Finding an International Equilibrium in Times of Globalisation and Redesign of International Institutions

5.8.1 Data on GIobaIisation and Its Implications

A further channel through which the financial crisis can have an impact on stagnation is globalisation.[104] In fact, globalisation is a powerful way of transmitting shocks, crises and the tendency to stagnation from the countries or regions initially more affected to other countries or regions.

The financial crisis has shown that industrialised countries are not immune from contagion and that international imbalances can have a high cost for all countries. Regional agreements, such as the EMU, do not isolate countries from shocks but, on the contrary, may exacerbate them if they are not dealt with by appropriate institutions and policies.As largely shown by Table 5.4 (but see also Ortiz-Ospina and Roser 2016), international trade has grown remarkably since the nineteenth century. Over the course of the second half of the nineteenth century, what is commonly called the ‘first wave of globalisation' occurred, with a marked growth in world trade and foreign investment. It was fostered by technological advance and free trade policies. A halt to globalisation occurred in the period between the two world wars (not shown in the table), but after World War II, ‘international trade and investment started growing again, and in the last decades before the crisis trade expansion has been faster than ever before. Today, the sum of exports and imports across nations is higher than 50% of global production.' At the turn of the nineteenth century this ratio was below 10 per cent. After World War II, the share of exports rose very rapidly from 10 per cent in 1960 to a little more than 30 per cent in 2014, even if it suffered a drop of around 4 per cent as an effect of the global recession (UNCTAD 2016).

50

In the twentieth century, the stock of foreign capital with respect to the world's GDP moved from almost 20 per cent in 1900 to almost 80 per cent a century after (Ortiz-Ospina and Roser 2016: 1).

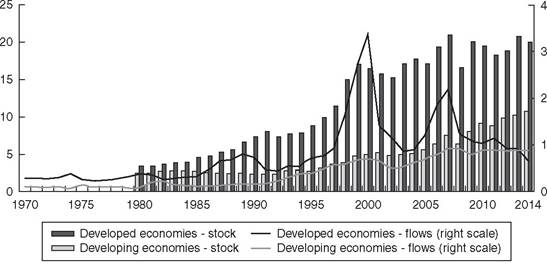

In most recent decades, the high dynamics of foreign direct investment has continued and also has involved developing economies (see Figure 5.13).Globalisation has also had a large impact on single economies, influencing the competitive position of each country (with effects on wage policy, content of production and domestic governance of social relations), changing their relative positions and then the balance of power for international governance. Globalisation represents a challenge for policymakers. It brings new opportunities but also new problems. There is no doubt that the globalisation observed in the last three decades, like the wave of globalisation around the turn of the nineteenth century, has contributed - together with technical progress - to an increase in world growth rates as a whole.[105] It has supported growth in many ways; among them, allowing information on people, available resources and knowledge to move internationally. Many developing

Table 5.4 globalisation waves in the nineteenth and twentieth Centuries (percentage change unless indicated otherwise)

| World | 1850-1913 | 1950-2007 | 1950-1973 | 1974-2007 |

| Population growth | 0.8α | 1.7 | 1.9 | 1.6 |

| GDP growth (real) | 2.1a | 3.8 | 5.1 | 2.9 |

| Per capita | 1.3a | 2.0 | 3.1 | 1.2 |

| Trade growth (real) | 3.8 | 6.2 | 8.2 | 5.0 |

| Migration (net), million | ||||

| United States, Canada, Australia, New Zealand | 17.9a | 50.1 | 12.7 | 37.4 |

| (cumulative) | ||||

| United States, Canada, Australia, New Zealand (annual) | 0.42a | 0.90 | 0.55 | 1.17 |

| Global FDI outward stock, year | 1982 | 2006 | ||

| FDI as % ofGDP (world) | - | bgcolor=white>-5.2 | 25.3 |

a Refers to period 1870-1913.

Source; WTO 2008.

