Argentina

A leap into the unknown

| GDP | USD632.8bn (World ranking 22) |

| Population | 46.2mn (World ranking 33) |

| Form of state | Presidential republic |

| Head of government | Javier Milei (President) |

| Next elections | 2025, Legislative |

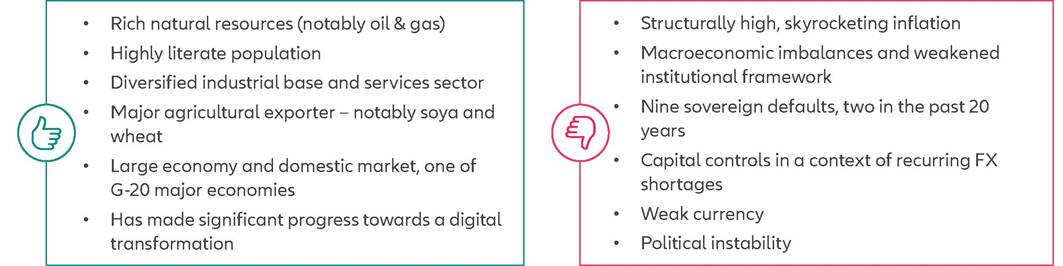

Strengths & weaknesses

Economic overview

A painful short term

Argentina has a long history of political and economic instability.

In recent years, the country has experienced major policy shifts with significant macroeconomic stability implications, characterized by high economic and currency volatility, structurally high inflation, recurrent debt default crises and social tensions. After a deep recession during the pandemic, including a debt default, Argentina experienced strong base effects and a recovery in agricultural exports, coupled with the gradual reopening of the economy, leading to a strong rebound in 2021 (+10.3%). In 2022, growth reached 5.0%, driven by a strong performance in services. In particular, the tourism and transport sectors were strongly supported by the stimulus measures introduced after the pandemic. In 2023, however, an unprecedented drought, in addition to macroeconomic imbalances, will pushed the country into recession since 2023 is over. In 2024, Argentina is also likely to be in recession (we estimate a -2% contraction), due to the measures announced by the government to rebalance the macroeconomic picture, which includes fiscal cuts on top of galloping inflation, triggered in the short term by a major currency devaluation. In the longer term, growth could accelerate on the back of a more competitive business environment and sustained investment encouraged by the fiscal consolidation wall. We expect economic growth to average +2.5% in 2025, but uncertainties high.Argentina also struggles with rising and widespread inflation since mid-2022, surging from 48.1% yoy on average in 2021 to 211% yoy in 2023; extremely low international reserves; continued financing of public debt by the Banco Central de Republica Argentina (BCRA) and a high spread between the official and parallel exchange rates (e.g., the Blue Rate). The official USD:ARS exchange rate has doubled since the beginning of 2023 and has been pegged at AR350 per USD since mid-August 2023 - before being devalued by the new administration to ARS800 per USD - leading to an increase in currency competitiveness as currency depreciation outpaced inflation. Javier Milei is likely to favor keeping the peso weak as part of his idea to improve competitiveness. The inflation situation remains uncertain, but we expect it to get worse before it gets better. We expect inflation to exceed 250% in H124. Further depreciation of the peso, as well as government disengagement - especially subsidy cuts - are likely to add to inflationary pressures before orthodox economic policies start to weigh on inflation. It will take several years for inflation to stabilize at lower levels: 70.0% yoy by end-2025 and 40.0% yoy by end-2026.

Finally tackling fiscal imbalances?

Javier Milei's administration is trying to address the chronic fiscal imbalances Argentina faces by introducing fiscal austerity measures and by trying to improve the external position of the country. In accordance with Mr Milei's libertarianism, subsidies to the public sector, public employment and public investment should be reduced, as well as tax revenue (reduction of income tax and VAT). Fiscal consolidation should be well seen by the IMF, which struck a deal with Argentina in 2020.

After the first announcements of the Milei administration, the IMF welcomed “bold initial actions” and said “the new package provides a good foundation for further discussions to bring the existing (...) program back on track”.Debt levels remain high despite the restructuring of market debt in 2020. They especially grew in the last two years, from 80.8% of GDP in 2021 to 89.5% of GDP in 2023. Sovereign debt remains highly exposed to FX, given the large share of debt denominated in foreign currency. Debt repayment will remain a challenge over the medium-term as Argentina's access to capital markets remains constrained by high yields and the country's relationship with official creditors is uncertain.

Political uncertainty remains high while the business environment is poor

The business environment in Argentina is quite poor. Capital controls are quite stringent and extremely sensitive to the country's external position and the track-record of expropriation, although current risks are lower. Argentina ranks 144 out of 177 worldwide in the 2022 Heritage Foundation Index of Economic Freedom's survey and 27 regionally. The country has low rankings in terms of property rights and monetary freedom and even ranks comparatively poorly regarding its strengths. The Worldwide Governance Indicators survey of 2022 points out a degradation of the country's position, especially in control of corruption and regulatory quality. The accession to power of Javier Milei could turn the tables, because his ultraliberal stance, will for fiscal consolidation and privatizations could attract investors. But on another front, weaknesses also appear, as shown by our proprietary Environmental Sustainability Indicators of 2023: Argentina has a very poor recycling rate, as well as a renewable electricity output. It is not really vulnerable to climate change, but is poorly placed in the race for the green transition. It is overall ranked 105 out 202 for sustainability, upheld by its low water stress levels.

Political tensions peaked as the economic situation became dire in 2023 saw Milei come to power on 10 December. Milei advocates for a drastic reduction of expenses (-15% of GDP), large privatizations of the health and education systems, redesign of more than half the ministries, gradual dollarization of the economy and suppression of the BCRA. Whether Milei will implement his “shock therapy” as strictly is still to be determined, because he enjoys relatively low support in the lower house of Argentina (38/257 seats) and in the upper house (7/72 seats) and because popular opposition to his anti-social reforms is likely to be elevated. Risks to governability of the country are therefore likely to arise as time passes and as Milei's political capital fades. Having stood out as anti-system during the campaign, Milei now has to prove himself if he wants to consolidate his position in the 2025 mid-term legislative elections.

Overall, recent data show that the trade balance is deteriorating: a deficit was recorded in Q1 2023, at -0.59% of GDP, but also in Q2 2023, at -3.27%, in seasonally adjusted terms. Weather phenomenon El Nino had a harsh impact on Argentinian production of agricultural products. We still expect the current account to register a surplus in 2024 (1.2% of GDP) following a -0.6% deficit in 2023. The “fiscal shock” Milei wants to implement should indeed allow for internal macroeconomic indicators to get back on track and the rebound in agricultural exports due to the - speculated - end of El Nino phenomenon should support the country's current account. Note that Argentina's current and capital accounts are highly distorted by widespread trade, financial, capital, price and FX controls. Hence, the stability of the Balance of Payments is to a large extent relative, given binding controls and extensive financial repression.