New production

Businesses are going concerns, and investors need to plan the future of their new portfolios. New production is a forward looking process where time evolution is the underlying factor.

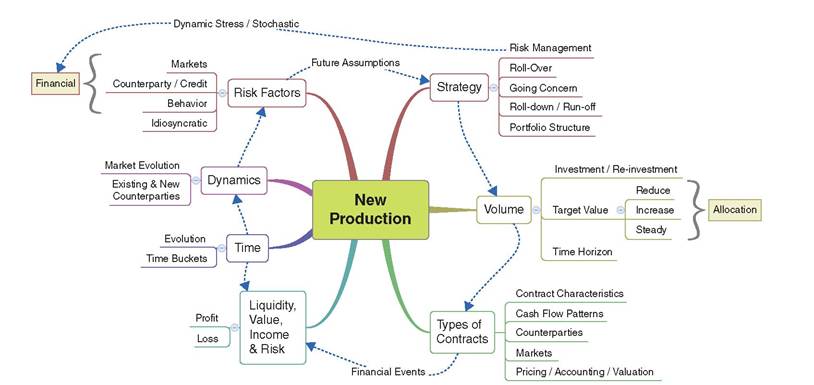

Time drives the dynamics of market evolution, credit status of both existing and new counterparties. Thus, these dynamics are considered in estimating the future performances of financial risk factors (i.e., market, counterparty and behavior), and also the idiosyncratic characteristics of the investors. All future assumptions of the financial risk factors are considered in the strategic decisions on whether the performance of the portfolio structure will be based on run-off or rollover and going concern processes. Moreover, how the risk management will be applied is also taken into consideration. Based on the investors’ strategies the following decisions have to be made:a. The target volume/size of the investment performance with a certain time horizon

b. The type of business in regards to contract terms and conditions made among the counterparties, i.e., lender and borrower

c. The investment and re-investment process for structuring or restructuring the portfolios respectively based on the new business types and/or the targeted volume.

After all, at future times, the expected value, income and their risk measurements will result in the corresponding evolution of profit and losses to evaluate the worthiness of the new production.

We would like to list all the above elements that should be considered during the new production process:

■ Time. The future time is set in regard to the horizon and time buckets/intervals where the evolution of financial risk factors, patterns of the financial contracts and financial events will be aligned.

■ Dynamics. The expected evolution of market conditions and future credit status of the counterparties are the dynamics considered in planning the production of the future businesses.

For instance, yield curves, prices, credit spreads, etc., to be started at future points in time should be defined. Furthermore, such evolution is expected to impact, directly or indirectly, both market and counterparty behaviors.■ Risk Factors. The risk of the above dynamics to move away from the initial expectations is part of the constant changes in financial risk factors. Moreover, some idiosyncratic characteristics, of the investor, may change through time.

■ Strategy. The investor must decide whether only the existing contracts in the current portfolios will be considered at roll-down/run-off liquidation process or a roll-over process will be applied. Moreover, new contracts may enhance the future investments at goingconcern view. As such, where a process is applied at portfolio (or account) level its structure must be also defined. Finally, the management of financial risks should consider the future evolution of risk factors, i.e., dynamic stochastic or deterministic.

■ Volume. The target degree in the volume of the future business, for a certain time horizon, must be defined by the investors. Thus, based on their strategies three different options may be considered:

■ Reducing the volume by rolling-down/run-off of the existing business without reinvesting in the same or different types of business, i.e., financial contracts/portfolios. This may happen when investors would like to sunset the existing portfolios following the maturity steps, at future times, of the financial contracts.

■ Keeping the volume steady by rolling-over the existing (old) type of business after they mature, i.e., re-investing in the same types of financial contracts/portfolios. In this case, the investor is most probably happy with the returns and thus enhances the portfolio with

FIGURE 12.5 The elements and processes of a new production

the same types of financial contracts—assuming, however, that the market conditions and counterparties’ credit status stay steady and/or the current portfolio has a favorable degree of robustness against risks.

■ Increasing the volume by adding new contracts, discussed in the next point referring to types of contracts.

A combination of the above investments and re-investments defines the business allocation and portfolio structure of the new production.

■ Types of contracts. Adding new contracts (type of business), investors must decide and define their characteristics, i.e., the terms and conditions that will define the pattern of cash-flow exchange, types of counterparties and possible options that could be exercised. Moreover, the markets linked to these contracts, pricing assumptions and the applied accounting/valuation rules.

■ Liquidity, value, income and risk. Both current and existing financial contracts will result in liquidity, value, income and corresponding risk measurements leading to profit and loss analysis.

Figure 12.5 illustrates the above elements and process considered in a new production.

In marketplace lending the investment on a single capital, provided by the lender, is in fact sliced to a number of loans, constructing therefore a portfolio of loans linked to several borrowers. Having said that we can argue that the risk and portfolio management discussed in the above paragraphs can be naturally applied following the same guidelines.

12.4