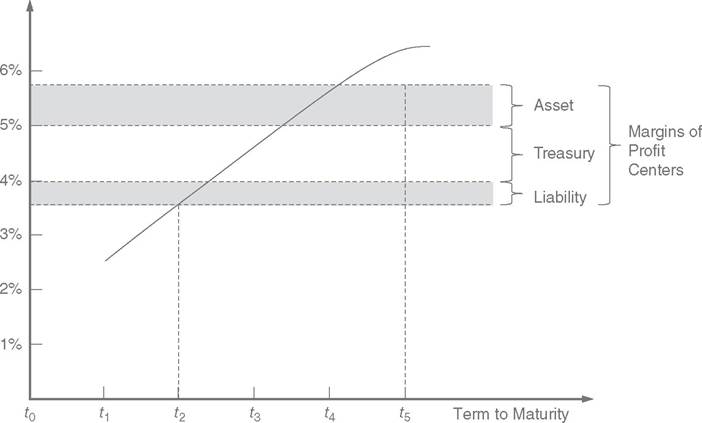

The treasury plays the role of the intermediator between the two profit centers: it buys the one-year liability with the risk-free rate of 2.2% and then finances the five-year loan for the current risk-free fixed market rate of 5%. In this example, the one year deposit bought by the treasury pays a margin of 2.2% - 1.5% = 0.7% to the liability profit center. At the same time, the asset profit center for the five-year loan makes from the treasury a margin of 5% - 5.8% = 0.8%. The treasury receives a net margin of 2.2% - 5.0% = 2.8%.You may wonder why the treasury should play such a role and receive this margin in the first place. In our example, for the next five years (i.e., from t0 to t5) the asset profit center receives from the loan the agreed rate of 5.8% whilst still passing 5% to the treasury, and thus is keeping the margin constant at 0.8% regardless of any possible changes in the market conditions. After one year however, at t1 the deposit with rate of 1.5% matured. Assume now a situation where at t2 the market is under stress and the new yield curve shifts to higher rates as illustrated in Figure 12.8. This means that the liability profit center will have to pay a higher rate of 3.6% to borrow the new loan deposits. Consequently, the treasury must also adapt to new market conditions by buying the new liability with the higher risk-free rate of 4%. Both liability and treasury margins will be adjusted accordingly resulting in lower margins of 0.4% and 1% respectively. Note that from the new yield curve it is expected that the rates increase dramatically in years three and four which implies that the treasury profit will become

negligible or even negative, which indicates losses. The problem becomes even worse where the asset profit center is lending at t2 a five-year loan at a rate of let's say 5%. This implies that the treasury will have to finance this loan with fixed market rate lower degree and thus shrink out the final margin.

Another question is: what if, due to stress market conditions, accessing capital from the liability side has become difficult and thus the bank cannot provide liquidity to the asset side? Or what if there is an excess of cash from profit centers that the bank cannot lend to the market? In both cases, the treasury will buy or sell the missing capital required or excess liquidity by using its link to money and capital markets. Moreover, the treasury may trade liquid assets to access liquidity. In a nutshell, we can say that the treasury acts as a buffer between the asset and the liability profit centers of a bank, ensuring its profit margins stay intact.

Banks transfer their financial risks to the treasury. Therefore, beyond the role of splitting the profits, the treasury is responsible for managing liquidity, value, income and associated risk as well as absorbing, by hedging or mitigating the risks, any associated losses.15 Therefore, on top of the transfer rate discussed above, transfer rates should include different types of margins:

■ Credit margin which is considering the counterparty risk of the loan credit exposure.

■ Liquidity margin used for the liquidity16 that should beheld against short-term liabilities.

■ Treasury margin for the bank’s treasury profit.17

■ Institution-specific margin which refers to the institution’s own credit rating that impacts the cost of funding.

■ Add-on margins that may include additional profit margins, operational risks and cost, behavior risks, and cost referring to new strategies.18

Banks apply financial analysis to manage risk and optimize profitability. These margins balance asset and liabilities, which both incur risk.

12.4.2 Treasury in P2P finance

After all, financial institutions, with a support of treasury, try to ensure that the lender has positive interest income for the duration of the loan and the borrower enjoys fair market and spread rates.

