India

Unlocking the growth potential

| GDP | USD3416.6bn (World ranking 5) |

| Population | 1 417mn (World ranking 1) |

| Form of state | Federal parliamentary republic |

| Head of government | Narendra Modi (PM) |

| Next elections | 2024, general |

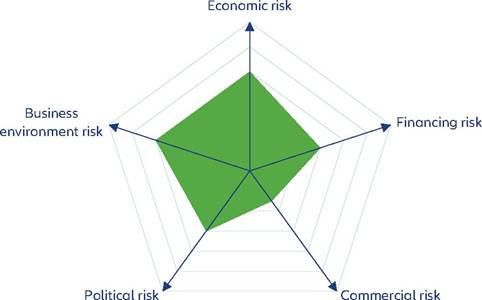

Strengths & weaknesses

Economic overview

India to become the second-largest economy in Asia-Pacific region by 2030

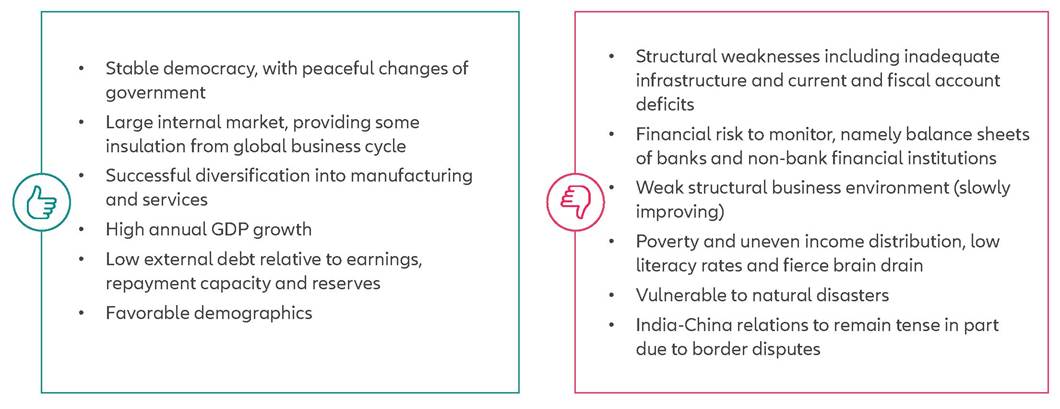

The Indian economy is a good performer among emerging economies, with +6.5% growth on average over 2000-2019 and +6.9% over 2010-2019 (in line with emerging Asia).

However, the Covid-19 crisis hit India badly and the economy was already in a vulnerable state at the end of 2019. The resulting contraction in GDP was among the deepest in the Asia-Pacific region. A partial recovery was thereafter delayed by a renewed outbreak of Covid-19 (the Delta variant). Despite a moderation in growth in 2022, India's economy remains resilient and outpaced the average growth rate among emerging economies and Asian economies. We expect India to grow by +6.9% in FY23-24 and +6.3% in FY24-25, in the context of moderating domestic and external demand. That said, public spending, foreign investment and easing inflation will be tailwinds. Over the longer run, we expect India to become the second-largest economy in the Asia-Pacific region by 2030. Five game-changers could shape India's mid-term economic outlook: foreign investment, trade, human capital, climate change and geopolitics.In terms of public policies, measures had been put in place to dampen the negative impact of the Covid-19 crisis. The fiscal deficit has declined slightly since, but public spending remains elevated (ahead of the general election in April-May 2024), supporting energy, transport and infrastructure and measures for households. On the monetary side, after policy tightening to contain inflation (250bps of cumulative rate increases between May 2022 and February 2023), we expect the Reserve Bank of India (RBI) to start cutting the policy rate in the second half of 2024. This will help ease financial pressure on households and businesses.

Structural vulnerabilities in check but to keep in mind

Overall, indicators show that the financing risk is low in the short-term. In the medium run, the indicators that need monitoring are (i) public finances, with an exceptionally large (albeit declining) fiscal deficit; (ii) the financial sector and non-performing assets and (iii) the current account deficit and moderate foreign direct investment inflows (for now).

We are particularly wary of the leeway for and efficiency of policy stimulus on both the fiscal and monetary sides. Public debt shot up with the Covid-19 crisis and seems to be stabilizing at the high level of around 80% of GDP (vs. c.70% before the pandemic). Resilience of the financial sector has improved since 2022 but needs to remain monitored (the system-wide gross non-performing-loans ratio came down to 3.9% in March 2023 from 5.9% in March 2022). Banks need reinforcing of their capital and liquidity positions against potential stress. The current account deficit is expected to narrow but remain around 1% of GDP in the coming few years. More broadly, foreign direct investment inflows are moderate for now, but adequate liberalizing reforms in a potentially favorable geopolitical environment could allow India to attract large amounts of foreign investment in the coming years.

Business environment and political developments

India's business environment is close to the median in our assessment of 185 economies, with little change over the recent years.

The Heritage Foundation's Index of Economic Freedom survey in 2022 assigns India rank 131 out of 184 economies (slightly deteriorated from 123rd in the 2021 survey), reflecting good scores with regards to the tax burden, government spending, trade freedom and monetary freedom though weaknesses remain with regards to fiscal health, investment freedom, financial freedom and government integrity. Meanwhile, the World Bank Institute's annual Worldwide Governance Indicators survey indicates scores since 2019 that have stagnated in the control of corruption and slightly improved in regulatory quality and the rule of law (all in the 45%-55% percentile range). Our proprietaryEnvironmental Sustainability Index puts India at rank 175 out of 202 economies, reflecting better performance in energy use per GDP and CO2 emissions per GDP, but weaknesses in terms of climate change vulnerability, renewable electricity output and the recycling rate.

The ruling Bharatiya Janata Party (BJP) is likely to stay in power and renew its term at the general election in April- May 2024. Narendra Modi, prime minister since 2014, should remain the dominant figure in the government. Given his strong popularity and the lack of an effective political opposition, the stability of this government is unlikely to be rattled in the coming few years. We would watch out for potential episodes of the BJP intensifying its Hindu nationalist agenda, potentially generating communal clashes - though unlikely to spark large-scale social unrest.