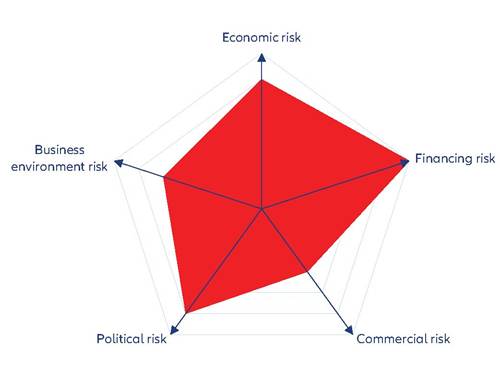

Kazakhstan

High vulnerability to global economic cycle and external shocks

| GDP | USD220.6bn (World ranking 54) |

| Population | 19.6mn (World ranking 63) |

| Form of state | Presidential Republic |

| Head of government | Kassym-Jomart Tokayev (President) |

| Next elections | 2028, Legislative |

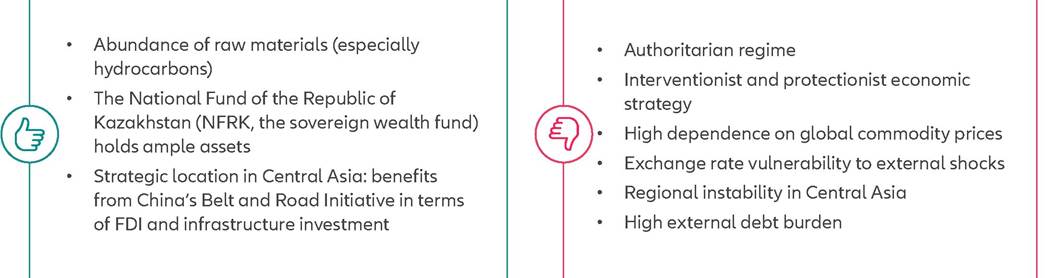

Strengths & weaknesses

Economic overview

Solid growth but persisting inflation and currency risk

A lack of economic diversification makes Kazakhstan's economy highly vulnerable to global demand for and prices of commodities, especially of oil and gas.

Economic growth has been volatile and modest over the past decade, at just +2.8% on average annually. After contracting by -2.6% in 2020, real GDP expanded by +4.1% in 2021, +3.2% in 2022 and around +5% in 2023. The external sector was the main growth driver, benefiting from surging global oil and gas prices and, in 2021, rapid growth in China (Kazakhstan's main export destination). China's revocation of its zero-Covid-19 policy in end-2022 supported Kazakh growth again in 2023. Looking ahead, we forecast average annual real GDP growth to remain above +4% in 2024-2025.Currency and inflationary risks remain on the cards. Since the massive devaluation of the Kazakh tenge (KZT) in 2014 and the subsequent shift to a floating exchange rate regime, the currency has depreciated by an average annual -14% in 20142022, though it stabilized in 2023.

The KZT is particularly vulnerable to external shocks such as the global oil price slumps in 2015-2016 and 2020 or the Covid-19 pandemic. Strong exchange-rate movements also feed through to inflation. The latter rose to an average of 15% in 2022-2023 owing to increased energy and food prices as well as supply disruptions. Inflation has only gradually come down to 9.8% at end-2023 and we forecast it to remain elevated in the next two years.Manageable public finances but weak external finances

