Dealing with Secular Stagnation

This topic has again come to the forefront in recent years. In fact (despite the recent recovery from the Great Recession), especially Japan and the Euro zone - but also some other countries, as an effect of the international links - will probably experience low growth for a number of years, facing lasting low demand and low real interest rates and potential growth.

Stagnation is not a new phenomenon. Concern with it emerged at the beginning of the twentieth century (and most classical economists were concerned about the possible advent of a ‘stationary state' as a negative prospect[94]); in the 1930s and again in the 1970s, in this case associated to inflation; and in 1990s, this time mainly in Japan and Europe. Now, however, the problem is deeper and more widespread, and economists have begun to talk again of a global secular stagnation.[95] Larry Summers, in particular, has insisted on the reality of this prospect (Summers 2014a, 2014b), even if his arguments have been questioned by Bernanke (2015) and others.[96]Eichengreen (2015) suggests discussing four possible causes of stagnation, which he defines as a downward tendency of real interest rates, reflecting an excess of savings over investment: a rise in savings rates due to the higher propensity to save of emerging markets, a decline in attractive investment opportunities or in the relative price of investment goods and a decline in the rate of population growth. This implies that both the demand- and the supply-side perspectives are relevant.[97]

The Great Recession has raised the issue of a prospect of stagnation through its hysteresis effects, which makes falling GDP have a negatively influence on potential output (Krugman 2014a; Fatas and Summers 2016a).[98] In fact, the median loss in potential output in 2014 among the nineteen OECD countries experiencing a bank crisis over the period 2007-11 has been estimated to be 3.75 per cent, which is to be contrasted with an estimated loss across all OECD countries of about 2.75 per cent in the same year (Ollivaud and Turner 2015).

However, Ollivaud and Turner argue that the most adverse effects derive from a lower productivity trend. Thus, technological progress - the main source of this trend - should also be taken into account, but its role is difficult to assess. Some authors are critical about the possibility of continuing to have high rates of productivity growth in the future. Data are difficult to collect, as indicators such as research and development (R&D) expenditures and patent registrations can be biased and misguiding, and some other measures of productivity growth may be illusory, concerning largely tertiary sectors, where productivity is difficult to be assessed due to absence of material content (Cowen 2011). According to Gordon (2014), productivity growth in the next decades is predicted to be as high as it was in the five previous decades. However, to some extent, the effects of technological progress may appear less relevant in some countries, namely, the innovation leaders, due to the geographic distribution of its implementation in a globalised world. In fact, innovations devised in one country - such as those derived from information technology - can be implemented in other countries due to decentralisation of production. In addition, technological progress appears to be more relevant for investment than for consumption goods, where the weight of services tends to grow, which is consistent with the secular decline in the price of investment goods (Eichengreen 2015).

Also demographics can have an impact on the secular stagnation that, according to some authors, can be even more important than that of technology. Ageing and the increased life expectancy have been shown to be the main demographic trends in many countries, especially in Europe, the United States, Japan and China. They have an uncertain effect on net aggregate demand and on real interest rates. As a matter of fact, these factors have decreased to very low levels in the last three decades. However, the a priori impact of demographic trends is complex; on the one hand, increased savings can derive from the section of the population having a higher propensity to it, due to the increase in longevity; on the other hand, the larger share of older people - having a lower propensity, consistent with the life-cycle theory (Modigliani and Brumberg 1954) - will act in the opposite direction.

The net effect on real interest rates is therefore uncertain (Favero and Galasso 2015), the more so - we can add - as account should be taken of possible changes in the retirement age, some of which are already being implemented. A final effect of demographic trends is to be noted: reduction in the working cohorts of the population lowers their direct contribution to growth, unless the retirement age is prolonged. Intuition thus suggests that an ageing population can reduce growth. However, in practice, this is not so, as the positive effect of higher automation - in response to the demographic trend - can counteract this effect (Acemoglu and Restrepo 2017).Rising inequality in both developed and less developed countries (even if inequality between them has decreased) has reinforced these negative effects. In fact, the increasing concentration of wealth and income in the hands of the top 1 per cent has led to under-consumption, and/or over-saving (Piketty 2013).41 The rise of financialisation and monopoly capitalism has also been suggested as a factor underlying both rising inequality and under-consumption (Foster and McChesney 2012). The negative impact of inequality on growth mentioned earlier is an additional cause of stagnation.

