Singapore

Resilient growth in a roaring business environment

| GDP | USD466.8bn (World ranking 34) |

| Population | 5.6mn (World ranking 114) |

| Form of state | Parliamentary Republic |

| Head of government | Lee Hsien Loong (PM) |

| Next elections | 2025, Legislative |

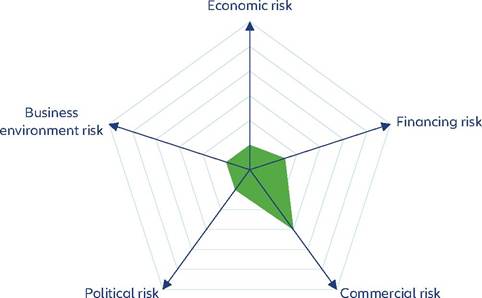

Strengths & weaknesses

Economic overview

Sustained economic resilience underpinned by disciplined fiscal and monetary policy

Singapore has a remarkable track record of economic growth, with an annual average rate of +5.4% in the 2000s and +5% in the 2010s.

The economy was severely hit by the Covid-19 crisis with growth contracting by -3.9% in 2020, followed by a strong rebound of +8.9% in 2021 and moderating to +3.7% in 2022, driven by a rebound in external demand and higher corporate and household confidence. However, the post-pandemic recovery seems to have come to an end, as we estimate growth to have slowed down to +0.9% in 2023 due to softening external demand amid high inflation and a downturn in the electronics cycle. Going forward, we forecast growth to settle at +2.2% in 2024 and +2.3% in 2025, driven by a recovery in private consumption and investments. In the medium term, risks to economic growth are tilted to the downside, which include risks such as a global economic slowdown, supply chain disruptions and rising geopolitical tensions. In the longer term, risks from climate change may weigh on the economic prospects of the economy.Fiscal policy in Singapore has been supportive during the Covid-19 crisis, with measures such as cash payouts, wage subsidies and targeted financial support which pushed the fiscal balance into a deficit of -6.8% of GDP in 2020 - a significant deviation from the pre-pandemic surplus of +5% of GDP. The economic recovery and the rollback of broadbased supportive measures have brought back the fiscal balance into positive territory since, with the fiscal balance posting a surplus of +1.2% of GDP in 2021, +0.8% in 2022 and +3.2% in 2023. Looking ahead, we expect it to moderate at +2.8% in 2024 and +3.4% in 2025, while targeted policy measures will continue to be rolled out, especially to ease the impact of higher prices. Medium and long-term challenges such as an aging population, risks from climate change and the need to maintain its competitiveness among rising competition from its regional peers will constrain the surplus from increasing further.

In terms of prices, headline inflation remained elevated in 2022 and 2023 at +6.1% and +5% respectively, relative to a pre-pandemic average of +1.7% across 2010-2019, on the back of the GST rate hike and a tight labor market. The Monetary Authority of Singapore (MAS) has tightened monetary policy five consecutive times between October 2021 and 2022 and have maintained a neutral stance since, to tame inflation. Its policy stance has been helpful in dampening inflation, with inflation expectations remaining well-anchored. We expect them to continue to maintain a neutral stance in the short term before pivoting, staying cautious particularly on the back of upward risks to inflationary pressures. Looking ahead, we expect inflation to moderate to +2.9% in 2024 and +2.5% in 2025 with upside risks mainly arising from higher agricultural prices from a severe El Nino weather event and higher oil prices if the Israel-Hamas conflict escalates.

Rock-solid macro fundamentals outshine structural vulnerabilities

Short term financing risk in Singapore remains low on the back of strong macro-fundamentals - both in terms of public and external finances.

It remains one of the few countries with the top credit rating of AAA from leading credit agencies. We forecast public debt to remain elevated in 2024 and 2025 at 165% and 168% of GDP respectively. However, it should not be a cause for concern, as it is entirely domestic and is issued to meet specific long-term objectives, in addition to the economy being a net external creditor.On the back of favorable trade policies and infrastructure, Singapore continues to solidify its strength as a globally renowned entrepot. In terms of external balances, the economy has run a current account surplus for decades, with an annual average of +18% of GDP during the 2010s and as a consequence, has accumulated ample foreign exchange reserves. The solid current account balance reflects a surplus in trade in goods and services, partly offset by a deficit in the income account, on the back of repatriation of profits by foreign firms and interest payments on external debt. We estimate the current account balance to post a surplus of +16.6% of GDP in 2023 and going forward, we forecast it to moderate a little to +15.2% in 2024 and +14.6% in 2025, as private consumption and capital-related imports recover. Vulnerabilities mainly arise from the economy's dependence on its external sector, making it exposed to challenges that are sometimes beyond Singapore's control.

Corporate-friendly business framework, with low risks to political stability

Singapore offers a prime business environment for corporations thanks to its liberal landscape in terms of trade and investments, transparent political system, favorable tax policies, solid infrastructure and a strong workforce. The World Bank Institute's annual Worldwide Governance indicators suggest that the regulatory and legal frameworks are business-friendly and the level of corruption is low. On broadly similar lines, the Heritage Foundation's annual Index of Economic Freedom Survey 2022 ranks Singapore first out of 185 countries, reflecting strengths in areas such as property rights, government integrity, tax burden, government spending, business freedom, trade freedom, financial freedom and investment freedom.

However, Singapore scores less favorably with regard to environmental sustainability, owing to a very low level of renewable electricity output and a high level of water stress. Overall, Singapore ranks 79 out of 202 economies based on our proprietary Environmental Sustainability Index.The political landscape in Singapore remains stable, transparent and efficient. By addressing medium and long-term challenges such as social inequality, immigration, job-skill mismatches and the perception of an inadequate social safety net, the ruling People's Action Party (PAP) led by Lee Hsien Loong, will aim to further boost its popularity after a mild erosion to its dominance following the election in 2020, when the Worker's Party (WP) - the main opposition - increased its vote share. Vulnerabilities to the political landscape arise from Singapore's ethnic diversity, but escalated racial tensions are not likely due to constraints on press freedom and public demonstrations.

More on the topic Singapore:

- Conclusion

- Founding Moments for the Republic of Singapore: Tension between the de Jure v de Facto Status of the Constitution

- Introduction: Repurposing an Extant Constitution

- The Process of Repurposing a Constitution

- The Substance of Constitution-Making

- Making the Constitution Work: More Re-Making

- Limits of Unconscionability and No-Injunction Clauses

- From Correlates to Fundamental Causes

- Economic Growth and Income Differences

- Introduction