Hungary

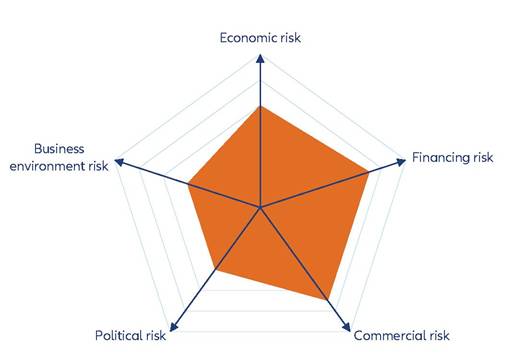

Macroeconomic imbalances remain a cause for concern

| GDP | USD178.8bn (World ranking 58) |

| Population | 9.7mn (World ranking 94) |

| Form of state | Parliamentary Republic |

| Head of government | Viktor Orban (PM) |

| Next elections | 2026, Legislative |

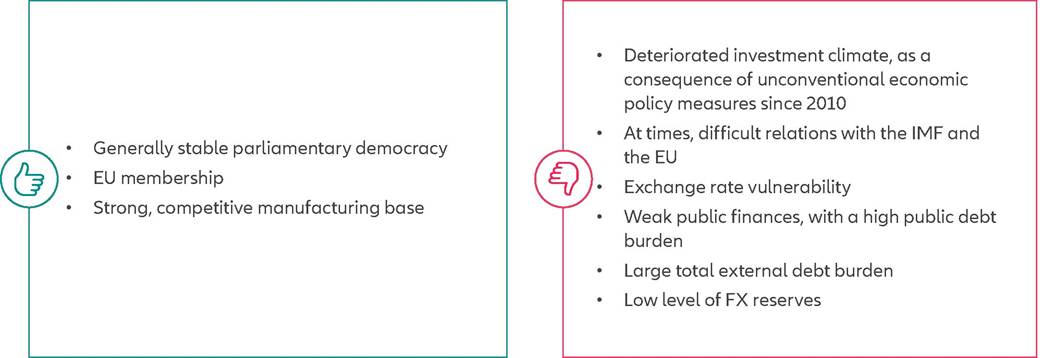

Strengths & weaknesses

Economic overview

From recession to gradual recovery

Hungary is a modest performer among emerging economies and its high dependence on exports, in particular on automotive shipments, causes above-average cyclical fluctuations in growth.

Real GDP expanded by an average +2.1% over the past 20 years though the performance was better over the last five years prior to the Covid-19 pandemic (+4.1% on average, on par with the average of the Central and Eastern European EU member states). While the global Covid-19 crisis affected the Hungarian economy markedly in 2020 (-4.5% contraction), it rebounded strongly with a +7.2% output increase in 2021. However, Hungary's economic prospects have considerably worsened since war broke out in Ukraine. This is mainly due to the country's heavy (prewar) energy-import dependence on Russia and the impact of EU sanctions against Russia on the domestic economy. In 2022, economic growth in Hungary still held up better than initially expected (+4.6%) thanks to robust consumer and public spending as well as external demand. However, the impact of surging inflation, rising interest rates, sluggish external demand and deteriorating business confidence took full effect in 2023. Real GDP contracted by an estimated -0.6%, largely driven by plunging consumer spending and investment activity. Looking ahead, GDP is forecast to expand by just over +2% in 2024 and about +3% in 2025, mainly thanks to improving investment and consumer spending on the back of falling interest rates and recovering real income growth.Inflationary pressures will decline but remain on the cards in

2024. Consumer price inflation rose into double-digit territory in May 2022 and remained there until September 2023, with a peak of 25.7% y/y in January 2023, the highest rate seen in the EU. It was driven by surging energy and food prices combined with a weakening forint (HUF, the local currency) in 2022 that pushed up import costs. The Magyar Nemzeti Bank (MNB, the central bank) began monetary tightening earlier than peers in the region (in June 2021) and eventually also more decisively - it hiked its key policy rate from 0.60% in May 2021 to 13.00% in September 2022 and the overnight lending rate to 25.00%. Meanwhile, in Q4 2023, inflation fell rapidly to 5.5% at year-end and the MNB was one of the first central banks in Europe to embark on a monetary easing cycle. Going forward, we expect the disinflation process to moderate and forecast annual average inflation of just under 5% in 2024 and 4% in 2025. In line with that, the MNB is likely to continue a gradual easing cycle.

Worrisome public and external finances

Hungary's public finances have become a cause for renewed concern after the Covid-19 crisis reversed eight years of fiscal consolidation. The annual fiscal deficit had been smaller than -3% of GDP since 2012, resulting in a gradual improvement of public debt from the peak of 80% of GDP in 2011 to 65% in 2019. Owing to large fiscal stimulus measures in response to the Covid-19 crisis, annual budget shortfalls of -6% to -8% of GDP were recorded in 2020-2022, pushing public debt up again to 79% of GDP temporarily. Government stimulus measures in response to the higher energy costs and inflationary pressures since 2022 and the recession in 2023 have been smaller than the previous measures, mainly because financing costs have markedly increased.

Nonetheless, the annual fiscal deficit is estimated at over -5% of GDP in 2023 and forecast at -3% to -4% in 2024-2025, keeping the public debt-to-GDP ratio at around 70%.Despite a swift rebalancing of the current account in 2023, Hungary's external position remains a cause for concern. As Hungary's import bill began to rise in 2021-2022 owing to surging energy prices, the current account deficit widened substantially to -4.1% of GDP in 2021 and -8% in 2022. But thanks to lower energy import prices and reduced imports due to the economic recession, the current account improved substantially and is estimated to have come in roughly balanced in 2023. Looking ahead, the external balance is forecast to return to small annual deficits in 2024-2025 on the back of the expected recovery of domestic demand and imports. What remains a concern, however, is Hungary's gross external debt in relation to GDP which surged from an already high ratio of 97% in 2019 to over 160% in 2020 and is currently estimated at about 140%. Even if we exclude intercompany debt liabilities to foreign parent companies, the remaining external debt stands at a still comparatively high ratio of more than 60% of GDP currently. Meanwhile, the biggest concern is Hungary's low level of FX reserves. At the end of 2023, they covered less than three months of imports or, in other terms, less than all external debt payments falling due in the next 12 months (below both the benchmark "comfort" levels of four months and 125%, respectively).

Deteriorating business and political environments

The Hungarian business environment is just above average. Increased state interference in the economy through frequent and arbitrary policy changes (for example sectoral taxes, pension nationalization, mortgage pre-payment schemes, utility tariff cuts and the weakening of institutions (diminished roles of the Fiscal Council and the Constitutional Court)) have hurt the investment climate in recent years. This is also reflected in the World Bank's annual "Worldwide Governance Indicators" surveys, according to which Hungary has steadily deteriorated with regard to regulatory quality, rule of law and perceptions of corruption over the past decade.

In our proprietary "Environmental Sustainability Index", Hungary is ranked 92nd out of 210 economies, reflecting poor scores for renewable energy, water stress and recycling rate.Systemic political risk remains somewhat elevated since the government has engaged in unconventional economic and institutional measures over the past decade. As a result, international relations have suffered, especially with the IMF and the EU. Currently, the EU is withholding funding for Hungary under the "Recovery and Resilience Facility". This probably explains why Hungary's economy is one of a few in the EU which experienced a huge drop in investment activity in 2023. In the longer term, persistent tensions with the EU may have a damaging effect on investor confidence.