238

The Challenges of the Financial Crisis

Figure 5.13 Stockand flows Ofinwardforeign direct investment as a share of global output by country group (per cent), 1970-2014. (Source: UNCTAD, 2016).

countries have in fact grown fast as an effect of catching up to the frontier of technology. This effect can be seen in Table 5.5, which shows the relative increase in income growth in the more recent decades along the progress of globalisation.

At the same time, the kind of globalisation we have experienced so far has created new risks. A risk has arisen in particular with reference to jobs, due to sudden changes in the competitive position of a given country and to the conduct of transnational corporations, which has made it difficult for the nation-state to protect labour (Beck 2015). These risks often materialise in specific sectors of more developed countries and entire less develop economies. The need for compensating losers should be stressed. In fact, ‘trickle-down of gross benefits spilling over the losers cannot be taken for granted, a reverse trickle-up is just as likely' (Nuti 2017: 4). Compensation can take a form such as that implemented by the United States with the Trade Act of 1974, establishing a Trade Adjustment Assistance Program that provided $1 billion of federal spending in 2010. This should be generalised to other countries, regions or world organisations and agreements.

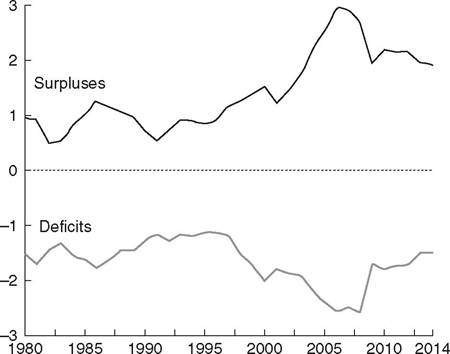

Moreover, risks derive from global imbalances of various kinds, fuelled by countries pursuing different growth strategies. External imbalances - associated with financial liberalisation and the fragility of the international financial system - represent one of the fundamental causes of the global financial crisis. Their rising dynamics, in particular, in the last fifteen years is shown in Figure 5.14.

One notable example is the sovereign debt crisis in the Euro zone, which has derived from previously unchecked capital account imbalances (Acocella 2016b).

Cross-border capital movements and financialisation of the economies have indeed increased, rather than decreased, risk. Lasting increases in imbalances of the balance of payments, favoured by other imbalances internal to each economy and also by the liberalisation of capital movements, have led to concentration of wealth, unequal distribution and crises, as discussed earlier. These, in turn, have largely come to the detriment of the welfare state (on this, see also Atkinson 2002).Drawing a balance of the benefits and costs of globalisation is a difficult task. Dollar (2007) examines case studies of several developing countries with high growth records and makes them partly depend on the growth of their populations but also on their openness and international integration. Dissenting views are also diffuse, however. Pogge (2007) emphasises the role of global institutions, which deter abatement of inequality. Thompson (2007) notes that trade and capital movements still take place mainly among developed countries - i.e. instead of globalisation, we should speak of ‘sub-globalisation’. Wade (2007) questions the correctness of the pro-market orientation of economists who hold that globalisation has led to benefits in terms of both growth and reduced inequality. In fact, he says, growth rates have slowed down, the distance between developed and less developed countries in terms of per-capita income has not reduced and most of the apparent benefits derive from the performance of China. Most likely, globalisation generates mixed outcomes,