This happens by considering the evolution of future performance of risk factors as well as by considering and influencing the strategies applied in both asset and liability sides.Does a marketplace lending platform also need a treasury? With the current business model, most likely not. Since they connect lenders and borrowers directly, marketplace lenders have no need to raise funds in the money market. Because the loans they originate never enter their balance sheet, all credit and market risks lie with the lender, so there is no financial risk to offload. The unique selling proposition (USP) of marketplace lending platforms lies in their streamlined operations that reduce operating costs, new rating algorithms to score borrowers and their performance, and in the ability to connect counterparties directly without using their own balance sheet. In this sense, they have a limited need for a specialist who can access credit markets rapidly to generate liquidity. However, what they do need is a way to assess the financial health of the system of which they are after all a part. If there were a financial crisis that led to defaults en masse on a particular marketplace lending platform, this could be catastrophic for the entire sector. The health of the capital markets will inevitably influence the performance of their loan book. Of course, lending platforms do monitor financial markets and certainly have a good overview of the macroeconomics going on around them and of the performance of their current loans. But how the actions that take place on their platforms and the loans that they originate influence the economy beyond the platform will be more complex to assess. Without models of the expected performance of their loans that assess marketplace loans in similar ways to the rest of the formal financial sector, including expected profit and loss for platforms, banks, and individual counterparties, platforms will only have half the picture. Even though their liquidity arises on the spot when a lender and a borrower connect, transparent and consistent analysis will give them a clearer picture of the risk of loans and of the expected market liquidity that borrowers and lenders cumulatively shape.

Platforms need to operate with awareness of their impact on the markets so they can secure robust revenue streams for their lenders. This is where treasury services can fill in the information gap—namely between individual platforms and their impact on the financial sector on the margin.12.5 Concludingremarks

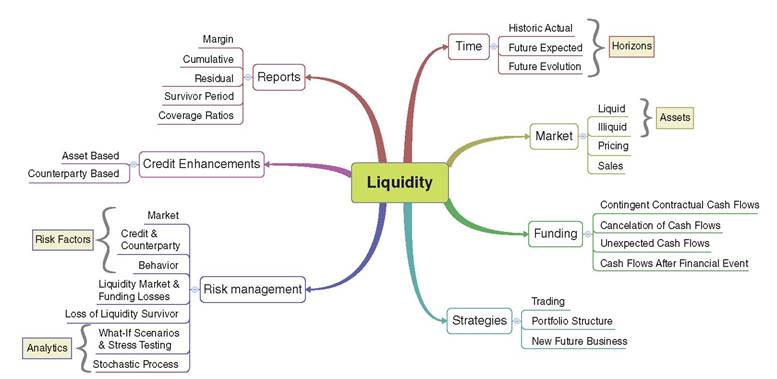

The source of liquidity risk is, in most cases, a combination of all financial risk factors and thus the risk management of liquidity demands integrated risk analysis. The evolution of cash in and out flows is monitored and estimated from past to future times respectively. Market liquidity analysis answers the question as to how liquid a financial instrument is; thus, it is very much linked to its pricing characteristics and trading activities. Funding liquidity refers to contingent contractual cash flows; for instance any risk event (e.g., default) will cancel the expected cash flows, and may initiate the ones from credit enhancements and recoveries. Liquidity managers must consider both types of liquidity analysis, assessing and driving the strategies for rolling over and/or defining the future businesses accordingly. The combination of funding and market liquidity is the basis of applying risk management based on real-world probabilities. Liquidity risk is a result of market, counterparty and behavior risk factors and thus, institutions acting as investors should apply the different types of risk analytics discussed in the previous chapters. Therefore, liquidity risk is measured based on deterministic or stochastic scenarios. Moreover, institutions also assess their strength against contingent liquidity events. Liquidity and its risks are viewed mainly by using ratios and gap reports of historical to future cash flows. Investors must pay great attention to identifying and managing both market and funding liquidity ensuring liquidity survivor under any stress conditions. They apply strategies to manage liquidity and to keep the business and credit enhancements always liquid. Figure 12.9 illustrates in detail the main elements considered in liquidity risk analysis.

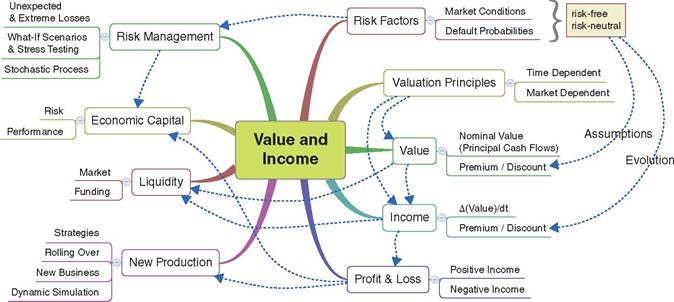

In value and income analysis, the main parameters are the nominal value and the delta of values over time, whereas premium and discount are employed to adjust them. Moreover, valuation principles play a critical role in estimating values. Of course, all financial risk factors based on risk free assumptions affect value and expected income. Stressing deterministically and/or stochastically these factors, by employing risk management, will result in changes in value and corresponding possible negative income, i.e., losses. Income and losses reflect the profits and losses which, together with risk measurement, give an estimation of the economic capital. Based on dynamic simulation, income drives the profit and loss together with strategies for the evolution of new production. Finally, as mentioned, value plays a key role in managing both market and funding liquidity. The correct estimation of the value of an asset indicates the degree of the cash results from the liquidation process. Moreover, both value and income will indicate the expected contractual cash flows over time, which may be used in funding liquidity management. Figure 12.10 illustrates in detail the elements and their relations used in value and income analysis.

