Hong Kong

Strong fundamentals safeguard the Fragrant Harbor

| GDP | USD359.8bn (World ranking 43) |

| Population | 7.3mn (World ranking 103) |

| Form of state | Special Administrative Region of the People's Republic of China |

| Head of government | John Lee Ka-chiu (Chief Executive) |

| Next elections | 2025, Legislative |

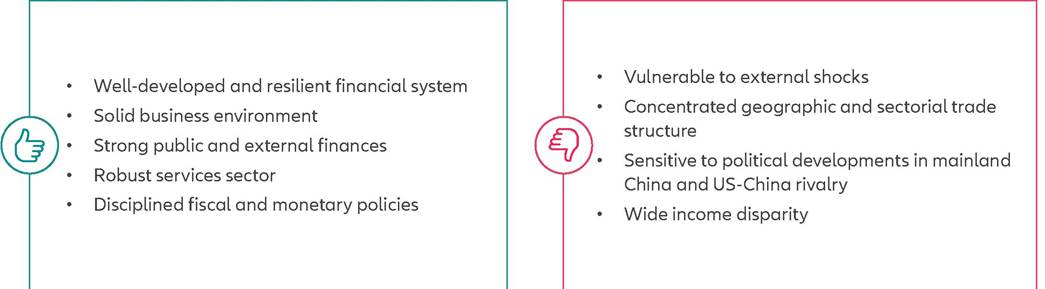

Strengths & weaknesses

Economic overview

Sailing through calmer waters, after a multitude of adverse economic shocks

Hong Kong has been a strong economic performer in the past decades, with an annual average growth of +4.2% during the 2000s and +2.9% on average in the 2010s.

But in three of the five years between 2019 and 2023, Hong Kong's real GDP has been in a contractionary phase. In addition to the 2019-2020 social unrest, the Covid-19 pandemic significantly impacted the economy. As a consequence, real GDP contracted for two consecutive years by -1.7% in 2019 and -6.5% in 2020, followed by a strong rebound in 2021 with growth accelerating to +6.4%. But the recovery was shortlived as economic growth contracted again in 2022, by -3.5% on the back of a challenging external environment, tightening in monetary conditions, rising geopolitical tensions and a significant decline in mainland China's trade activities. Going forward, we estimate the economy to have grown by +3.3% in 2023 and expect growth to settle at +2.1% in 2024 and +2.4% in 2025 on the back of a gradual recovery in external trade and higher inbound tourism (notably from China). However, private investments, inflationary pressures, rising geopolitical tensions and demographic challenges may weigh on medium term growth prospects.Fiscal policy has been broadly accommodative in the past five years, with an annual average fiscal deficit of -4.1% of GDP, with broad based stimulus measures to businesses and households including health spending, temporary employment schemes and direct support measures - lowering profit tax, waiving business registration fees and distributing consumption vouchers for instance. Going forward, we expect the fiscal deficit to narrow to -1.0% of GDP in 2024 and to return to a surplus of +0.2% of GDP in 2025 reflecting the government's commitment to fiscal discipline and increased revenues from land sales and profit taxes. Yet, the surplus will remain low in the medium term relative to the pre-pandemic average, on the back of constraints from an aging population and infrastructural projects that include the Northern Metropolis and the Lantau Tomorrow Vision.

On the monetary policy front, the Hong Kong Monetary Authority (HKMA) has limited room to maneuver as the Hong Kong dollar is pegged to the US dollar. Consequently, policy rates are primarily a function of the actions of the US Federal Reserve and until early 2024 has seen a cumulative increase of 525bps since the quantitative tightening cycle of the US Federal Reserve began in March 2022. At the same time, the high levels of liquidity in Hong Kong have reduced banks' reliance on HKMA facilities, restricting effective transmission of monetary policy. In terms of prices, the currency peg has broadly kept inflation under control and we expect a moderate overall price growth of +2.1% in 2023, +2.2% in 2024 and +2.5% in 2025.

Robust macro-fundamentals with vulnerabilities due to the trade structure

Short term financing risk in Hong Kong broadly remains low as the economy has strong fundamentals in terms of public and external balances. Indeed, fiscal support played a crucial role to mitigate the impact of the adverse economic shocks that hit the economy in the last five years.

However, we expect broad fiscal consolidation going forward. Despite remaining high relative to historical levels, public debt as a percentage of GDP remains low internationally and will remain below 10% of GDP in 2024 and 2025.In terms of external balances, Hong Kong's current account balance has recorded surpluses for more than 25 years now (including during a number of external and domestic shocks such as the Great Financial Crisis and the Covid-19 pandemic), which has resulted in the accumulation of external financial assets. On the back of a recovery of trade and earnings from overseas investments, we expect the current account balance to post a surplus of +6.3% of GDP in 2024 and +6.1% of GDP in 2025. The main structural vulnerability arises from the economy's geographical and sectorial concentration in terms of its trade structure. For instance, Hong Kong's reliance on China for exports (notably of electronic machinery and appliances) makes it vulnerable to potential cyclical swings in global demand and in China, as well as rising geopolitical tensions. Meanwhile, gross external debt remains high, at more than 500% of GDP. However, this only reflects Hong Kong's position as a global and regional financial center rather than a structural macroeconomic vulnerability.

Resilient business environment, within a stable political landscape

The business environment in Hong Kong remains strong with internationally renowned infrastructure, free port status, favorable policies in terms of trade and exchange controls and tax policies. The World Bank Institute's annual Worldwide Governance Indicators 2022 survey indicates strong scores with respect to the regulatory and legal frameworks and the control of corruption. Likewise, the Heritage Foundation's annual Index of Economic Freedom survey 2020 (the economy has been discontinued since) suggest a broad-based strength in economic freedom, notably with regard to property rights, government integrity, tax burden, government spending, fiscal health, business freedom, labor freedom, trade freedom and financial freedom.

Our proprietary Environmental Sustainability Index suggests weaknesses in environmental sustainability owing to a very low level of renewable electricity output and a moderate recycling rate. Overall, the index ranks Hong Kong 100 out of 210 economies.We do not expect significant changes to the political landscape in Hong Kong and disruptions to business and public services are unlikely in the short to medium term especially in the context of the national security law implemented in 2020. John Lee, a former police officer and security official who served as Chief Secretary for administration in 2021-22, was elected as the Chief Executive of Hong Kong following a restricted-franchise poll in May 2022 and we expect him to be selected for a second term in 2027 by the central government. While the territory will retain a high degree of autonomy under the Basic Law, a great deal of local policy steering will be influenced by mainland China's central government.

More on the topic Hong Kong:

- Shanghai vs. Hong Kong

- The Chinese and Hong Kong Experiences Compared

- Assessing the Determinants of the Hong Kong Discount

- Hong Kong

- Introduction

- References

- Would Renminbi Appreciation Really Help the US Trade Balance?

- PART ONE CHINA'S EXCHANGE RATE REGIME AND MONETARY POLIC

- 51 The Oceans in a Box

- Confronting Deflation and the Asian Financial Crisis in the Late 1990s