Table 5.5 Growth of real GDP per capita at purchasing power parity, selected regions and economies, 1951-2015

| 1951- 1980 | 1981- 2015 | 1951- 1960 | 1961- 1970 | 1971- 1980 | 1981- 1990 | 1991- 2000 | 2001- 2010 | 2011- 2015 | |

| Developed economies | 3.5 | 1.8 | 3.1 | 4.2 | 2.6 | 2.5 | 2.1 | 1.2 | 1.1 |

| United States | 2.3 | 1.8 | 1.3 | 3.4 | 2.2 | 2.6 | 2.4 | 0.9 | 1.4 |

| Developing economies | 2.7 | 3.8 | 2.7 | 2.6 | 3.0 | 2.1 | 3.2 | 5.8 | 4.0 |

| Africa | 1.8 | 1.2 | 1.5 | 1.9 | 1.2 | -0.4 | 0.7 | 3.0 | 1.8 |

| America | 2.6 | 1.3 | 2.4 | 2.4 | 3.0 | -0.4 | 1.6 | 2.4 | 1.1 |

| Asia | 2.8 | 5.0 | 2.8 | 2.7 | 3.3 | 3.6 | 4.2 | 7.0 | 4.9 |

| East Asia | 3.0 | 7.1 | 4.2 | 3.4 | 4.1 | 6.7 | 5.8 | 9.6 | 6.5 |

| China | 2.3 | 7.7 | 4.1 | 2.7 | 3.1 | 6.5 | 6.2 | 11.1 | 7.2 |

| Southeast Asia | 2.6 | 3.5 | 2.3 | 1.6 | 4.0 | 2.6 | 3.0 | 4.2 | 4.0 |

| South Asia | 1.4 | 4.1 | 1.5 | 1.5 | 1.2 | 3.1 | 3.7 | 5.7 | 4.1 |

| West Asia | 4.4 | 1.4 | 3.2 | 4.9 | 3.4 | -1.6 | 1.6 | 3.3 | -0.1 |

| Transition economies | 3.2 | 0.5 | 3.7 | 3.7 | 2.0 | 0.5 | -4.9 | 6.2 | 2.1 |

| World | 2.7 | 2.1 | 2.6 | 3.1 | 2.0 | 1.5 | 1.7 | 3.1 | 2.5 |

| Memo Items: Developing economies, | bgcolor=white>2.7 2.4 | 2.4 | 2.5 | 2.9 | 1.1 | 2.3 | 3.6 | 2.3 |

excluding China

Note: The Islamic Republic of Iran is included in West Asia.

Real GDP corresponds to Geary-Khamis PPP [See United Nations, 1992). Source: UNCTAD 2016.

Figure 5.14 Global current account surpluses and deficits as a share of world output (per cent), 1980-2014.

(Source: UNCTAD, 2016).

and the balance much depends on at least three factors: (1) the period of reference, (2) the nature of the international operations considered and (3) the value judgments and preference function on which the balance is drawn.

A picture of the world economy's blocs that have emerged parallel to globalisation can be useful because it summarises existing imbalances and the recent trends prevailing in the different countries. Some played the role of net importers of both raw materials and manufactured goods (e.g. the United Kingdom and the United States); others were net exporters of manufactures (e.g. Germany, Japan, China, Southeast Asia and Brazil) or of raw materials (Russia, Saudi Arabia and many other developing countries). Growth in each bloc was supported by different factors. It was finance-led growth for net importers tout court and export led in the net exporters of manufactures. Growth of these two blocs, in turn, benefitted raw materials exporters.

In the last two decades, countries in the above-mentioned blocs had experienced different, but positive, rates of growth. These were very low in most of Europe and Japan but very high elsewhere. In general, countries in all groups experienced a rather good performance. Some countries, however, for various reasons, suffered from low or even negative growth until recently as an effect of the Great Recession. As we know from Section 5.1, this has transmitted in waves from the United States to Europe and later hit Brazil, Russia, India, China and South Africa (BRICS). More recently, positive signs of recovery have emerged in the countries that were initially hit by the crisis.

This picture of the world economy in blocs can explain why countries have suffered differently from the prospect of stagnation.