FIGURE 12.9 Main elements of market and funding liquidity and their risk management

As businesses evolve there should be a new production of credit portfolios. In such cases, institutions are simulating the dynamics in market and credit risk factors evolution. This means at future time intervals reevaluating both market conditions and credit quality of the existing as well as new counterparties; in addition considering their future behavior under normal and stress market conditions. The above means simulating the evolution of value and income as well as the possible losses. Based on these dynamics as well as the idiosyncratic characteristics of the investors they are defining the strategies for rolling down or rolling over under stress or going concern scenarios. The aim is maximizing profitability and minimizing losses whilst ensuring enough liquidity even under stress conditions. Such targets can be reached by investing, re-investing and allocating on the same or different types of financial instruments within a certain time horizon. In fact the characteristics of the new contract and counterparty must be defined and analyzed using their outcomes under assumed and uncertain conditions.

FIGURE 12.10 Main elements of value and income analysis

Because banks need access to capital markets, they need an experienced specialized center, i.e., treasury, to access these markets. On the other hand, the treasury can support and influence the management of assets and liabilities that would otherwise weigh down the balance sheet of the bank. The advantages of working with a treasury department are clear-cut for banks: they can increase their spread and increase returns for investors; the treasury identifies exposure to financial risks and manages these risks by absorbing or mitigating possible losses; the separation of risk and front-end operations can increase the stability and robustness of a bank. The treasury itself fulfils these functions by pragmatically applying analytics on liquidity, value, income, and risk measurements. It also measures and balances profit and risks for exposures to borrowing and lending.

Individual marketplace lenders will hardly need a treasury department, but several platforms together—or the entire sector, for that matter—could benefit from a centralized entity that would provide treasury-like services for all of them in an aggregated manner. The benefits of such a system are to ensure positive interest income for the lenders on one hand and fair market and spread rates for the borrowers on the other—under both canonical (expected), and stress (unexpected) market, liquidity and behavior risk conditions.

The aim of applying risk management is to increase profitability, ensuring at the same time robustness of the financial system against unexpected conditions. The applied methods should have a sufficient degree of complexity, whereas the risk scenarios should have effectiveness sensitive to risk factors. All models and approaches must have a high degree of transparency, available to the market. This will ensure consistency in the disclosure reports. Overall, counterparties involved in the financial deal should make decisions by having a good view and understanding of the existing status as well as any assumptions made for the future. The efficiency of such decisions is a result of an optimal combination of analytics and intuitiveness.

NOTES

1. Typical credit risk contracts are financial collaterals and guaranties.

2. Before the credit crunch in the financial crisis of 2007/8, financial securitization products were considered highly liquid due to their high quality of senior and mezzanine tranches; ironically, many of them became highly illiquid due to stress market and credit conditions.

3. See also the approaches on Funding and Liquidity Valuation Adjustment denoted as FVA and LVA.

4. Use other source of liquidity, typically for financial institutions via additional facilities or bailout from central banks.

5. Under market liquidity stress, the institutions may be forced to carry out trading activities (mainly sales) of their liquid assets with additional discounts; they may also request to access funding facilities and deposits with probably high cost.

6. See also BIS paper bcbs238 on Basel III: The Liquidity Coverage Ratio and liquidity risk monitoring tools.

7. Defined as high quality with certain degrees of liquidity.

8. Based on the regulation from the Bank of International Settlements (BIS), the total net cash outflows considered in the estimation of the Liquidity Coverage Ratio are the ones occurring over the next 30 calendar days.

9. Income analysis is also called income simulation.

10. Unified Financial Analysis, The missing links of finance, by Willi Brammertz, Ioannis Akkizidis, Wolfgang Breymann, Rami Entin, Marco Rustmann (Wiley 2009).

11. Sensitivity analysis can also be a cause for measuring the impact of risk factors' fluctuation to value; however, in this book we will be focusing on real-world probabilities based on stress testing and stochastic process analysis.

12. The size of the portfolio is not important for the VaR method; it can consist of only one contract or of all the contracts in the entire organization.

13. Commonly used ROC models are Risk-Adjusted Return on Capital (RAROC), Return on Risk- Adjusted Capital (RORAC); moreover, there are well known ROA models which are Return on Risk- Adjusted Assets (RORAA), Risk-Adjusted Return on Assets (RAROA).

14. The minority is received by the stake holders which defines the equity.

15. Of course, if the market had moved in the opposite direction the profit of the treasury would have increased.

16. Usually as cash or highly liquid assets.

17. Deal-making profit center.

18. New markets and contracts.