Indonesia

Resilient growth amidst improved fundamentals

| GDP | USD1319.1bn (World ranking 16) |

| Population | 275.5mn (World ranking 4) |

| Form of state | Presidential Republic |

| Head of government | Joko Widodo (President) |

| Next elections | 2024, Presidential and legislative |

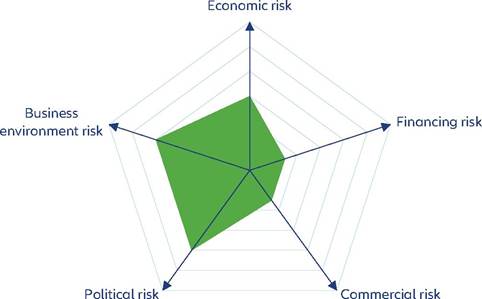

Strengths & weaknesses

Economic overview

Solid levels of growth in coming years

Indonesia has shown relatively strong GDP growth rates over the past two decades, averaging +5.2% in the 2000s and +5.4% in the 2010s.

However, it was severely affected by the Covid-19 pandemic, suffering a -2.1% full-year contraction in 2020. 2021 saw a moderate recovery, with GDP growing by +3.7%. The momentum continued in 2022 with GDP growing by +5.3%. Growth took a small step down in 2023 (likely to +5%), on the back of a resilient consumer sector but slowing external demand. We expect Indonesia to continue to register solid levels of economic growth, nearing +5% in 2024-2025, on the back of a strong consumer base and easing inflation, investment in the context of global supply-chain diversification and a moderate rebound in global demand.

After expanding to around 6% of GDP in 2020, the fiscal deficit has been narrowing in recent years and returned close to the pre-crisis long-term average of around 2% in 2022. Increases in direct taxes, new commodity export levies, removal of income assistance expenditure and higher corporate tax revenue are keeping the fiscal deficit in check.

This is likely to help gradually reducing the public-debt-to- GDP ratio.In terms of monetary policy, Bank Indonesia (BI) started a tightening cycle in the second half of 2022, against inflationary pressures and to stabilize the rupiah. A cumulative 250bps of rate hikes have been applied until October 2023. We expect no further increases as inflationary pressures ease and the rupiah stabilizes against the US dollar and 50bps worth of rate cuts are likely in the second half of 2024.

No imminent risk from structural vulnerabilities

Indonesia's short-term financing risk is deemed moderate. Though not in alarming states, the following areas of structural macroeconomic vulnerabilities are worth monitoring: (i) fast-rising domestic credit and (ii) FX reserves for rupiah stabilization and external repayment. The long history of reliance on external financing led to this vulnerability, especially under episodes of downwards pressure on the rupiah.

On the back of wider fiscal deficits and the recovery in domestic demand, real domestic credit growth increased rapidly from the beginning of 2021, though it has slowed down since the middle of 2022. The public debt-to-GDP ratio rose from 30% pre-pandemic to about 40% in 2022. Efficient fiscal consolidation since then allowed to stabilize the public-debt-to-GDP ratio and we expect a gradual decline in the coming years. On the external side, the annual current account balance was back in positive territory in 2021-2022 (after a decade of deficits) and is likely to register much lower deficits over 2023-2025 compared to the pre-pandemic long-term average. That said, FX reserves have not kept pace with the growth of imports in recent years. As a result, import cover dropped from ten months at end-2020 to 5.6 months in late-2023. The latter is still an adequate ratio but the indicator requires monitoring. Meanwhile, Indonesia's reliance on commodity exports also makes it vulnerable to a reversal in global commodity prices that could undermine investor confidence and external repayment capacity.

Business environment and political developments

Indonesia's business environment is ranked above average in our assessment of 185 economies. The Heritage Foundation's Index of Economic Freedom survey 2022 assigns Indonesia rank 66 out of 185 economies (it climbed from 2017 to 2020, but went down since 2021), given its good performance in government spending, fiscal health and tax burden, though weaknesses remain in government integrity, judicial effectiveness and labor freedom. Meanwhile, the World Bank Institute's annual Worldwide Governance Indicators survey indicates that government effectiveness, regulatory quality and rule of law have improved since 2011. Though the government has taken policy actions to achieve net zero emissions by 2060, environmental sustainability remains in bad condition, considering Indonesia's coal-dominated energy mix and industry reliance on natural resources.

The next presidential election will take place in February 2024, which will test the political stability Indonesia has achieved in recent years and challenge the wave of liberalizing reforms. Indonesia has traditionally been inclined towards protectionism of key industries and natural resources. Over his two terms in office, current President Joko Widodo (known as Jokowi) has pushed consensus on this issue further towards acceptance of higher levels of foreign investment, especially in industries downstream of primary goods extraction. However, after the election, there is the risk that the next government could tighten laws on foreign ownership and investment, as protectionist views still persist strongly among the political class. That said, in the baseline scenario (based on latest polls), the next president is likely to be current defense minister Prabowo Subianto, who has committed to continue Jokowi's policies. We would also watch out for potential protests and unrest if the election result is close.

More on the topic Indonesia:

- MUSIK ISLAM AND MUSIK ISLAMI

- Acknowledgements

- CLITORAL RELATIVISMFEMALE GENITAL MUTILATION IN “TOLERANT" ISLAMIC INDONESIA

- Backdrop as foreground: environment and histories of imperialism

- Discrimination

- Conclusion

- Bui Ngoc Son, Malagodi Mara (eds.). Asian Comparative Constitutional Law, Volume 1: Constitution-Making. Hart Publishing,2023. — 495 p., 2023

- THE PORTFOLIO CONCEPT

- Flaying, Blinding and Impaling: Royal Women and Court Eunuchs

- Buddhist Violence in Sri Lanka, Myanmar, Bhutan and Tibet