Russia

Gloomy medium-term economic outlook

| GDP | USD2240.4bn (World ranking 8) |

| Population | 143.6mn (World ranking 9) |

| Form of state | Presidential Republic |

| Head of government | Vladimir Putin (President) |

| Next elections | 2024, Presidential |

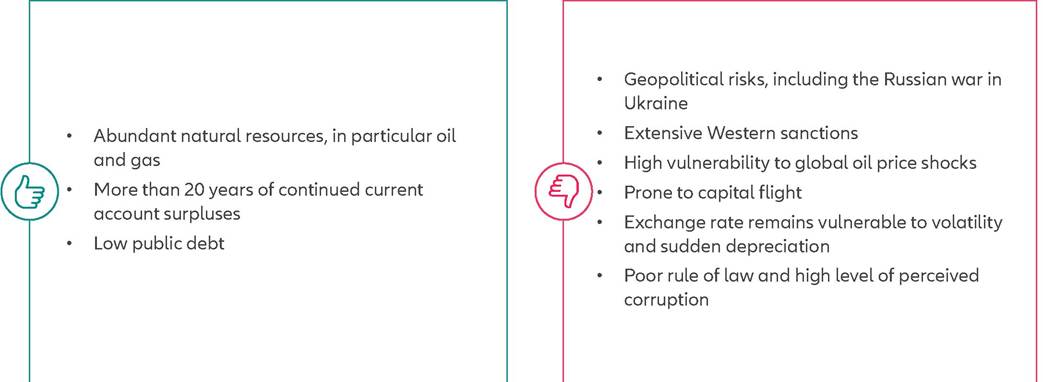

Strengths & weaknesses

Economic overview

Unprecedented sanctions have resulted in much deteriorated political, economic and business environments

Following the Russian military invasion of Ukraine on 24 February 2022, governments around the world imposed sweeping and sizable financial and economic sanctions on the Russian economy and individuals, including partial export embargoes on hi-tech goods exports, sanctions against the largest Russian banks, the removal of multiple Russian banks from the SWIFT messaging system and the freezing of around one half of the Central Bank of Russia's (CBR's) foreign exchange (FX) reserves held in G-7 and other Western countries.

Meanwhile, many countries have also imposed an oil-import embargo. Counter-sanctions from Russia have included FX controls for business transactions, stringent capital controls regarding payments abroad (including sovereign debt service and banning foreigners from selling securities), the nationalization of foreign companies deciding to exit Russia after the start of the war as well as selected export embargoes to the West (especially on most natural gas exports to the EU). The capital controls also led to a selected default of the Russian government on its sovereign debt in mid-2022. As long as the Russian war against Ukraine continues, further escalation cannot be excluded, which could result in even harsher sanctions and counter-sanctions. The overall environment for doing business in and with Russia is now very unfavorable.Modest growth and elevated inflation in 2024-2025

The Russian economy entered a recession in 2022 but held up much better than initially expected despite wide-ranging sanctions. Real GDP contracted by -2.1%, driven by a drop in inventories, a negative contribution of net trade and a decrease in consumer spending. In 2023 the economy rebounded strongly on the back of substantial fiscal stimulus that supported domestic demand. Real GDP expanded by +2.9% y/y in the first three quarters and is estimated at over +3% in 2023 as a whole. Russia was also able to divert a large part of its exports. While Western sanctions were stepped up - including the EU's embargo and the G-7 countries' price cap (at 60 USD/bbl) on seaborne Russian crude oil imports from December 2022 and the EU ban on Russian oil products from February 2023 - China, India and Turkiye have become the main buyers of Russian oil and some of their imports have been "re-blended" and sold on to countries with sanctions in place. Looking ahead, economic activity is projected to cool in the next two years owing to slowing domestic demand due to higher inflation and interest rates and difficulties in replacing lost European markets for gas exports. Overall, we forecast average annual GDP growth of around +1.5% in 2024-2025.

Consumer price inflation has steadily increased from the low of 2.3% in April 2023 to 7.4% at the end of the year as import suppression, labor shortages, supply-chain disruptions and a weaker currency in 2023 exerted upward pressure on prices. Lower oil and gas prices in 2023 have markedly weakened demand for the Russian ruble (RUB), which has lost -30% in value against the USD since end-November 2022 - when the West's oil embargo and price caps came into force.

We expect headline inflation to remain elevated for some time and to begin moderating in the second half of this year. We forecast it at an average of around 6.5% in 2024 and 4.5% in 2025. In response to the weakening RUB and the building inflationary pressures, the CBR hiked its key policy interest rate from 7.50% to 16.00% in H2 2023. We expect monetary policy to remain tight until substantial disinflation takes hold.Fiscal and external positions are deteriorating but remain sustainable, for now

Russia's fiscal deficit widened in 2023, mainly due to rising defense spending and social expenditures as well as declining energy export revenues. Looking ahead, military spending is expected to surge to around 6% of GDP in 2024, making up about one third of the total budget. However, revenues are also expected to rise, in part thanks to special taxes on energy companies. Overall, we forecast an annual fiscal deficit of around -2% of GDP in 2024. Russia will finance the shortfall through domestic bond (OFZ) issuance and withdrawals from the National Wealth Fund (NWF, a sovereign wealth fund). That said, it should be noted that a substantial drawdown of the NWF, as well as potential expenditure cuts in the next years, would have crucial medium and long-term effects for the economy and the welfare of the Russian people.

Russia's foreign exchange (FX) reserves have recovered since September 2022 and we expect the Russian economy from this perspective to be able to cope with Western sanctions in 2024. FX reserves (excluding gold) fell from USD498bn in January 2022 to a temporary low of USD417bn (including frozen FX reserves) in September 2022, about half of which was due to the USD's strength weighing on the valuation of assets in other currencies. Since then, they have recovered somewhat and stood at to USD443bn at end-2023. A reversal of the valuation effect played a role in the recovery, but the record-high current account surplus of USD238bn (+10.5% of GDP) in 2022 and the de-dollarization of external trade have likely been more important.

The Chinese renminbi is gaining increasing popularity in Russia's external trade so that forthcoming export earnings cannot be frozen by Western sanctions anymore. Under the assumption that frozen FX reserves have remained roughly stable at USD238bn (half of total FX reserves in February 2022) since the war began, available FX reserves are currently estimated at just over USD200bn. This level is sufficient to cover a healthy six months of imports. Meanwhile, the current account surplus shrank markedly to USD53bn in 2023 (around +2.7% of GDP), mainly due to lower energy export revenues and we forecast it to remain close to that level in 2024. Yet such a surplus should help to escape a sharp decline in available FX reserves over the next year. In a more conservative but less likely scenario where available FX reserves fall to USD160bn at some point in 2024, import cover would still be five months. And in a worse scenario, Russia would still have the possibility to monetize part of its gold reserves, which stood at around USD156bn at end-2023.