Confronting the theory with some facts

Although the above framework is extremely simple, it generates a number of predictions for empirical analysis on emerging markets. In particular, our model predicts that:

1. The investment to GDP and private credit to GDP ratios should increase during a “lending boom.” To see this in the context of the above model, just note that:

which indeed increases during a lending boom as a result of the price effect;

2.

Lending booms are times of net capital inflows; this in turn follows from the fact that the capital account (or net capital flow) at any date t, is equal to:

so that

which is indeed negative if, as one would reasonably expect in a small open economy, domestic savings are only weakly correlated with borrowers' wealth;

3. The real exchange rate should increase during a lending boom; this immediately follows from the real exchange rate being simply equal to pt in our model;

4. The probability of default should increase during a lending boom; this conclusion obtains in a straightforward extension of our model with output uncertainty and defaults, which we develop in Aghion et al. (2004a).

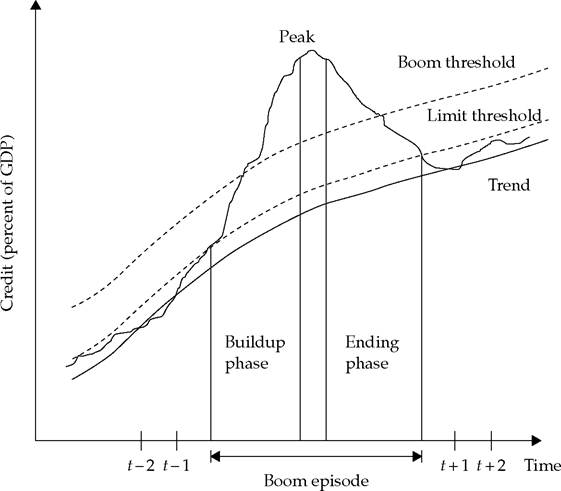

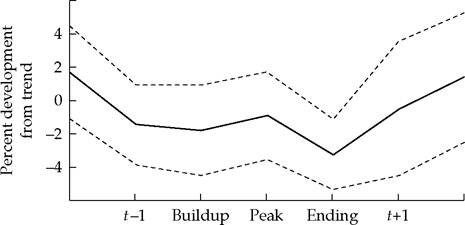

Fig. 4.2 Definition of a lending boom episode. Source: GVL (2001), figure 1.

Recent work by Gourinchas-Valdes-Landerretche (2001), henceforth GVL, provides strong empirical support for all of these predictions. First, they define a lending boom as “a deviation of the ratio between nominal private credit and nominal GDP from a rolling retrospective country-specific stochastic trend." This definition encompasses the booms in our model.

As shown in Figure 4.2, each lending boom comprises a buildup phase during which the credit to GDP ratio increases beyond its long-run trend, a peak phase where the credit stops growing faster than GDP, and finally an ending phase during which the credit to GDP ratio decreases below its long-run trend.Second, they consider a cross-country sample comprising 91 countries over the period 1960-96. They measure private credit by the amount of claims of nonbanking institutions from banking institutions, and they estimate the trend of the corresponding credit to GDP ratio by using a rolling Hodrick-Prescott filter for each country.

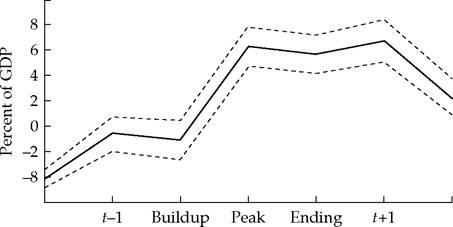

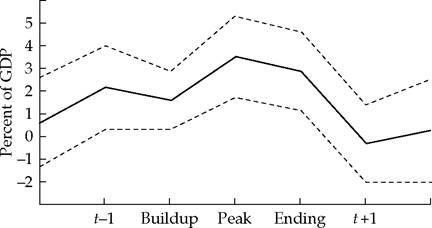

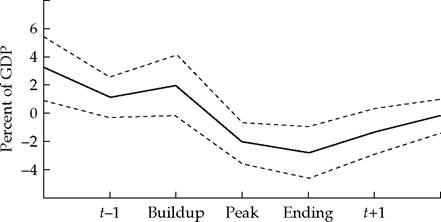

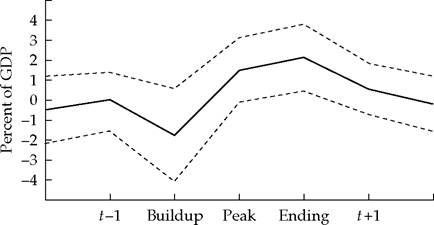

The behavior of macroeconomic indicators such as aggregate output, investment to GDP, private credit, the current account, and the real exchange rate is shown to be fully consistent with the above predictions. In particular: (i) Figure 4.3 shows that the ratio of private credit to GDP increases sharply during the buildup phase of a lending boom; (ii) Figure 4.4 shows a similar pattern for the investment to GDP ratio, which also increases sharply during the buildup phase of a lending boom and then decreases during the ending phase; (iii) Figure 4.5 shows that the current account decreases and becomes negative during the buildup phase

Fig. 4.3 Private credit/GDP.

Source: GVL (2001), figure 6.1.

Fig. 4.4 Investment/GDP.

Source: GVL (2001), figure 6.4.

Fig. 4.5 Current account/GDP.

Source: GVL (2001), figure 6.11.

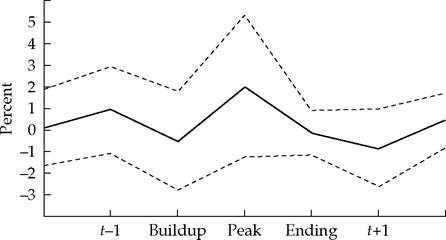

Fig. 4.6 Private capital flows/GDP.

Source: GVL (2001), figure 6.13.

and then increases again during the ending phase; (iv) Figure 4.6 shows that the inflow of private capital is (increasingly) positive during the buildup phase, but reverses to negative later on;

(v) Figure 4.7 shows that the real exchange rate increases during the buildup phase and decreases during the ending phase;

(vi) Figure 4.8 shows that the interest spread—which is positively correlated with the likelihood of defaults—increases during the buildup phase and decreases during the ending phase, although GVL point out that this pattern is not significant.

By comparing with “tranquil periods," GVL show that during lending booms the output gap is higher, the investment/GDP ratio increases, the proportion of short-term debt increases, the current account worsens, and the real exchange rate appreciates, especially

Fig. 4.7 Real exchange rate.

Source: GVL (2001), figure 6.12.

Fig. 4.8 Interest rate spread.

Source: GVL (2001), figure 6.7.

at the end of the boom period. When lending declines, all these movements are reversed. In particular, the fact that investment follows a credit expansion and is sharply procyclical is fully consistent with our approach.

4.2