In fact, some of them devised export strategies to cope with low domestic growth of demand to the benefit or detriment of other countries. Countries receiving a benefit were raw materials exporters, mostly developing countries. Others suffered as an effect of beg- gar-thy-neighbour strategies.After 2008, the growth of the world as a whole did fall, but no bloc changed its role, and there were a few changes in their relative roles. The financial crisis has reduced growth in the net importers. Exporters of raw materials, in turn, have been hit by lower growth than net importers. Again, net exporters of manufactures performed better as an effect of their beggar-thy-neighbour strategies; however, they suffered from the growth slowdown too.

5.8.2 Policies to Deal with Globalisation

The strategies of some specific countries parallel to globalisation has already been considered. Whether the policies they implemented were the best possible ones is certainly an issue worth digging into further and difficult to answer, as this would involve knowledge of the specific situation of each. Instead of doing this, we prefer to investigate the reaction to globalisation by international institutions. How these institutions have and will cope with the developments of globalisation is, in fact, an intriguing point. As to the past, on the one hand, we should first note that a century of evolution of the international payment system represents a good guide to understanding the ability of international institutions to adapt to changes; a notable example is the IMF after introduction of a floating exchange-rate system, which, from a historical perspective, is a recent innovation. On the other hand, international institutions have been directed to a large extent to pursue not only the interests of some industrial countries in general but also, in particular, the commercial and financial interests in those countries (Stiglitz 2002).[106] This raises issues involving the equilibrium of the international system and the orientation of its governance.

Here we aim to offer some more technical reflections on how to devise a new and fair design of international institutions to cope with these and other issues arising from globalisation. These reflections refer to: arrangements to favour equilibrium, check of the correctness of existing institutions, the nature of positive and negative international spill-overs and the need to internalise them in a number of areas; progress achieved and desirable in order to pursue international policy coordination.

The need for discussing the arrangements to favour equilibrium arises, in particular, for the case of the public goods existing in a global space, i.e. global public goods, such as the environment, financial stability and the like. The traditional theory of public goods, in fact, can be recast in terms of the new theory of economic policy in a strategic context where some of the players share common targets (having either equal or different target values) that can be thought of as public goods by reason of their commonality.

52

In general, as mentioned earlier, from the point of view of the theory of economic policy, difficulties in finding a unique equilibrium or an equilibrium at all can arise. We recall that even when target values coincide, such as between countries, multiple equilibria arise in the instrument space because the number of instruments is higher than that of targets. Different target values, instead, imply the non-existence of an equilibrium in the target space (see Chapter 4).

Global public goods raise a coordination problem among policymakers on how to settle conflicts or how to converge to the commonly preferred solution. A decentralised solution is difficult to implement because the level of the public goods desired by the various countries is usually different. When that level is common to all countries, decentralisation leads to indeterminacy and destabilisation (if not collapse) of the system if the players randomise their policies in response, unless specific circumstances occur or can be imposed that make it possible to reach a decentralised equilibrium.

The necessary circumstances include the case where some players voluntarily abstain from making use of their instruments (Acocella and Di Bartolomeo 2011), as with the Bretton Woods system. In fact, the arrangements established at Bretton Woods did so for more than a couple of decades, since the United States acted as a hegemon, abstaining from controlling its balance-of-payments deficit. The arrangements that followed have not ensured equilibrium for a number of reasons: a notable one - in addition to the well- known Triffin dilemma - was the lifting of limits to capital mobility and the features taken by globalisation, which have added to the problems to be faced; or the players were forbidden to use their instruments for some reason. As opposed to these situations, the tendency to ensure an equilibrium was facilitated by introduction of some additional (possibly common) targets that changed the nature and contents of the game, creation of a mechanism for announcing the strategies to be played (as in international forums) or the existence of situations in which politics, history, conventions and path dependence act as the constraints that provide for a ‘smooth’ solution.

A centralised solution always exists from an abstract point of view, as the exceeding instruments could freely be set and the distributive problems (deriving from the conflict) solved. However, such a solution would be difficult to obtain in an international context like the current one, as there is no such thing as a superstate to deal with conflicts, and resistance to the devolution of powers to an external authority is extreme, unless very specific situations and issues occur.

