Complementarity in innovation

In the models described so far, innovation has no effect on the profitability of existing intermediate firms. This is a knife-edge property which descends from the specification of the final production technology, (3).

In general, however, new technologies can substitute or complement existing technologies.Innovation often causes technological obsolescence of previous technologies. Substitution is emphasized, in an extreme fashion, by Schumpeterian models such as Aghion and Howitt (1992). In such models, innovation provides “better of the same”, i.e., more efficient versions of the pre-existing inputs. Growth is led by a process of creative destruction, whereby innovations do not only generate but also destroy rents over time. This has interesting implications for dynamics: the expectation of future innovations discourages current innovation, since today’s innovators expect a short life of their rents due to rapid obsolescence. More generally, substitution causes a decline in the value of intermediate firms over time, at a speed depending on the rate of innovation in the economy.

There are instances, however, where new technologies complement rather than substitute old technologies. The market for a particular technology is often small at the moment of its first introduction. This limits the cash-flow of innovating firms, which initially pose little threat to more established technologies. However, the development of new compatible applications expands the market for successful new technologies over time, thereby increasing the profits earned by their producers. Rosenberg (1976) discusses a number of historical examples, where such complementarities were important. A classical example is the steam engine. This had been invented in the early part of the XVIIIth Century, but its diffusion remained very sporadic before a number of complementary innovations (e.g., Watt’s separate condenser) made it competitive with the waterwheels, which remained widespread until late in the XIXth Century.

Complementarity in innovation raises interesting issues concerning the enforcement and design of intellectual property rights. For instance, what division of the surplus between basic and secondary innovation maximizes social welfare? This issue is addressed by Scotchmer and Green (1995) who construct a model where innovations are sequentially introduced, and the profits of major innovators can be undermined by subsequent derivative innovations. In this case, the threat of derivative innovations can reduce the incentive for firms to invest in major improvements in the first place. However, too strong a defense of the property right of basic innovators may reduce the incentive to invest in socially valuable derivative innovations. Scotchmer and Green (1995) show that the optimal policy in fact consists of a combination of finite breadth and length of patents. Scotchmer (1996) instead argues that it may be optimal to deny patentability to derivative innovations, instead allowing derivative innovations to be developed under licensing agreements with the owner of the basic technology. More recently, Bessen and Maskin (2002) show that when there is sufficient complementarity between innovations (as in the case of the software industry), weak patent laws may be conducive to more innovation than strong patent laws. The reason is that while the incumbent’s current profit is increased by strong patent laws, its prospect of developing future profitable innovation is reduced when patent laws inhibit complementary innovations.

While this literature focuses on the partial equilibrium analysis of single industries, complementarity in innovation also has implications on broader development questions. Multiple equilibria originating from coordination failures [of the type emphasized, in different contexts, by Murphy, Shleifer and Vishny (1989), and Cooper and John (1988)] can arise when there is complementarity in innovation. Countries can get locked-in into an equilibrium with no technology adoption, and temporary big-push policies targeting incentives to adopt new technologies may turn out to be useful.[57] One such example is Ciccone and Matsuyama (1996).

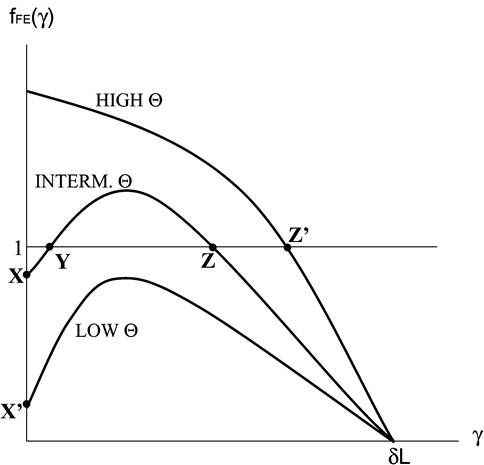

In their model, multiple equilibria and poverty traps may arise from the two-way causality between the market size of each intermediate good and their variety: when the availability of intermediates is limited, final good producers are forced to use a labor intensive technology which, in turn, reduces the incentive to introduce new intermediates.Young (1993) constructs a model where innovation expands the variety of both intermediate and final goods. New intermediate inputs are not used by mature final industries, and their market is initially thin. The expansion of the market for technologies over time creates complementarity in innovation. The details of this model are discussed in the remainder of this section. To this aim, we augment the benchmark model of Section 2 with the endogenous expansion in the variety of final goods.[58] Over time, innovative investments make new intermediate inputs available to final producers, as in Romer’s model. However, as a by-product (spillover), they also generate an equivalent expansion of the set of final goods that can be produced. There are no property rights defined on the production of new final goods, and these are produced by competitive firms extraneous to the innovation process.

