Costa Rica

Slowing economic growth, rising macroeconomic policy risks

| GDP | USD68.4bn (World ranking 83) |

| Population | 5.2mn (World ranking 121) |

| Form of state | Presidential republic |

| Head of government | Rodrigo Chaves Robles (President) |

| Next elections | 2026, Presidential and legislative |

Strengths & weaknesses

Economic overview

A fragile economic recovery

Costa Rica's macroeconomic outlook was already fragile prior to the pandemic despite structural reforms.

As part of its accession to the OECD, Costa Rica implemented key fiscal and structural reforms aiming at containing the high fiscal deficit, boosting medium-term growth prospects and lowering the high levels of unemployment. However, the growth outlook remained fragile, with real GDP growth averaging +1.5% over 2017-2019 amid a challenging external environment, natural disaster shocks and deteriorating investor sentiment, given the widening fiscal deficits.Despite weakening domestic demand in the context of high inflation and rising interest rates, economic activity was supported by robust external demand, as the free trade zones continue to showcase double digit growth. As a result, a strong export performance and recovered tourism sector fueled the economy growing by +7.8% in 2021 and +4.3% in 2022. We expect that GDP growth will continue at +4.4% in 2023 and forecast that it will cool to +3.2% in 2024.

We expect inflation to fall to +2.8% in 2023, after it accelerated rapidly through 2022, peaking at +12%.

The Banco Central de Costa Rica (BCCR, the central bank) is in the process of bringing down interest rates, having raised them to combat surging consumer price inflation in 2021-22. Its most recent statement indicated that it remained concerned about the risk of global oil prices delivering another supply shock and it will therefore take its time over monetary easing, even though consumer prices are firmly in deflationary territory. We expect the BCCR to keep its easing policy stance in 2024 and 2025 and returning the rate to a broadly neutral level, which we estimate at 3.25% by the end of 2025. We expect a restrictive monetary policy stance coupled with the easing of global commodity prices will result in a gradual convergence to the central bank's inflation target of 3% by 2024. The main risk to our monetary policy forecast is an unexpected spike in global food or fuel prices, triggered by geopolitical conflict or by adverse weather conditions caused by El Nino, which would push up local inflation. This would force the BCCR to pause its easing cycle and could even prompt it to raise rates again as a last resort.Weak public finances will remain a key risk

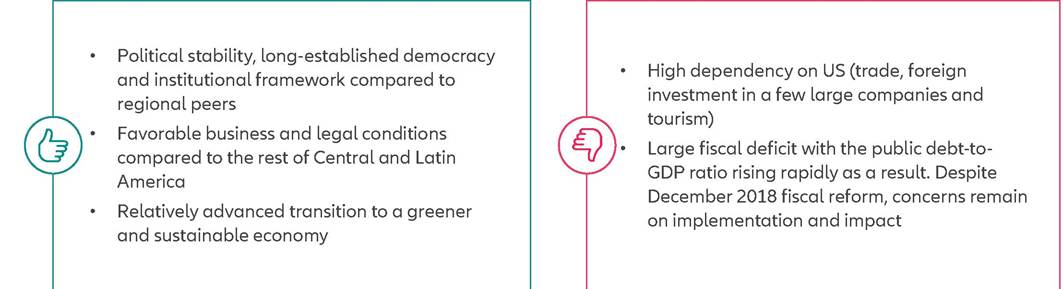

Costa Rica's fiscal outlook mediated from the strike of pandemic. Costa Rica's Extended Fund Facility will continue to support the government's efforts to reduce the non- financial public-sector deficit, which narrowed from a pre-pandemic average of 5.7% of GDP in 2016-19 to 2.5% of GDP in 2022. However, modest economic growth will keep government revenue low, meaning that fiscal consolidation will need to be achieved through reforms to state spending, revenue-raising tax reforms and a greater focus on current and historical tax evasion.

The fiscal adjustment required by the IMF program approved in early 2021 could be a challenge, given Costa Rica's history of political impasses in the process of approving reforms or external financing. Thus, fiscal consolidation will have to be achieved through reforms in state spending and fiscal reforms for collection, but the lack of a parliamentary majority poses risks.

That said, approval of the IMF program should help to catalyze additional official support from creditors for the 2023-27 period, easing sovereign financing conditions.Fiscal overperformance, a stronger exchange rate and inflation lowered debt/GDP to 63.8% at the end of 2022 and we expect it will continue as 63% in 2023. The legislature has approved the issuance of up to USD5bn in Eurobonds and legislation is being drafted to give the executive more discretion over external borrowing. A primary dealer pilot program is underway and a new law has been passed to reduce the obstacles for foreign investors to participate in domestic debt markets, which should help develop the local market. Finally, legislation was submitted to centralize debt- related functions into a debt management office and the government is developing a strategic framework to govern its management of sovereign assets and liabilities.

The 2022 primary balance was 1.4% of GDP above the target. Tax revenues rose by 0.4% of GDP between 2021 and 2022, mostly due to stronger activity and the price effect (including strong increases in the price of imported goods). Costa Rica's balance of payment position will be supported by higher inflows of FDI. The current account deficit is expected to decline from 4.3% of GDP in 2022 and to around 3% of GDP over the medium term as external demand, including tourism, continues to recover. Additionally, the IMF program and lower import demand, alongside slower economic growth, should limit balance of payment pressures.

Business environment and political developments

According to the 2022 Heritage Foundation's annual Index of Economic Freedom survey, Costa Rica ranked 10th in Latin America, reflecting very strong scores with regard to government spending and monetary freedom while shortcomings in fiscal health, labor freedom and financial freedom.

Costa Rica's strong political institutions, long democratic tradition and relative social stability support political stability. Fiscal reforms and external financing require Congress approval and Costa Rica has a track record of political gridlocks, which could hamper policymaking in the medium-term, especially as the proposed adjustment includes several contentious reforms. In early 2023, President Chaves secured parliamentary approval for the issuance of USD5bn in Eurobonds over the next three years, in exchange for relatively minor concessions. Efforts to improve the fiscal position will be the main source of political contention.