Overall, with respect to the debate about the causes of secular stagnation, institutional aspects and political mistakes are also to be considered. Secular stagnation was surfacing in some regions such as Europe and Japan in the last couple of decades. In the former case, it was mainly an effect of the deflationary design of institutions and to some extent of wrong policies (De Grauwe 2013, 2015). Crafts (2014) emphasises that the risks of stagnation are greater for Europe than for the US hypochondria, due to a number of factors, among which institutional factors such as the burden of fiscal consolidation and the ECB's focus on low inflation. More recently, Ferrero, Gross and Neri (2017) have shown the impact of demographic factors in Europe.

In Japan, wrong policies as well as the effects of ageing population prevailed.[99] [100]Other barriers to growth can be education, increasing government debt, energy shortages and the environment.43 In particular, as to education, Gordon (2014) complains about the rising number of dropouts in the United States.44 Education and productivity growth are the focus of Mokyr (2014). As in the past centuries, progress in science and technology will have indirect beneficial effects on productivity that can outpace the direct effects in the long run.45 However, this will polarise labour markets and require proper education to deal with the rise of new jobs and the loss of previous qualifications.

We can add that many countries have limited their public deficits, in particular, in order to comply with institutional limits, just by curbing public investment and, within it, the items that are more sensible for productivity growth, such as educational expenditures, due to the relatively larger flexibility in their management with respect to almost fixed current expenditures. From this perspective, Fatas and Summers (2016b) underline the permanent effects deriving from fiscal consolidation.

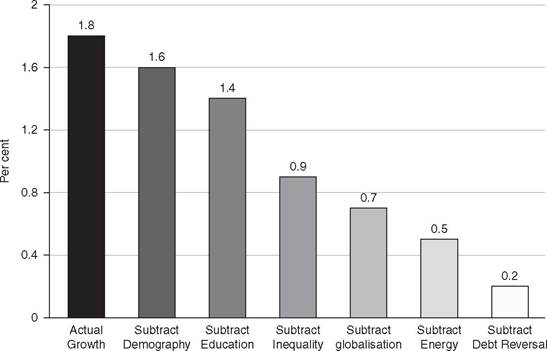

Gordon (2012) has made an exercise of considering the effects on the supply side of most of the factors that did support growth of the US economy in the two decades after

number of wrong monetary and fiscal policies but underlines that these were minor mistakes compared to those committed in the United States and Europe (Krugman 2000, 2014b). Other authors stress in addition to the ageing demographic, over-reliance by local governments on transfers from the central government and capital requirements. These made Japanese banks reluctant to lend money to start-up businesses and small and medium-sized enterprises, which discouraged Japanese innovation and technological progress (e.g. Yoshino and Taghizadeh-Hesary 2015), possibly the most important cause of Japanese stagnation (Tyers 2012).

43 From the point of view of a specific country such as the United States, the interaction of globalisation and the ICT technology also can be of a problem, as it has caused or facilitated outsourcing.

44 In this perspective, we can recall what we noticed earlier about the increasing number of NEETs in OECD countries after the crisis.

45 If this is the case, hysteresis of supply could produce a situation of prolonged deflation and reduction in employment when aggregate demand does not keep pace with increasing supply (Buiter, Rahbari and Seydl 2015).

1987 and should no longer apply in the future. This allowed him to foresee a prospective future annual rate of growth of consumption per head for the 99 per cent of lower-income earners, which drops from 1.8 to.2 per cent (see Figure 5.12).

Some changes in these determinants may be possible, but, as we will see, this mainly depends on political ‘winds' and the policies that will be implemented. Possibly, some pressing - derived from international coordination - on countries with low debt and current account surpluses to raise demand could be useful, as indicated in international forums (Bernanke 2015), but we agree with Buiter, Rahbari and Seydl (2015) that international coordination is a difficult task on these matters.

With reference to monetary policy, recent experience suggests that the ZLB matters more than previously thought, following the secular decline in real interest rates (Laubach and Williams 2016).46 All this implies that ‘it could be a very long time before “normal” monetary policy resumes' (Krugman 2014a: 66). Only a credible promise of a high enough inflation rate that reduces real interest rates would produce an economic boom, which would yield the target inflation. As Krugman says, the promise of a high inflation rate should be credible, as to involve ‘a strong element of self-fulfilling prophecy'.

Some authors (Buiter, Rahbari and Seydl 2015) are sceptical about a rise in inflation rates as a way to go beyond the ZLB and suggest instead lowering the policy rate below zero.

However, the difficulties of implementing the policy of a negative interest rate are high. Apart from their being ‘stupid' for shrinking bank's capital, with all the consequences that can be imagined (Stiglitz 2016), the resistance of some sections of the finance46 One must be aware, however, that these estimates - and their possible consequences for secular stagnation - are characterised by a considerable degree of uncertainty, even if they use the same methodology developed by Laubach and Williams in a previous paper, as shown by Holston, Laubach and Williams (2017) with reference to the United States, Canada, Europe and the United Kingdom and Belke and Klose (2017) with reference to the Euro zone countries only.

