Japan

Slow return to normal

border=0>

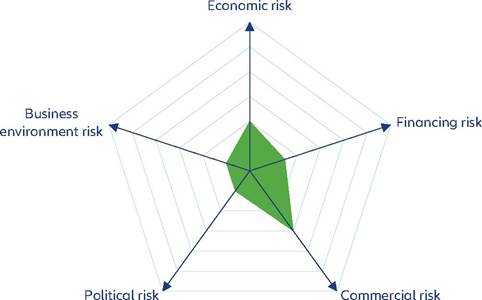

Strengths & weaknesses

Economic overview

Real GDP just back to prepandemic levels

The Japanese economy has been a slow performer among peers, with GDP growing by +0.8% on average over 20002019 and by +1.2% over 2010-2019.

This compares with average growth of +1.9% and +2.0% for all advanced economies, respectively and average growth in Asia-Pacific of +4.5% and +5.0%, respectively. In 2020, the economy entered the Covid-19 crisis on a soft footing, being on the verge of a technical recession at the end of 2019. Real GDP contracted by -4.3% in 2020, after shrinking by -0.4% in 2019. The recovery in 2021 was mild, with growth of just +2.3%, followed by a modest +0.9% in 2022, even though Covid-19 constraints ended in that year. In 2023, growth picked up to an estimated +1.8%, bringing real GDP back to its 2019 level. Private consumption has been the driver of the modest rebound in the last two years, compensating for the decline in net exports due to worsening global demand. We predict annual real GDP growth to moderate to approximately +1.0% in 2024-2025, still supported by domestic spending and investment, but tamed by higher input costs and weak trade. Over the longer term, Japan should return to its prepandemic, structurally low growth rate of slightly over +1% per year until 2028. On the one hand, the medium-term economic performance will be supported by more dynamic global and domestic demand, higher public investment as well as a competitive environment. On the other hand, labor shortages caused by the aging of the population will curtail Japan's growth prospects.Inflationary pressures are scarce in Japan. Headline consumer price inflation averaged +0.5% over 2010-2019, including three deflationary years. Inflation accelerated to an average +2.5% in 2022 but remained well below the global rate of +8.7%. In 2023, inflation came in at around +3% - a 30-year high in Japan - while global inflation decreased to an estimated +7%. Against this backdrop, the Bank of Japan, (BoJ, the central bank) has maintained its ultra- accommodative, negative policy interest rates stance - in contrast to almost all other major central banks in the world that have tightened their monetary policies over the past two years. Such a divergence is putting pressure on the currency, with the JPY depreciating against the USD (JPY132:USD1 in Q1 2023, JPY149:USD1 in Q4 2023). Alongside high global energy and food prices, the weakness of the JPY will cause higher imported inflation. Further depreciation is likely until the second half of 2024, when the US is expected to begin with monetary easing. In the coming years and as long as the economic recovery and inflationary trends are not sustainable, the BoJ is likely to keep a negative policy rate and continue purchasing assets and controlling the yield curve. If inflation proves persistent and if wages increase, the BoJ could eventually seize the opportunity to raise its policy rate into positive territory, reversing the deflationary mindset. Fiscal policy had been eased significantly during the height of the Covid-19 crisis and we expect the government to continue to support household income and encourage rising wages and workforce training in the next few years. On the corporate side, the government will keep incentivizing efforts towards digitalization and innovation (especially when it comes to semiconductors and the green transition).

Structural vulnerabilities: public finances, demographics, climate

Overall, indicators show that Japan's short-term financing risk is low. The indicators that need monitoring in the short run are mostly related to public finances, with very large levels of fiscal deficit and public debt. The latter already stood at 236% of GDP in 2019 and rose to 260% in 2022. It is expected to moderate a little to just over 250% by 2025, benefiting from somewhat higher nominal GDP growth, which mechanically drags down the ratio. The annual fiscal deficit is only slowly declining: -9.1% of GDP in 2020, between -7.0% and -6.0% in 2021-2023 and forecast at around -4.5% in 2024 and -3% in 2025. However, debt-servicing costs remain manageable, given low interest rates. Currency risks are also limited as most of the debt is denominated in JPY and domestically- owned.

In the long run, the Japanese economy's vulnerabilities mostly stem from a declining, aging population - with gains in productivity not enough to compensate and a strong resistance to immigration. The working-age population (between age 15 and 64) has been declining in Japan since 1996 and the old age dependency ratio reached 51.2% in 2022, meaning that there is not even two working-age

Japanese people per person over the age of 64. The fertility rate in Japan declined to 1.26 in 2022. Climate change is another long-term risk for Japan, which, as an archipelago, is vulnerable to rising sea levels and more intense weather events.

Business environment and political developments

Japan's business environment is well-positioned in our assessment of 185 economies, rated in the best range in the majority of the subcomponents, although it seems to be slightly deteriorating. The 2023 Heritage Foundation's Index of Economic Freedom survey assigns Japan rank 31 out of around 180 economies, reflecting particularly good scores with regards to property rights, judicial effectiveness, government integrity, business freedom and trade freedom, while there remains room for improvement regarding public finances and investment freedom.

Meanwhile, the World Bank Institute's annual Worldwide Governance Indicators surveys suggest that the regulatory and legal frameworks are business-friendly and the level of corruption is low. Our proprietary Environmental Sustainability Index puts Japan at rank 78 out of 210 economies, reflecting strengths in energy use per GDP, water stress and CO2 emissions per GDP, but weaknesses in terms of the recycling rate and renewable electricity output.Japan's political stability rests on the dominance of the Liberal Democratic Party (LDP) under Prime Minister Kishida Fumio. Internal LDP dynamics, including factional debates and cooperation with the junior coalition partner, Komeito, shape policy more than opposition scrutiny. Despite economic challenges and a by-election setback, the LDP maintains broad appeal, securing Kishida's position amid a lack of credible contenders. In September 2023, a cabinet reshuffle reinforced Kishida's leadership, aligning with influential conservative factions. The weakened liberal and left-wing opposition, marked by successive defeats and a lack of reform ideas, struggles to challenge the LDP. While the conservative Ishin party gains support, it shares policy proposals, limiting its ability to challenge the LDP's national rule. In the House of Representatives, the LDP-Komeito coalition holds a robust majority, streamlining legislative processes. Kishida is anticipated to call an early 2024 lower- house election, seeking public approval for tax increases and is likely to obtain it. A victory would pave the way to political stability in the medium term.