Examining the effect of compensation motivation and work period on employee performance

N. Nawiyah, T. Endrawati, M.R. Cili, R.T.H. Parnanto & A. Wahyudin

Polytechnic APP Jakarta, Ministry of Industry, Indonesia

ABSTRACT: The research was aimed to determine the effect of compensation, motivation, and work period on employee performance before and after the performance allowances at the Academy of Corporate Leadership Jakarta.

The analysis was based on managerial implications. The research used quantitative with multiple linear regression analysis technique to determine the effect of compensation variable (X1), motivation variable (X2), and work period variable (X3) on employee performance (Y). The population of this research was 60 employees of Academy of Corporate Leadership, and census technical sampling method was used. The data were collected through questionnaires distributed to employees of the Academy of Corporate Leadership that consists of two sources of data namely primary data and secondary data. The result of the research showed that before the performance allowances, compensation had positive and significant effect on the employee performance while motivation and work period had no effect on the employee performance. After the performance allowances, compensation and motivation have positive and significant effect on employee performance, while work period has no effect on employee performance. The implication from this research is motivation and compensation can give encouragement to employee more than hard work.1 INTRODUCTION

Human resources in the organization make a contribution to the achievement of organizational goals. Such contribution is usually referred to as work or performance. Each job has a specific job criterion or a working dimension that identifies the most important elements of a job. Organizations need to know the various weaknesses and advantages of employees as a foundation to fix weaknesses and strengthen the advantages.

This is to increase productivity and employee development so that the performance of employees in the organization can be optimized for the achievement of organizational goals.The performance appraisal is in accordance with PP. 10 year 1979 namely DP3 assessment system (List of Job Implementation Assessment). In 2011 was issued Government Regulation no. 46 of 2011 on the assessment of the performance of civil servants who are expected to contribute well in terms of assisting government agencies in measuring employee performance. Furthermore, on November 17th, 2012, Presidential Regulation of the Republic of Indonesia Number 101 of 2012 was published, on employee performance benefits within the Ministry of Industry. This Presidential Regulation is issued as a manifestation of the implementation of Bureaucracy Reform within the Ministry of Industry; the Academy of Corporate Leaders follows the applicable regulations. This Presidential Regulation starts to be implemented and the performance appraisal system is also adjusted to this Presidential Regulation.

Moeheriono (2010) states that the factors affecting employee performance cover expectations regarding rewards, encouragement, ability, needs and nature, perceptions of job, external and internal rewards, perceptions of reward levels, and job satisfaction. Compensation and motivation play an important role in implementing employee performance. In addition, the work period can contribute to the performance of an employee; the longer the employee work, the higher the knowledge of the job.

Based on the background described above, this study was intended to obtain empirical evidence on “whether there is effect of compensation, motivation, and work period on employee performance at the Academy of Corporate Leaders Jakarta before and after the existence of performance allowances”.

Performance, as stated by Mangkunegara (2005), refers to work performance or achievement that is actually achieved by someone in quality and quantity in performing their duties in accordance with the responsibility given to him/her.

The Regulation of the Minister of Industry of the Republic of Indonesia. No. 112/M-IND/PER/12/2012 definition of performance allowances is followed for the allowance given to employees based on discipline and employee performance appraisal. Assessment of the discipline is the assessment of the working hours of Civil Servants stipulated under the regulation.

Compensation is a Human Resource Management (HRM) function that deals with each type of reward an individual receives in return to the performance of the organization’s jobs. Employees exchange their energy to get financial reward and non-financial reward (Kadarisman 2012).

Motivation, on the other hand, is a set of attitudes and values that affect the individual to achieve the specific goal in accordance with the individual goals. Such attitudes and values are an invisible one that provides the power to encourage individuals to achieve their goals (Veitzhal 2004).

Last, the work period is the period of time people have started working until the current working time. The period of work can be interpreted as a long piece of time where a workforce entered into a single area of business until a certain time limit (Suma’mur 2009).

2 METHOD

2.1 Population and sample

The research was conducted at the Academy of Corporate Leadership and it involved 60 lecturers and employees of the Academy of Corporate Leadership. The participants were selected by saturated sampling technique/census where all employees become target of sampling.

2.2 Research variable

Dependent variable in this research is employee performance before and after existence of performance allowance. Employee performance indicators in this study are the quality of work, the quantity of work, the utilization of time, the level of attendance, and cooperation.

There are 3 independent variables in this research, namely compensation (X1), motivation (X2), and work period (X3). The compensation (X1) indicators in this research are justice, expectation and achievement, prosperity, and spirit.

The motivation (X2) indicator in this the study covers actualization, appreciation, achievement, promotion, creativity, direction, and stimulation. Meanwhile, the work period (X3) indicator in this research is referred to the working period from the beginning of employee become civil servant until 2012 for the regression model before the performance allowances and 2013 after the performance allowances.2.3 Analysis

The data were analyzed using multiple regression test with equation (1) to test the regression model before the existence of performance allowances and equation (2) to test the regression model after the existence of performance allowances. Here are the equations of the regression model.

Y = a + b1 compensation + b2 Motovation

+ b3 Work Period + e

(1)

(2)

Further partial test (t-test) and simultaneous test (F-test) in each regression model with 95% confidence level or significance of 0.05 were carried out.

3 RESULTS AND DISCUSSION

This section presents the results of data processing and analysis to answer the research issues that have been put forward thereafter. The correlation formula of Pearson Product Moment is used for testing the validity of the questionnaire. From the validity test performed, it was found that all r-arithmetic is positive and r-count > r-table at significant value 0.05. It is therefore concluded that all item statements in the instrument/questionnaire are valid. The truth and reliability of the questionnaire were tested by Alpha Cronbach method. The reliability test showed that the value of Alpha Cronbach > 0.70. Thus, it is concluded that all items statement in this research instrument is reliable or consistent and can be used as an instrument in this research.