Moving on now to consideration of the suitability of existing international institutions, we can say that the correctness of current institutions - and the theoretical assumptions on which they are based - can be questioned from a number of points of view. First, current institutions are unable to reallocate demand across economies in order to generate growth. Moreover, freely floating exchange rates cannot support demand and act as a shock absorber. Finally, free international capital movement cannot improve the global allocation of capital and make international adjustment smoother. All three assumptions have been questioned by the experience of the last decades as well as recent research.

In particular, as to the first point, the capacity of the global economy to sustain an appropriate pace of global growth has been questioned because of the export-led strategies implemented by some countries, generating high savings and a low interest-rate trap.[107] As to the second point, global interconnections seem to have altered the shock-absorbing role of floating exchange rates. The third point is tied to the first one (due to the symmetry between the current and capital accounts of the balance of payments), but we dealt with it earlier (for all three points, see Cmure 2015).

As for spill-overs, they can be either negative or positive. Tax havens - which largely continue to act in a number of places, not only in underdeveloped but also in European countries - generate issues of the former type, as they reduce the tax base and the tax proceeds for other countries and sometimes also divert investment, while feeding, and adding to, other sources of unstable (and sometimes illegal) capital movement. This is particularly to the benefit of corporations, which can elude taxes by manipulating transfer prices relative to their intracorporate transactions.

Spill-overs of a positive kind can, instead, derive from fiscal expansion in one country. Especially in a situation such as the current one, characterised by low demand and interest rates, such an expansion can have a beneficial expansionary effect in other countries. Certainly, the open-economy multipliers are lower than those for a closed economy, but this should favour simultaneous expansion by many countries. International coordination thus could add to the expansionary outcomes in a remarkable way (see Eggertsson, Mehrotra and Summers 2016; Gaspar, Obstfeld and Sahay 2016).

A redesign of international institutions should take place to realise the potential for good of globalisation while reducing or eliminating its shortcoming and the distortion of its current governance. Both authors and policymakers have become aware of the numerous holes in the current

suggest a direct role for multilateral surveillance. ‘This process can play two potentially useful roles: first, as a discussion of the differences in assessments; second, as a potentially useful commitment device for countries to implement some of the required but politically unpalatable fiscal or structural adjustments.' governance, but policy responses show some inertia. For example, concern for the free mobility of capital has arisen. The need for limitations has been urged (among others, see Cmure 2015; Stiglitz 2015a) via the use of instruments (such as regulation tending to avoid volatile capital flows and taxation) reducing negative externalities and increasing the effectiveness of domestic policies (in particular, monetary policy). A similar position is shared by the IMF, which has recently altered its previous position in favour of full capital market liberalisation and fiscal consolidation towards a more cautious, or even negative, attitude. The new position is justified especially in view of the negative effect of these policies on inequality, which also hurts the growth rate and its sustainability (Ostry, Loungani and Furceri 2016).

By contrast to the free mobility of capital, take the limited mobility of persons. In some areas (such as the European countries that are members of the ‘area of Schengen'), mobility of persons has been put in check recently by the wave of immigrants from developing countries, in particular, those hit by war and repression, and lack of a common attitude. Immigration is the single most relevant and hot issue - even more prominent than that of free capital movement - that should be the object of international coordination. It could be allowed to some extent in advanced countries, which should also act on its economic and political roots, in particular, by aid to development in order to contain or reduce it.

Apart from action for immigration, international coordination can indeed be initially limited to the areas where it is most needed, such as central bank policy (Claessens, Stracca and Warnock 2015; Engel 2015),[108] tax harmonisation in particular within regional institutions (Keen and Konrad 2012; Karakosta, Kotsogiannis and Lopez-Garcia 2014; Benassy-Quere, Trannoy and Wolff 2014), financial regulation (Davies and Green 2013; Schenk 2016), environmental issues (United Nations Environment Programme 2015), anti-monopoly action and, as said, freedom of capital movement (Ostry and Ghosh 2013).To face and solve these and other problems, at least three points must be discussed that have a practical relevance: (1) whether limited amendments to the existing institutional architecture are sufficient or a new architecture needs to be designed, (2) whether a change in the rules of the game and the relative roles of different countries will be required and (3) how to devise institutions that can ensure both fairness and progress in a stable context.