Deteriorating business environment and high political risk

Kazakhstan's public finances have deteriorated in recent years but will remain manageable in the near term. A crisisresponse program to address the adverse effects of the Covid-19 pandemic and low commodity prices widened the annual fiscal deficit from -0.6% of GDP in 2019 to -7% in 2020 and -5% in 2021. The shortfall narrowed markedly thereafter and the official fiscal account was near balance in 2022-2023 thanks to the economic recovery and higher oil prices, but also due to some activities of numerous public entities which actually weaken fiscal accountability. For example, in 2023 the National Fund of the Republic of Kazakhstan (NFRK, the national oil fund) purchased shares of KazMunayGas, the previously 100% state-owned oil and gas company, in order to generate fiscal revenues for the government. In 2024-2025, we forecast small annual fiscal deficits. In any case, budget transfers from the NFRK have been used to finance most of the higher fiscal spending since 2020. As a result, assets held by the NFRK fell from a 2.5-year peak of USD62bn at end-2019 to a low of USD52bn in September 2022, before eventually recovering to USD60bn at end-2023. Meanwhile, total government debt rose from 20% of GDP in 2019 to 26% in 2020 but that ratio has slightly declined since then. In any case, this is still low compared to peer countries.

Kazakhstan's external finances are a cause for concern. Following eight years of annual deficits in 2014-2021 (on average -3.3% of GDP), the current account moved to a surplus of +3.1% of GDP in 2022 on the back of the high oil and gas prices, but reverted to an estimated deficit of around -3% in 2023, owing to the decline in oil prices.

We forecast continued annual deficits to the tune of -2.5% to -4% of GDP in 2024-2025. Meanwhile, Kazakhstan's external debt-to- GDP ratio has declined from an average 85% of GDP over the past decade but is forecast to remain above 60% in the next few years, which will still be a comparatively high ratio while external debt servicing will remain hefty at around 35% of export earnings.The central bank's official foreign exchange (FX) reserves are another cause for concern, since they have heavily fluctuated between USD9bn and USD17bn over the past five years, with the high volatility causing uncertainty. Towards the end of 2023, reserves strengthened somewhat to USD16bn which, however, is only sufficient to cover around 38% of the estimated external debt payments due in 2024 (estimated at USD42bn), well below an adequate ratio of 100%. In other terms, FX reserves cover only three months of imports, well below a comfortable level of four months. The assets of the NFRK provide some cushion with respect to the low level of official FX reserves. However, the Kazakh authorities have indicated over the past decade that they are not willing to use those assets for purposes they are not meant for, such as for example bailing out faltering banks.

The business environment in Kazakhstan has weakened in recent years and is now slightly below average in our assessment of 185 economies. The Heritage Foundation's 2023 Index of Economic Freedom survey assigns Kazakhstan rank 71 out of more than 180 countries, down from rank 34 two years earlier. The significant worsening reflects deteriorated property rights, judicial effectiveness, business freedom and labor freedom while government integrity has remained weak. Moreover, the World Bank Institute's annual Worldwide Governance Indicators surveys continue to indicate considerable weaknesses with regard to regulatory quality and, in particular, the rule of law and control of corruption. Our proprietary Environmental Sustainability Index ranks Kazakhstan only 140th out of 210 economies, reflecting serious weaknesses regarding renewable electricity output and the recycling rate.

Systemic political risk in Kazakhstan is high. The political regime is considered an autocracy with weak institutional effectiveness. In response to violent social unrest in January 2022, President Tokayev began reforms that aim at curbing presidential powers and delegating more powers to parliament, as well as making the registration of political parties easier in an attempt to improve pluralism. The reforms have the potential to significantly improve the political environment in Kazakhstan. However, progress on the reforms is likely to be slow, not least because of potential opposition from political elites. Moreover, mismanagement or slow advancement of the reforms could spark renewed social unrest, in particular if the economic situation worsens. Overall, the risks to political stability will remain high in Kazakhstan over the medium term.

More on the topic Kazakhstan:

- The ratio of the economy, politics and law.

- Conclusion

- HYPERTHERMIA

- The place and role of knowledge of life safety basics in the modern world

- The ramifications of the Union of Lublin and the absorption of Ukrainian lands into Poland were not only political in nature;

- Today over 2.5 million people of Ukrainian descent live outside the borders of the Soviet Union.

- Miscellaneous

- Key Takeaway

- Allianz Research. Country Risk Atlas 2024: Assessing non-payment risk in major economies. Allianz,2024. — 179 p., 2024

- Sovereign bond risk and return