3.1 Classical assumption test

The first test is normality test using the Kolmogorov-Smirnov test method. From the test results, it was revealed that there is a significance value of 0.624 in the regression model before the performance allowances and 0.190 after performance allowances.

These values are significant because both values are above the value of α of 0.05, meaning that the error is normally distributed.The second test is the Heteroscedasticity test with the scatterplot test method. After analyzing the data, the scatter plot charts show that the points do not form a particular pattern on both regression models. This condition indicates that there isn’t any hetero- scedasticity in the regression model before and after the performance allowances.

The third test is a Multicollinearity test symbolized by a Variance Inflation Factor (VIF). The analysis revealed that VIF value is less than 10 and Tolerance value is more than 0.10. This condition means that all independent variables in both regression models show no multicollinearity or no linear relationship between independent variables.

The fourth test is an Autocorrelation test by calculating Durbin Watson. From the output of the regression model, the regression model before the performance allowances is 2.123 and the regression model after the performance allowances is 1.892. Whereas from Durbin Watson table with significant 0.05 and samples (n) 60 obtained dL = 1.4794 and dU = 1.6889. Durbin Watson values in both regression models are in the region between dU and 4-dU, implying that there is no autocorrelation in both regression models.

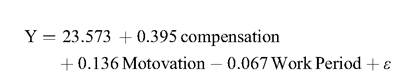

3.2 Regression model before performance allowances

The result of multiple regression test before performance allowances was obtained from the equation as follows:

Furthermore, the partial test is performed between each independent variable and the dependent variable. With t-table 1.67356, the results of partial test are as follows:

- There is a positive and significant effect of compensation on employee performance before performance allowances because t-count (1.995) > t- table with positive regression coefficient.

- There is no effect of motivation on employee performance before performance allowance because t-count (1.056) < t-table.

- There is no effect of work period on employee performance before performance allowance because -t-count (-0.151) > -t-table.

Then, another test that simultaneously investigated relationship between compensation, motivation, and work period of employee performance before performance allowance was also conducted. With the determined of F-table value of 2.77, the result of simultaneous test showed that F-count is 3.663 > F-table. Thus, it can be concluded that simultaneously, there is an effect of compensation, motivation, and work period on employee performance before performance allowance.

The next test is the determination coefficient test to determine the dependent variable explained independent of any heteroscedasticity variable. The test results showed that the value of Adjusted R Square is 0.164, meaning that 16.4% performance variables before performance allowances are explained by compensation, motivation, and work period, whereas 83.6% is explained by other factors.

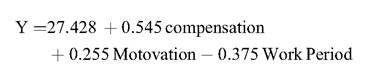

3.3 Regression model after performance allowances

Meanwhile, another focus of the study to investigate multiple regression tests after performance allowances was carried out by using the equation as follows:

After that, the partial test was carried out between each independent variable and the dependent variable. Using the determined t-table value of 1.67356, the results of partial test are:

- There is a positive and significant effect of compensation on employee performance after performance allowances because t-count (5.101) > t- table with positive regression coefficient.

- There is a positive and significant effect of motivation on employee performance after performance allowances because t-count (3.557) > t-table with positive regression coefficient.

- There is no effect of work period on employee performance after performance allowances because -t-count (-1.411) > -t-table.

Further, the study also tested simultaneously the relation between compensation, motivation, and tenure of employee performance after performance allowances. With the determined value of 2.77 for F-table and the gained result of simultaneous test of F-count (30.177) > F-table, it can be concluded that, simultaneously, there is an effect of compensation, motivation, and work period on employee performance after performance allowances.

The next test is the determination coefficient test to determine the dependent variable explained by the independent variable. From the calculation, it was revealed that the Adjusted R Square test results show the value of 0.618, meaning that 61.8% variable performance after performance allowances was explained by compensation, motivation, and work period. Meanwhile, 31.2% is explained by other factors.

The findings revealed that partially, there is a positive and significant effect of compensation on employee performance before and after the existence of performance allowances. This condition means that with the presence or absence of performance allowances, employees have a professional performance in accordance with their respective duties and responsibilities.

Before the existence of performance allowances, there is no effect of motivation on employee performance, and after existence of performance allowances, there is positive and significant effect of motivation on employee performance. This condition indicates that there is a difference in motivation in the period before and after the performance allowance. With performance benefits, employees are more motivated to work.

Meanwhile, before and after the existence of performance allowances, there is no influence of working period on employee performance. This means that the working period of employees does not affect the results of their work.

4 CONCLUSION

Before the performance allowances, compensation has a positive and significant effect on employee performance, whereas motivation and work period have no effect on employee performance. Meanwhile, after the performance allowance, compensation and motivation have positive and significant influence on employee performance, whereas work period has no effect on employee performance.

REFERENCES

Kadarisman, M. 2012. Compensation Management. Jakarta: PT. Raja Grafindo Persada.

Mangkunegaran, A.P. 2005. Corporate Human Resource Management. Bandung: Rosada Karya.

Moeherionoo, M. 2010. Competency Based Performance Measurement. Second printing. Jakarta: Ghalia Indonesia.

Suma’mur, S. 2009. Analysis of Factors Affecting Employee Performance in the Regional Personnel Agency of Central Tapanuli Regency. Jakarta: Open University, Final Project Master Program (TAPM).

Veithzal, R. 2004. Leadership and Organizational behavior. Jakarta: PT. Raja Grafindo Persada.