China

Growth headwinds and complex geopolitics

| GDP | USD17963.2bn (World ranking 2) |

| Population | 1 412mn (World ranking 2) |

| Form of state | Communist party-led state |

| Head of government | Xi Jinping (General Secretary of the Communist Party) |

| Next elections | 2027, Legislative |

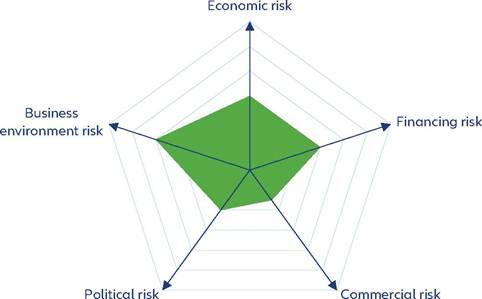

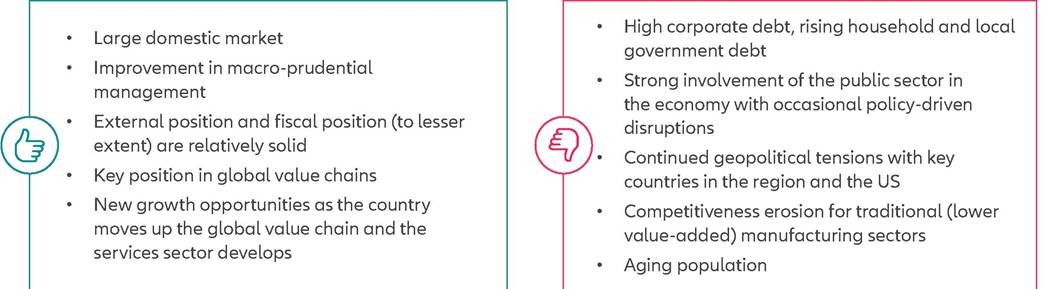

Strengths & weaknesses

Economic overview

All eyes are on policy

China has been a regular global outperformer, with real GDP growth averaging +7.7% during the period 2010-2019.

It was one of very few economies that was spared by a recession at the height of the global pandemic in 2020 (growing by +2.2%), followed by a massive rebound in 2021 (growing by +8.5%) while a significant slowdown was registered in 2022 (growth at +3.0%). In 2023, the economic rebound disappointed, primarily due to low consumer confidence, a property sector downturn and limited fiscal and monetary policy support. We expect China to grow by +5.2% in 2023, followed by +4.6% in 2024 and +4.2% in 2025 - thereby converging to a path of lower trend growth compared to the recent past, notably as growth headwinds both domestic and external are likely to persist. This is slightly above growth in the broader Asia- Pacific region, expected at +4.0% in 2024 and +3.9% in 2025. In terms of prices, as a result of industrial overcapacity and weak demand, consumer and producer prices have been on a disinflationary trend since the beginning of 2023 and we expect inflation to remain muted through 2024 and 2025 at 1.6% and 1.7% respectively. We forecast insolvencies in the Asia-Pacific region to rise by +5% in 2024 and +3% in 2025, although they are expected to remain below their prepandemic levels. China accounts for 57% in our regional index and the economy has recently proved to be successful in maintaining a low number of insolvencies, with around 6 500 cases expected for 2023 (45% below 2019 levels but close to 2017 levels).Policy support has been limited in 2023. However, going forward, we expect fiscal easing to shoulder the task of boosting broad based economic growth while monetary easing will play a facilitative role. Measures implemented so far have aimed to support real estate demand as well as fiscal support for urban village renovation and public housing construction. Another major focus will be to bring relief to local government debt stress through optimization and restructuring. Consequently, we expect the overall public- debt-to-GDP ratio to pick up from 83% in 2023 to 92% in 2025. In terms of external balances, we expect the current account surplus to decrease from 1.5% of GDP in 2023 to 1.1% of GDP by 2025, broadly driven by higher imports of services.

The challenge of continuing to grow in the long run

Overall, indicators show that the short-term financing risk is medium. The indicators that need monitoring in the short run are in particular the overall fiscal deficit and domestic credit growth, especially in the context of challenging local government finances and the property sector downturn. Domestic credit to the private sector relative to GDP, remains elevated compared to emerging peers (185% in 2022). However, we believe for now that authorities have the necessary tools to manage and keep risks under control.

Looking at external account balances, 2023 has been a challenging year for China. External pressures from the West are adding to domestic woes. The resilience of exports in late-2023 is unlikely to last as it is partly due to exporters decreasing prices to gain market share, which is not sustainable in the medium-term.

Going forward, we expect the current account surplus to decrease to 1.4% of GDP in 2024 and 1.1% of GDP in 2025. In terms of the capital and financial account balance, net outflows of direct and portfolio investment seem to be widening the deficit, primarily due to two factors. First, foreign investors are increasingly concerned about China's challenges in the housing market, low consumer confidence and high local government debt (FDI inflows into China turned negative for the first time on record in Q3 2023) and second, outbound flows from China have increased, notably towards ASEAN and Latin American economies.Lastly, while rising geopolitical tensions are likely to reshuffle trade and investment patterns, China will not lose its position as an end-supplier due to complex inter-linkages in the global supply chain. In the medium run, China's main challenge is managing the transition to a lower pace of potential growth as the economy matures and relies less on the real estate sector. What's at stake is to find new growth drivers (innovation, private consumption, services etc.) while navigating vulnerabilities (debt burden, geopolitical tensions, aging population etc.)

Business environment: Recent signs of deterioration

Our proprietary model that tracks the structural business environment across 184 countries suggests that the business environment in China has deteriorated over the last two years amid the broad-based economic turmoil, weaker business sentiment and rising geopolitical tensions. The World Bank Institute's annual Worldwide Governance Indicators' suggest that there has been a decline in regulatory quality in 2022 relative to 2021, although there have been slight improvements in the rule of law and control of corruption. In addition, the Index of Economic Freedom from the Heritage Foundation assigns a rank of 158 out of 184 countries in 2022, down from 107 in 2021, reflecting a deterioration in scores that reflect freedom in terms of trade, business, investment and property rights. Lastly, China ranks low based on our proprietary “Environmental Sustainability Index” at 178 out of 210 economies, suggesting that while China exhibits strengths in water stress and energy use per GDP, there is potential for improvement in terms of the recycling rate, climate change vulnerability and renewable electricity output.