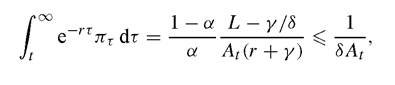

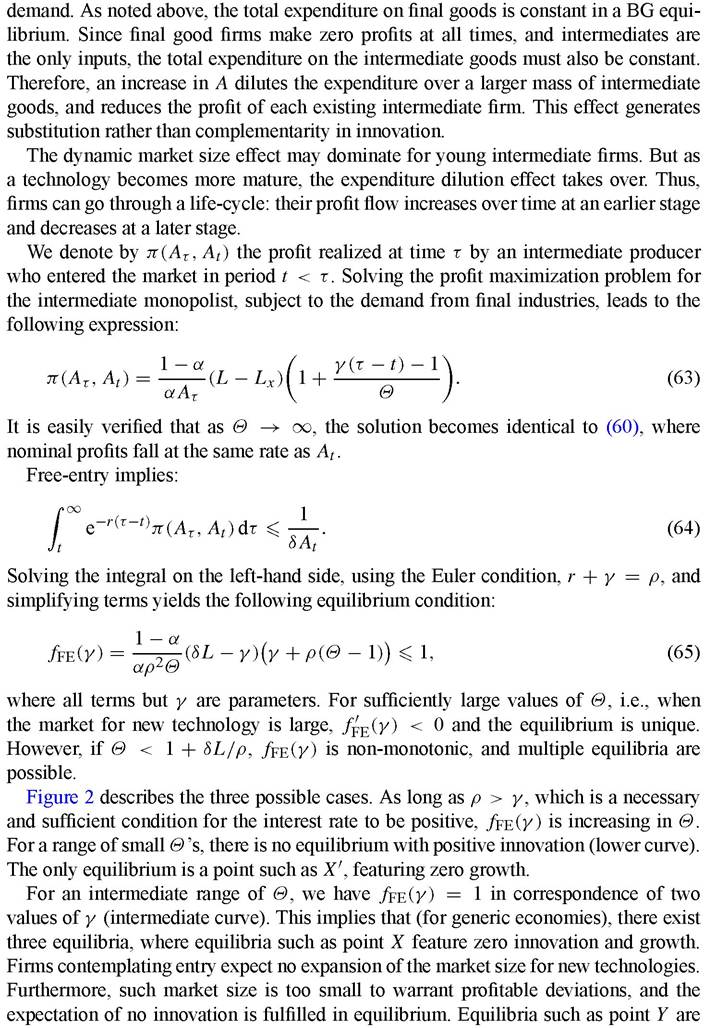

At will now denote the measure of both final goods and intermediate goods available in the economy at t. Final products are imperfect substitutes in consumption, and the instantaneous utility function is:[59] [60] [61] with total utility being This specification implies that consumers’ needs grow as new goods become available. Suppose, for instance, that a measure ε of new goods is introduced between time t and t + j.At time t, consumers are satisfied with not consuming the varieties yet to be invented. The productive technology for the s ’th final good is given by Note that profits fall over time at the rate at which knowledge grows. In a BG equilibrium, the interest rate is constant and A grows at the constant rate γ. Free entry implies: where we have used the fact that γ = δLx. Simplifying terms yields The intertemporal optimality condition for consumption also differs from the benchmark model. In particular, if E denotes the total expenditure in final goods, the Euler condition is:41 In a BG equilibrium, the total expenditure on consumption goods is constant. Hence, This expression can be substituted into (61) to give a unique solution for γ. As long as growth is positive, we have [62] [1] See Young (1993, p. 783) for the derivation of this Euler equation. Figure 2. characterized by local complementarity in innovation: the expectation of higher future innovation and growth increases the value of new firms, stimulating current entry and innovation. In steady-state (BG), this implies a positive slope of the locus fFE(γ).43 Eventually, for sufficiently high growth rates, the diversion effect dominates. Thus, in an equilibrium like Z, the value of innovating firms depends negatively on the speed of innovation.43 [63] [64] Finally, for a range of large Θ’s, substitution dominates throughout (upper curve). The initial market for new technologies is sufficiently large to make the expenditure diversion effect dominate the market size effect, even at low growth rates. The equilibrium is unique, and the solution is isomorphic to that of the benchmark model of expanding variety. 6.