Australia

Heading for a soft landing

| GDP | USD1675.4bn (World ranking 12) |

| Population | 26.0mn (World ranking 56) |

| Form of state | Constitutional parliamentary monarchy |

| Head of government | Anthony Albanese (PM) |

Next elections 2024, Legislative

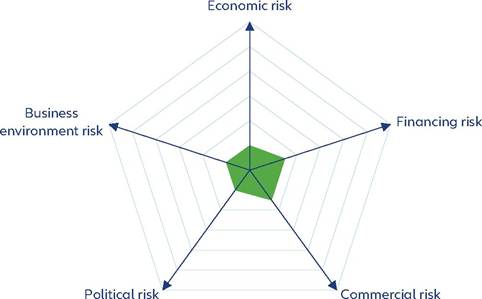

Strengths & weaknesses

Economic overview

Modest growth and elevated inflation in 2024

Australia has been a strong growth performer in the past decades, with its GDP expanding on average by +2.9% in the 2000s and +2.6% in the 2010s.

The economy contracted by -1.8% in 2020 but rebounded strongly by +5.2% in 2021, followed by +3.7% in 2022. A robust post-pandemic recovery and favorable terms of trade have positioned Australia more favorably in the cyclical aspect compared to most other advanced economies. However, headwinds have arisen from higher inflation and interest rates and the ongoing cost-of- living pressures continue to impact demand. Additionally, a sharp slowdown in export growth indicates that the external sector will likely contribute neutrally to growth in 2024. Overall, we expect annual GDP growth to slow down from around +2% in 2023 to +1.5% in 2024-2025. Australia is on a narrow path to a soft landing. Over the coming years, a more sustainable balance between supply and demand across the economy, including in labor and product markets, is expected to support the return to low and stable inflation while growth in domestic activity should return to trend.In response to the Covid-19 pandemic, the Australian government put in place a comprehensive set of fiscal policy measures, including significant stimulus payments to households and businesses. As a result, Australia's fiscal balance registered a deficit of -8.7% of GDP in 2020 and -6.5% in 2021. As tax revenues exceeded prepandemic levels and expenditure contracted significantly with the expiry of Covid-19 support programs, a rapid fiscal consolidation took place, bringing the fiscal shortfall to -2.3% of GDP in 2022. A period of high commodity prices is estimated to have allowed the government to register an even narrower deficit in 2023. Going forward, increased pressure on expenditures is expected due to higher defense spending as well as rising healthcare and welfare expenses. Therefore, we expect the fiscal deficit to widen somewhat to just over -2% of GDP in 2024-2025.

In terms of monetary policy, following a late start, the Reserve Bank of Australia (RBA) has tightened monetary policy rapidly. In response to rising inflation, the RBA hiked the policy rate by a cumulative 425bps from May 2022 to November 2023. Given a positive output gap, a tight labor market and continued inflationary pressure in the housing and energy sectors, we expect headline inflation to remain above 3% throughout 2024. As a result, the RBA will not pivot before the second half of the year and perhaps even only in 2025.

Structural vulnerabilities: domestic debt, external debt

Australia's short-term financing risk is low. The indicators that need monitoring in the short run are mostly related to household debt and external debt. Australia's household debt continues to be among the highest in OECD countries, which means that currently higher interest rates may cause some debt-servicing strains, though effective oversight should keep the risk of banking system instability low. At around 100% of GDP in 2021 and 87% of GDP in 2022, external debt remains another source of vulnerability.

However, buffers such as favorable investor confidence, a relatively positive economic outlook (compared to other advanced economies) and positive current account balances should provide some cushioning.While Australia had been exhibiting chronic current account deficits in the past, the balance turned to a small surplus in 2019, which then expanded until 2021, driven by high prices for Australian commodity exports, most notably thermal coal and LNG. After peaking at +3% of GDP in 2021, the external surplus narrowed gradually in 2022-2023 and the current account is forecast to come in near balanced in 2024-2025. Amongst others, policies that stimulate investment and higher outward dividend payments by mining companies will contribute to reducing the current account surplus. A risk in the medium term is Australian exports' reliance on Chinese demand in a potentially deteriorating geopolitical context.

Business environment and political developments

Australia's business environment is well-positioned in our assessment of 185 economies. The World Bank's annual Worldwide Governance Indicators surveys suggest that the regulatory and legal frameworks are business-friendly and the level of corruption is low. Likewise, the Heritage Foundation's 2023 Index of Economic Freedom survey has put Australia at rank 12 out of around 180 economies and rank four in the Asia-Pacific region, reflecting very strong scores with regard to property rights, judicial effectiveness, government integrity, business freedom, trade freedom, investment freedom and financial freedom. However, Australia scores less favorably with regard to the tax burden, attributed to a marginal income tax rate of 45% and a 28.7% tax burden in relation to GDP. In terms of our proprietary Environmental Sustainability Index 2023, Australia is ranked 54 out of 210 economies, reflecting strengths regarding water stress and climate change vulnerability, but weaknesses in terms of renewable electricity output and recycling rate.

After the general election in May 2022, the Labor party, led by prime minister Anthony Albanese, is likely to remain in power until the end of its term in 2025. Both the previous Liberal-National coalition government and Labor actually saw voting shares decline compared to the 2019 election, beneficiating the Greens and the independents and reflecting the electorate's concern with climate change and corruption. Labor and the Greens (along with some groups of independents) support more actions in these areas.