The answer to the first two issues, as far as monetary institutions are concerned, is that much depends on whether China and other BRICS countries will continue to push towards a new balance of power within the existing institutions. From this point of view, the Renminbi (RMB or yuan), the Chinese currency, has been recognised as a new reserve currency. Any prospect of rivalry with the dollar is certainly premature. However, in due time, an uneasy duopoly between the dollar and the RMB could arise. This prospect appears to be rather new in the world economy[109] and may require changes in the rules of the game. In the past, equilibrium and stability depended on the dominance of only one currency and its hegemony. Big issues arise having to do with volatility, trade imbalances and the new rules that, in turn, have an influence on political stability. Issues of a more limited nature arise with reference to coordination in specific sectors. Other issues arise about the way to facilitate the transition and the reforms of national policies and regional or international institutions such as the IMF needed for achieving this.[110]

As to the third issue, the actual development of international institutions, it seems to have disregarded the need for more fairness, stability and steady growth. Principles for devising a new order are therefore needed at various levels. Most discussions and the limited changes made so far (even after the crisis) have aimed only at constraining member countries to act in a way that is not detrimental to others in certain areas, as in the case of tax havens or environmental protection, with very limited achievements in both areas.[111] Some progress has been made for coordination of anti- monopolistic policies through the International Competition Network, established at the WTO Doha Round of negotiations. The participants of these negotiations agreed on a guidance document on investigative process that reflects key tools and procedural fairness principles. To some extent - i.e. apart from the influence of vested interests - the limitation in international agreements seems to derive from absence of a clear and shared concept of fairness, consistent over time, when the institutions were founded or reformed.

The existing asymmetries have become codified. Principles of responsible behaviour that take account both of the initial position of a country and the policies implemented by that country appear to be lacking. They should involve not only deficit countries but also those running surpluses. Symmetric adjustment would avoid the risk, on the one hand, of lasting inefficiencies and, on the other, of surplus countries regarding global institutions simply as an insurance mechanism that allows them to devise export-led strategies in a way that is less reactive to negative shocks and avoids taking the expansionary adjustments that would be needed to reduce their international imbalance. As to the specific imbalances of developing countries and, more generally, to the need to ensure a higher world liquidity and international regulation coordination of policies, the Stiglitz Commission established by the United Nations has recently suggested a number of solutions (see United Nations 2009).

This raises a more general issue, that of ensuring a number of requirements, beyond the targets and target values expressed by the policymakers of each country and referred to their relations or to issues relative to each country that derive from theories of justice. These may consist, first, in helping to boost living standards and ensuring democracy. In particular, as far as the first such target is concerned, the relative positions of less developed countries deserve specific attention not only for reasons of fairness but - as mentioned earlier - because aid to development also could help more developed countries to face some problems, such as that of the excessive flows of immigrants.

To the targets already indicated, i.e. boosting standards and ensuring democracy, self-determination within the nation-state could be added. However, Rodrik (2000, 2002, 2011) has shown that a trilemma of the global economy would then arise, as nation-state self-determination, democratic politics and full economic integration are mutually incompatible. If we deem the latter two requirements to be basic, the first one should be abandoned: global markets need global governance. A larger role of the nation-state requires a kind of ‘Bretton Woods compromise', with some limits to integration (Rodrik 2 0 00, 20 02, 2011).[112] Full integration would require dropping either democratic choices within nation-states or stronger world governance. Insisting on self-determination of people and countries would add to this prospect.