Slovakia

Defying the global headwinds

| GDP | USD115.5bn (World ranking 62) |

| Population | 5.4mn (World ranking 119) |

| Form of state | Parliamentary Republic |

| Head of government | Robert Fico (PM) |

| Next elections | 2024, Presidential |

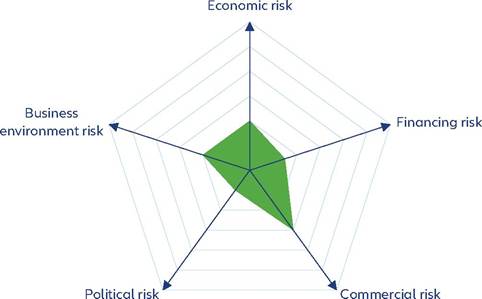

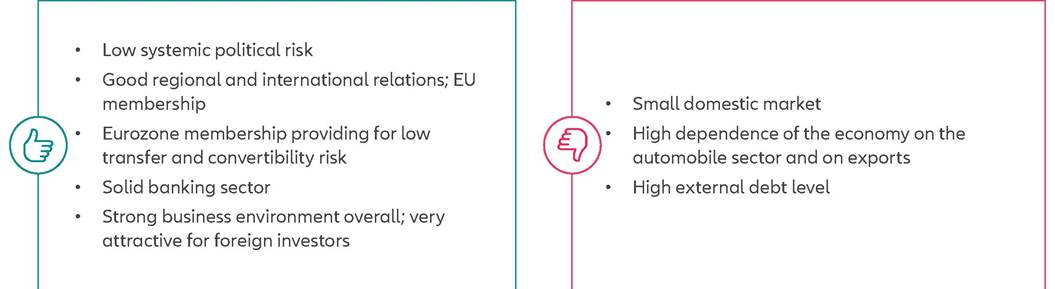

Strengths & weaknesses

Economic overview

Modest growth and elevated inflation

Slovakia has been a strong performer compared to both Eurozone and emerging economies, with real GDP expanding by an average +3.3% over the past 20 years.

However, a high dependence on exports (amounting to almost 100% of GDP) causes above average cyclical fluctuations in growth. Moreover, a high dependence on global supply chains and energy imports make the Slovak economy vulnerable to external shocks. Therefore, the economy was hit hard by the global Covid-19 crisis (-3.3% decline in 2020), despite sizeable economic policy support. And after a strong recovery in 2021 (+4.8% growth), growth slowed down markedly in 2022 (+1.8%) because of the consequences of the war in Ukraine, notably the subsequent EU sanctions on Russia and soaring energy prices. Growth in 2023 is expected to have slowed further to around +1% on the back of contracting consumer and public spending and a drop in inventories. However, a recession was avoided thanks to a solid rise in fixed investment and a positive contribution to growth by net trade. The latter was a result of a much stronger decline in imports than in exports.Looking ahead, we expect a gradual acceleration of real GDP growth to approximately +1.5% in 2024 and +2.5% in 2025, supported by the recovery of consumption from the energy price shock and continued investment growth driven by EU structural funds, the Recovery and Resilience Facility and government investment. External demand for Slovakia's main export products is expected to strengthen over the next two years, but the increase in Slovak imports is set to be as strong so that the contribution of net exports to growth will be more balanced.

Inflation will continue to moderate but remain elevated in 2024-2025. Consumer price inflation had begun to rise in the first half of 2021 and hit a peak of 15.4% y/y in February 2023, driven by interrupted supply chains and surging energy and food costs. Since then it has eased to 5.9% in December, in part due to base effects, the ECB's tighter monetary policy and slowing domestic demand. Going forward, inflationary pressures will remain elevated. Energy inflation is set to rise as government measures regarding gas prices for households are expected to be phased out in 2024. Moreover, the tight labor market provides conditions for strong wage and price growth in the services sector. We forecast annual average headline inflation at around 5% and 3% in 2024 and 2025, respectively. Meanwhile, Eurozone membership provides for low transfer and convertibility risk and has substantially decreased external vulnerabilities related to exchange rate risk in Slovakia.

Worsened but manageable public and external finances

Slovakia's public finances have deteriorated in recent years but should remain manageable over the two-year forecast horizon. The Covid-19 crisis reversed seven years of fiscal consolidation. The annual fiscal deficit had been below -3% of GDP since 2013 (on average -1.9%). As a result, total public debt fell from 55% of GDP in 2013 to 48% in 2019.

Then, fiscal stimulus measures combined with declining nominal GDP in the wake of the Covid-19 crisis resulted in large fiscal shortfalls of more than -5% of GDP in 2020 and 2021. Following an improvement to -2% in 2022, the deficit has widened again to around -5.5% in 2023 owing to increased expenditure to counter social pressures as well as the impact of high energy prices. Although energy-related measures are expected to be phased out in 2024, the annual fiscal deficit is forecast to remain above -5% of GDP in 2024-2025, mainly owing to a new range of social expenditure measures and an increase in defense spending. Nonetheless, financing the deficits should be manageable even though yields on Eurobonds have increased. The government is also eligible for substantial EU funding. As a result of several years of elevated fiscal deficits, total public debt has risen and should remain at close to 60% of GDP in 2024-2025. However, this is still a favorable ratio compared to most other Eurozone member countries, especially in Western Europe.Slovakia's external position has largely rebalanced after it rapidly deteriorated in 2022. Following a decade of moderate current account surpluses or deficits (on average -1% of GDP in 2012-2021), a large external shortfall of around -8% of GDP was posted in 2022, a result of surging energy import prices. Moreover, only one fourth of the shortfall was covered by net foreign direct investment inflows, which have a longer-term nature, in contrast to 61% of the cumulative deficit in 20152019. As energy prices have moderated from the very high levels in 2022 and imports contracted in 2023 due to weak domestic consumption, the current account deficit narrowed markedly to an estimated -2.4% of GDP last year. As imports are expected to recover going forward, we forecast the annual external shortfall to widen moderately to around -3% of GDP in 2024-2025. Overall, thanks to Slovakia's Eurozone membership, external liquidity risk should remain limited.

Strong business environment and low political risk

The Slovak business environment is well above average.

The World Bank Institute's annual Worldwide Governance Indicators surveys suggest that the regulatory and legal frameworks are business-friendly though a certain level of corruption is still perceived as present. The Heritage Foundation's Index of Economic Freedom survey 2023 assigns Slovakia rank 33 out of more than 180 economies, reflecting strong scores regarding property rights, judicial effectiveness, tax burden, trade freedom and investment freedom. However, weaknesses remain in the areas of government integrity and labor freedom. Meanwhile, our proprietary Environmental Sustainability Index puts Slovakia at rank 53 out of 210 economies, reflecting strengths in energy use and CO2 emissions per GDP, water stress and general vulnerability to climate change, though there are still weaknesses in renewable electricity output and the recycling rate.

Overall systemic political risk is low. Slovakia is a stable democracy and has good international relations, reflected in its EU, NATO and OECD membership. Government stability has suffered since 2016 and could, if continued, result in ineffective policymaking and slow reform progress. Yet, broad policy continuation has been the rule after past government changes.