Kenya

With bated breath until June, then onward?

| GDP | USD113.4bn (World ranking 67) |

| Population | 54.0mn (World ranking 27) |

| Form of state | Republic |

| Head of government | William Ruto (President) |

| Next elections | 2027, Presidential and legislative |

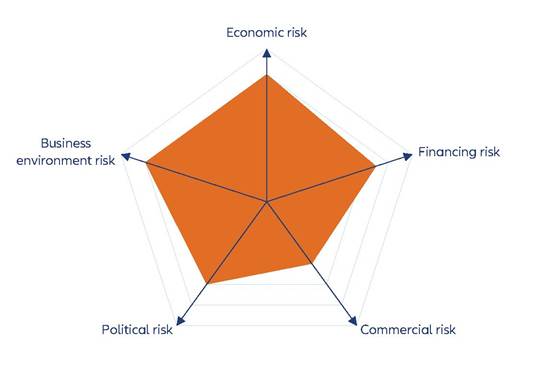

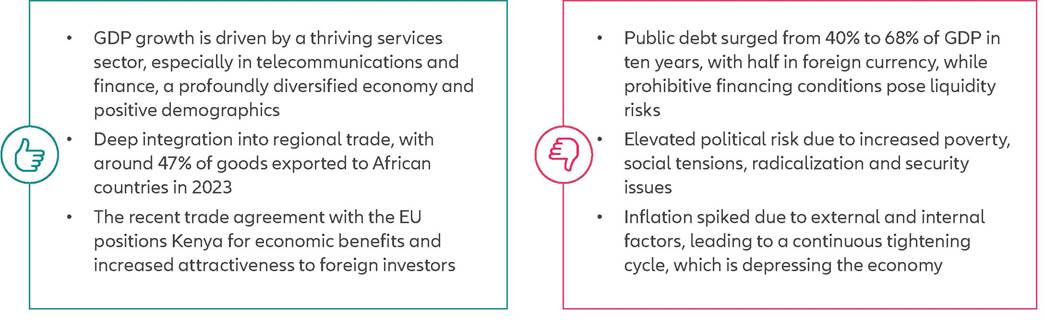

Strengths & weaknesses

Economic overview

Are structural reforms still fashionable?

Kenya has been a standout performer in Sub-Saharan Africa, achieving an average GDP growth rate of +5% over the past decade.

Factors such as a stable macroeconomic environment, sustained investor confidence and a thriving services sector, particularly in telecommunications and financial services, have fueled the country's economic potential. The new economic course Kenya has embarked on since late 2022 under President William Ruto is ambitious and may bear fruit in the medium-to long-term, although it is weighing on growth and domestic stability prospects in the short term.Kenya's real GDP is projected to grow slightly above +5% in 2024, but risks remain tilted to the downside, with 2023 closing at an expected pace of +4.4%, around 0.5% less than initially forecasted and persistent inflation (6.6% in December 2023). Kenya also benefits from manufacturing diversification and regional trade integration. In the first nine months of 2023, about 47% of exports were directed to African countries, up from 39% in 2019.

However, a less reliable client base, affected by the liquidity crisis, as well as increased costs of imported products that are essential to local manufacturers and agricultural producers, are weighing on Kenya's trade deficit, which is likely to stay at around -11% of GDP in 2024. In 2023, remittances grew at an estimated +4%, bringing in around USD4.5bn in hard currency, equivalent to 4% of projected GDP.Short-term uncertainties loom in line with prohibitive market financing conditions (yields on one-year sovereign maturities exceed 16% at the time of writing) and tight credit conditions. These factors are driving increased political confrontation and protests that could deter investment at a time when it is most needed and a substantial portion of sovereign debt in hard currency reaches maturity in the middle of the year. We anticipate that IMF and World Bank assistance will assist Kenya in navigating perilous economic challenges in 2024, notably the redemption of USD2bn in Eurobonds in June, as well as providing a medium-term framework for stronger macroeconomic stability. The next Eurobond redemptions, worth USD1.9bn, will not fall due until 2027-28, while the World Bank announced in December a massive USD12bn loan package over three years, starting in July 2024, to unleash infrastructure projects.

Beyond monetary tools: the vital role of concessional debt in economic support

Inflation accelerated in 2022-2023 due to rising global food and energy prices, but also because of regional peculiarities such as limited infrastructure, limited purchasing power and supply dependencies that add up to imported inflation. Consequently, the central bank initiated a tightening cycle in May 2022 by raising its policy interest rates for the first time since 2015 from 7% to the current 12.5%. This cycle is expected to continue well into 2024 (even though inflation is predicted to gradually moderate) to counter currency devaluation and rein in liquidity.

Kenya's fiscal and current account imbalances have exacerbated vulnerabilities to external shocks.

The country's public debt has increased from 40% of GDP to 68% in ten years, due to large infrastructure projects and poor tax collection. Moreover, almost half of Kenya's public debt is denominated in foreign currency, making it susceptible to exchange rate fluctuations. Reliance on commercial financing has increased, accounting for 30% of total public debt, as a result of improved personal income and access to commercial debt. In 2023, the International Monetary Fund (IMF) approved around USD2.4bn in new funds during successive reviews of ongoing programs. Existing facilities have been extended from 38 to 48 months, giving the country more time to execute reforms and they have been broadened to consider climate resilience measures after the country experienced the worst drought in decades.Unstable at home, on his way in diplomatic relations

Kenya's systemic political risk is elevated. This reflects political and social tensions stemming from social inequality and corruption, as well as security risks, including cross-border spillovers from the ongoing conflict in Sudan and latent tensions in Ethiopia and Somalia.

The difficulties of promoting organic reform while maintaining internal cohesion are reflected in a shifting approach to foreign relations. The current administration revised the terms and partly cancelled infrastructure projects contracted by Chinese companies with the previous government. On trade policy, Kenya signed an economic partnership agreement (EPA) with the EU in June 2023, expanding on an interim accord in effect since 2017. The EU is Kenya's top export destination and second-largest trading partner, generating EUR3.3bn of trade in 2022 - an increase of +27% compared to 2018. Once ratified, the EPA will open up new export potential for Kenya via duty-free and quota-free entry into the EU market and make the country more appealing to EU investors. The EPA will create significant economic benefits for Kenya, provide tools for dispute resolution and help in climate change mitigation. Other components, such as trade in services, competition policy and intellectual property rights, could be added to the EPA over time. On the other hand, the deal means Kenya has bypassed the fellow Eastern African Community (EAC) member states in implementing the agreement between the two sides after a previous version of the accord between the EU and the EAC stalled. Tanzania and Uganda declined to approve the agreement for various reasons, while Rwanda signed the previous EPA but did not ratify it.