Shanghai vs. Hong Kong

One way to address the difficult question of whether China’s recently buoyant stock markets became “overexuberant” is to compare local investors’ own valuations of Chinese equities to those of foreign investors.

This analysis involves setting the local prices for Chinese share issues against the prices at which they trade in offshore markets like Hong Kong and New York.11 Hong Kong has consistently been the most popular choice of Chinese firms seeking an offshore listing, accounting for about two-thirds of all Chinese listings outside the mainland. This apparent preference for Hong Kong over

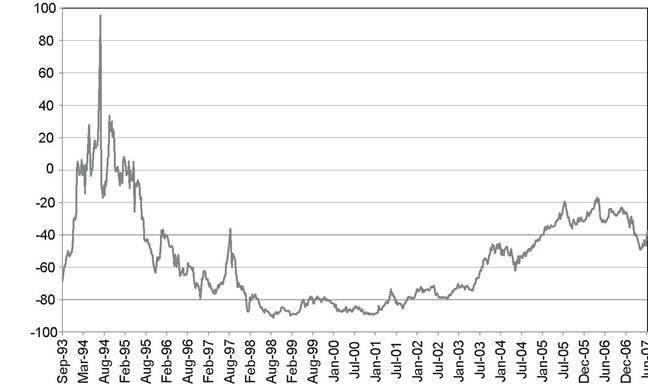

Figure 8.4. Discount Attached to Hong Kong Listings Relative to Shanghai Listings of Chinese Firms.

New York, the second most popular destination, may reflect greater access to external financing in Hong Kong. Yang and Lau (2006), for example, find that firms with New York listings were more likely to be capital-constrained than their Hong Kong counterparts. Meanwhile, Girardin and Liu (2007) identify a long-run relationship between the Shanghai “A” share index and Hong Kong’s Hang Seng stock index that appears to begin around the time of Hong Kong’s return to Chinese rule after June 30,1997.[139] Aftersomewild gyrations between 1993 and 1997 (Figure 8.4), however, a steep discount persisted in the Hong Kong price relative to the Shanghai price after 1997.

Over the 1997-2001 period, Chinese companies on average had a Hong Kong share (“H-share”) price that was 80% to 90% lower than the trading price in Shanghai, after correcting for the different currencies involved. A gradual shrinkage in the Hong Kong discount occurred during 20012006, however, with the average discount falling to as low as 17% for the week ending April 21, 2006.

This decline suggests that, relative to the more established market in Hong Kong, any overvaluation of Shanghai shares was, for the most part, greater before the rally period that began in late 2005. Whereas “A” share prices in Shanghai did accelerate faster than H-share prices after April 2006, the 38% Hong Kong discount at the end of June 2007 was still lower than any of the values observed from August 29, 1997, through January 14, 2005. Through June 2007, therefore, the Hong Kong discount remained quite low relative to its own past history.At the individual firm level, Wang and Jiang (2004, p. 1295) point to significant Commonalitybetween individual firms’ “A” shares and H-shares, concluding that the H-shares “behave more like Hong Kong stocks than mainland Chinese stocks” but “retain significant exposure to their domestic market.”[140] The general importance of the Hong Kong market to Chinese shares receives further confirmation from Kutan and Zhou’s (2006) analysis of Chinese shares traded on the New York Stock Exchange. In theory, the H-share price should be a function of the value of the underlying security in its home market of Shanghai and the exchange rate between the renminbi and the Hong Kong dollar - with arbitrage conditions implying that H- share and “A” share prices diverge solely due to exchange rate expectations and transaction costs. The relationships may be complicated by variations in market sentiment, however - a factor that seems to have played a role in the persistent discount of foreign-held “B” shares relative to locally held “A” shares that was discussed earlier.[141] Both Wei (2000) and Wang and Jiang (2004) suggest that market sentiment may be an important factor explaining the differences in the prices of cross-listed Chinese shares as well. Higher “A” share volatility relative to the firm’s corresponding H-share listing, for example, could indicate “more mood swings or noises in the Chinese market” (Wei, 2000, p.

238).There is also the issue of capital controls, with Chinese restrictions on capital outflows potentially pushing up the relative price of domestic listings insofar as domestic investors are prevented from placing funds abroad.[142] Girardin and Liu (2007, p. 368) suggest that capital controls have not precluded an “internationalization” of the strategy adopted by Chinese investors, however, and suggest that “[c]apital flight is already used by Chinese residents to buy shares in Hong Kong, including IPOs of Mainland firms listed in Hong Kong.”[143] In the empirical work following we show that both expected exchange rate changes and different market sentiment levels play a significant role in accounting for the changing size of the Hong Kong discount over time. Our empirical analysis focuses on comparisons with the Shanghai market, which accounted for approximately 80% of total mainland China stock market capitalization in 2006. We use a “panel” approach that looks at variations both across the two markets and over time - and control not only for overall market sentiment but also for company-specific measures of market sentiment.

More on the topic Shanghai vs. Hong Kong:

- CROSS-CULTURAL STUDIES

- References

- The Operations of the Asset Management Companies

- The Evolution of the People’s Republic’s Exchange Rate Policy

- Constructive controversy

- Index

- Foreign Competition, Public Listing, and WTO Entry

- Exchange Rate Expectations, Capital Flows, and Pressure for Appreciation

- Waves of Constitution-Making in Asia

- Preface