Figure 5.12 Components of growth in per-capita real GDP, 1987-2007.

(Source: Gordon 2012)

sector and the population may be very powerful - especially in countries having a high propensity to save and/or an ageing population. In addition, one of the reactions to such policy could be hoarding of cash balances with possible bubbles under certain conditions. Finally, a negative interest rate would lower lending to firms and the government.

A policy on a target rate of inflation that is higher than that hitherto chosen by policymakers should be different from simply temporarily tilting people's expectations of a higher inflation rate when the ZLB is reached, to be achieved through forward guidance or a policy framework based on history dependence, as indicated by Woodford (2013) and others (Bayoumi et al. 2014). It should involve a longer period of time and would either face less resistance, if the rate promised is not too high (being more subtle to be understood by many sections of the population), or generate self-fulfilling expectations of a high enough inflation, as suggested by Krugman (2014a).[101] In addition, it would have a number of advantages. The promise to implement a very expansionary monetary policy, consistent with this policy, could better fight contractionary factors still at work in the short run and the associated hysteresis. This would not be because a more expansionary monetary policy and a higher inflation target would reduce the probability of future real policy rates not to be low enough to give an incentive to investment.[102] In fact, a negative policy rate could do the same. A higher inflation rate would instead help to release the burden on fiscal policy and the extant public debt (see Chapter 3), avoiding the need of making recourse to consolidation, which would certainly cause negative short-run effects and activate the loop crisis stagnation. At the same time, a higher target inflation rate would unlock fiscal policy for short-term use. This would be very useful at least for deep recessions, when fiscal policy is most effective and should largely be self-financing. It would also facilitate the task of monetary policy, which has limited effectiveness or can result in incentives to asset bubbles, especially if prolonged (Rawdanowicz, Bouis and Watanabe 2013).[103]

On the side of demand, both conventional and unconventional monetary policies should be implemented, in addition to fiscal policy. From this point of view, their coordination, which also could take the form of helicopter money, seems to be ideal (see also Buiter, Rahbari and Seydl 2015).

Structural reforms are also needed. Public-sector efficiency should be raised. Improving material and immaterial infrastructures is another field of action (Buiter, Rahbari and Seydl 2015). A necessary reform is also restructuring of public debt, which can reduce its overhang. As to fiscal consolidation, Ostry, Loungani and Furceri (2016: 40) say that ‘the short-run costs in terms of lower output and welfare and higher unemployment have been underplayed, and the desirability for countries with ample fiscal space of simply living with high debt and allowing debt ratios to decline organically through growth is underappreciated'. In the field of distribution, all the instruments directed at reducing inequality should be implemented (see Section 5.5). Gottfries and Teulings (2015) suggest extending retirement age and pay-as-you-go benefit systems.

Structural reforms take time to materialise but in some cases can entail immediate positive demand effects (Bouis et al. 2012) and can boost potential output in the longer term. Some structural reforms have different effects according to other circumstances, such as the cyclical contingency or the level of protection in other markets. This can be the case when reducing unemployment support or the difference in provisions for permanent and temporary workers, which could have negative short-run effects in ‘bad times'. Product market reforms can reduce employment under weak job protection. This finding points to substitutability between product and labour market reforms; i.e. a combination of reforms would yield smaller long-term gains than the sum of the effects of each of them taken in isolation.

Policies towards secular stagnation also must be assessed from an international perspective. In fact, stagnation in a country also spreads its effects to other countries, through a higher real exchange rate that reduces net exports and thus shifts the AD curve inward in the country first experiencing it. A similar contractionary effect derives from capital inflows, possibly associated to a net trade surplus abroad (Eggertsson, Mehrotra and Summers 2016).

A general issue then arises: whether alternative policies and international institutions can be conceived of that reduce the prospect of stagnation while avoiding the risk of financial imbalances and new financial crises. This also calls for some kind of regulation. Both aspects - rapid growth in some countries and regulation issues - are relevant for a new design of world governance. The latter is the object of the next section.

5.8

More on the topic Dealing with Secular Stagnation:

- The secular transposition

- Contents

- 15 Rise of the Secular Modernists

- DAP AND SECULAR NGOS: LIBERAL RIGHTS AND SECULAR FUNDAMENTALISM

- DEALING WITH POISONS

- The Bourbon Empire

- 19 The Quest for Europe

- Reform and Counter-Reform

- Justifiable Inequality? Five Attempts to Defend the Prohibition of the Veil

- The Religious Crisis