Role of Internal Audit in Crisis

According to the definition of The Institute OfInternal Auditors-IIA, “Internal audit is an independent and objective assurance and consultancy activity aimed at improving an organization’s activities and adding value to them.

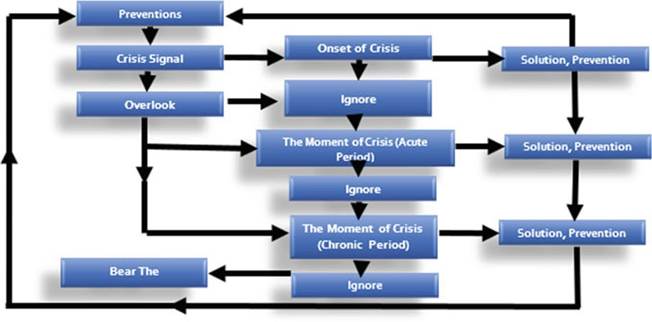

Internal audit helps the organization achieve its goals by bringing a systematic and disciplined approach to evaluate and improve the effectiveness of the risk management, control and governance (corporate governance) processes of the organization”. As can be understood from this definition, internal audit will add value to the organisation’s activities by measuring the effectiveness of the risk management, internal control and corporate management processes of the organisation. Crisis management is also included in the scope of internal control as a measure that organisations will take in case of extraordinary situations, and it is natural for internal auditors to add value to this process. In addition, the organisation will need an assessment of the design and implementation effectiveness of the planned controls while achieving its crisis management objectives, which can be presented by the internal audit activity.Examining the cyclical flow chart of the crisis in Fig. 4.4, the controls named as preventive measures or solutions to be taken during the crisis process can be operated, as designed, at every phase of the process and if the desired effect is provided, the results of the crisis can be converted to benefit. The internal audit activity plays a role as a strategic mind partner for the organisation, developing and ensuring taking precautionary measures in advance, with a process- and mistake- oriented approach that suggests doing things right as well as doing the right things. When this phenomenon is considered together with the questioning of the possibility of turning the crisis into an opportunity, the internal audit activity will also contribute to the management board and senior management in the management of the crisis process.

Fig. 4.4 Cyclic flow chart of the crisis. Source Kash and Darling (1998:181)

In order to reveal the contribution of the internal audit activity, it is necessary to explain what the organisation needs to do in the phases of crisis defined in Fig. 4.1 and the duties of the internal auditors in accordance with the scope.

4.5