Speculative Pressures in the Equity and Real Estate Markets

Notwithstanding China’s continued modest rates of consumer price inflation going into 2007, some economists have pointed to financial imbalances

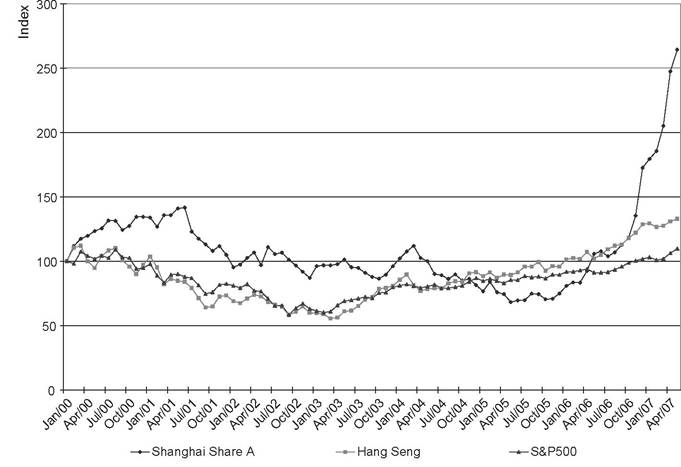

Figure 8.2.

Shanghai vs. Hong Kong and New York Share Price Movements, 2000-2007.being channeled into credit and asset price advances. In such a case, the central bank might consider acting preemptively to contain swings in asset prices and limit the risk of extreme boom-bust cycles (cf. Borio, 2005). According to Wu (2003), asset prices were an important conduit for excess money growth in China even over the pre-2001 period. Turning to the more recent 2006-2007 advance in Chinese share prices, former Federal Reserve Chairman Alan Greenspan - who famously raised the question of “irrational exuberance” in US financial markets in 1996 - issued a warning on May 23, 2007 that the gains were “unsustainable” and that a “dramatic correction” was inevitable (see Lima and Kennedy, 2007). Even more dramatic than the share price advance was the volume increase in the Shanghai market going into 2007 (shown in Figure 8.1). OnMay 9,2007, the combined trading volume in Shanghai and Shenzhen, for the first time, exceeded that of all other Asian bourses combined. An aggregate RMB 376.9 billion worth of shares changed hands that day, up from levels typically below RMB 40 billion just six months earlier (Anderlini, 2007a).

The stock market rally was accompanied by record numbers of Chinese companies issuing shares after the government lifted its temporary ban on domestic IPOs in May 2006. Substantial flows offunds into the nation’s stock markets out of individual savings accounts were seen in 2007. In Shanghai alone, over RMB 70 billion was transferred from savings accounts into stock trading accounts during the first four months of 2007 - and 421,831 new stock accounts were opened in a single day on May 8, following a weeklong holiday (China Securities Journal, 2007a).

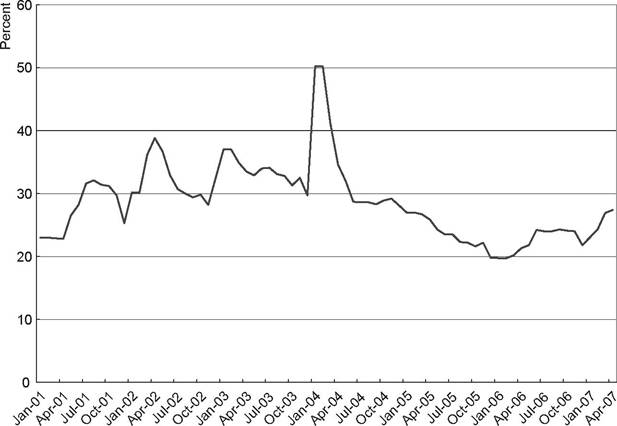

Meanwhile, national household bank deposits dropped by RMB 167.4 billion in April 2007 compared to a RMB 60.6 billion increase in April 2006 (China Securities Journal, 2007b). Fluctuations in household deposits appeared to be correlated with the ups and downs in the stock market, with a further RMB 278.4 billion decline in household deposits in May 2007 being followed by an RMB 167.8 billion increase the next month when the stock market corrected in June 2007 (People’s Daily Online, August 11, 2007c).April 2007 saw the combined market capitalization of the Shanghai and Shenzhen stock exchanges exceed the total value of savings deposits for the first time ever. One factor in the increased flow of funds into the stock market, aside from the self-fulfilling draw of the recent strong gains enjoyed there, was likely government intervention aimed at cooling off China’s strong property markets.[134] In March 2005, the regulated interest rate on home loans was raised, higher down payments were required, and the Shanghai authorities imposed a 5.5% capital gains tax on home sellers’ profits (Bradsher, 2005). There was also a special 5% tax on the total sales price for any property sold within two years of the original date of purchase. The Shanghai property market tailed off after these government measures, ending a run-up that saw average home sale prices double since 1997, including a 26% gain in 2004 alone. As shown in Figure 8.3, the flow of funds into the nation’s property markets was already turning down sharply in 2004. Given that price movements appear to have typically lagged behind innovations in property-related development by one or two years in China (Liang and Cao, 2007), it is actually not so obvious that the government initiatives were the decisive factor in the housing market downturn on this occasion.[135]

Figure 8.3. Annualized Growth Rate of Real Estate Investment in China.

Source: Great China Database.Some picking up in the rate of real estate investment was evident through 2006 and early 2007, potentially foreshadowing renewed strength in housing prices. High lending rates by Chinese banks seem to point in this direction given the historical link between bank lending rates and property prices (Liang and Cao, 2007). Nationwide year-on-year housing price increases averaged 7.1% through June 2007, led by an overall 15.9% advance in Shenzhen (Sito, 2007). Priorto the currency policy change on July 21, 2005 (Chapter 1), there were concerns that foreign investors seeking to profit both from a hot housing market and from renminbi revaluation were driving the market up excessively. This perspective receives support from the fact that hot money inflows do indeed seem to have exerted systematic, positive effects on Chinese housing prices during 1997-2005 (Zhang and Fung, 2006). In addition, even though hot money inflows appeared to diminish after the break from the fixed exchange rate policy, China’s National Bureau of Statistics continued to express concerns about the level of foreign direct investment in China’s real estate industry (“Foreign Capital Add to China’s Real Estate Bubble,” April 25, 2006).

rise to substantial defaults on loans as well as a plunging real estate market (see Zhang and Sun, 2006).

As noted earlier, China’s stock market gains through 2007, although seeming outlandish to many based upon comparisons with the much lower levels of 2005, should properly be assessed relative to the longer-run record. Indeed, not only was the market essentially flat during 2000-2006 but the lows of early 2005 matched levels seen as long ago as 1993 (see Figure 8.1)! The concern should not be the size of the share price increase itself but its source. If share price gains are an indication of excess liquidity, rather than improving fundamentals, then this would indeed suggest potentially worrisome parallels with the boom-bust cycles in Japanese and Taiwanese asset prices during the 1980s (Chapter 2). The Japanese experience of sudden tightening at the end of the 1980s, as well as the aftermath of the Chinese government’s own past heavy-handed interventions, argues against drastic action, however. Whereas the authorities did increase the stamp duty payable on stock transactions in May 2007, fears of a capital gains tax on stock gains were initially left unrealized.[136] The ongoing program of steadily placing previously nontradable shares onto the market may actually offer a more gradualist approach to soaking up some of the fervent demand for stocks. In the meantime, the authorities began a crackdown against banks whose loans had been illegally channeled into the stock market, announcing an initial series of penalties in June 2007.[137] [138]