Financial liberalization and instability

The previous analysis shows that a fully open economy with imperfect credit markets can exhibit volatility or a cycle. We show in this section that the same economy can be stable if it is closed to capital flows or if only foreign direct investment (FDI) is allowed.

Thus, a full liberalization to capital movements may destabilize an economy: while it stabilizes the real interest rate, it also amplifies the fluctuations in the price of the country-specific factor. This in turn, increases the volatility in firms' cash flows and therefore aggregate output. We first consider the case of an economy that opens up to foreign lending. Then, we examine the case of FDI, where foreign investors are equity holders and are fully informed about domestic firms. Even though the results are valid with general production functions, we present the Leontief case for pedagogical reasons.4.4.1 Liberalizing foreign borrowings

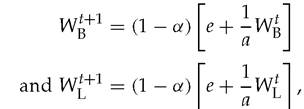

We consider an economy with low domestic savings, with the Leontief technology specified in Section 4.2, and we first assume that this economy is not open to foreign borrowing and lending.[12] In that case, at each date, the current wealth of domestic lenders WL matters since domestic investment is constrained by domestic savings Wb + Wl- Now suppose that the initial levels of wealth held by entrepreneurs and domestic lenders, Wb and Wl respectively, are sufficiently small so that initially p0 = 0. This corresponds to a situation where domestic entrepreneurs cannot exhaust the supply of country-specific inputs. Let us also assume that at date 0 domestic savings WB + WL are less than the investment capacity μWB-[13] If μ > 1 there will then be excess investment capacity in subsequent periods as long as pt remains equal to 0. To see this, note that the domestic interest rate rt, determined in a closed economy by the comparison between WL and (μ — 1) WB, is such that entrepreneurs are indifferent between borrowing and lending, that is: rt = 1/a in the Leontief case.

Therefore, if pt = 0 and WL < (μ — 1)WB,we have:

so that W£ < (μ — 1)WB implies that: WB+1 < (μ — 1)WB+1 and therefore rt+1 = 1/a. InAghion et al. (2004a) we provide sufficient conditions under which pt = 0 and rt = 1/a for all t. Under these conditions, entrepreneurs' wealth will grow at the (low) rate (1 — α)∕a, since it is constrained by the (low) level of domestic savings, and the WB+1 (WB) schedule will intersect the 45o line on its first branch along which pt = 0. This, in turn, implies that there will be no persistent fluctuations in this closed economy.

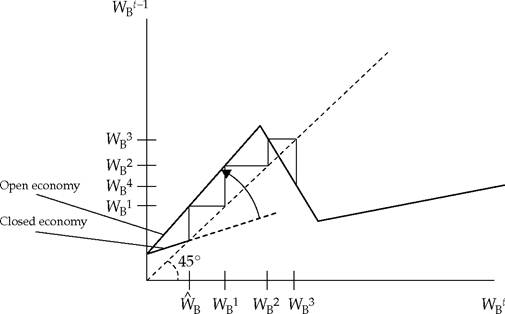

What happens if this economy is fully opened up to foreign borrowing and lending? The interest rate will be fixed at the international level r. By itself, this could only help stabilize any closed economy that otherwise might (temporarily) fluctuate in reaction to interest rate movements. However, the opening up of the economy to foreign lending also brings net capital inflows as investors satisfy their excess funds demand in international capital markets. The corresponding rise in borrowing in turn increases the scope for bidding up the price of the country-specific factor, thereby inducing permanent fluctuations in p, Wb and aggregate output.

Figure 4.9 presents an illustration of the impact of liberalization. The wealth schedule shifts up after a capital account liberalization. Wb refers to the stable steady-state level of borrowers' wealth before the economy opens up to foreign borrowing and lending. After the liberalization Wb progressively increases as capital inflows allow investors to increase their borrowing, investments, and profits. During the first two periods following the liberalization, the demand for the country-specific factor remains sufficiently low so that p = 0.

In period 3 (at WB) p increases but we still have growth. However, in period 4 (at WB4) the price effect of the liberalization becomes sufficiently strong as to squeeze investors' net worth, thereby bringing on a recession. At that point, aggregate lending drops, capital flows out and the real exchange depreciates (p drops). The resulting gain in competitiveness allows firms to rebuild their net worth so that growth can

Fig. 4.9 Liberalizing foreign lending.

Source: Aghion et al. (2004a), figure 4.

eventually resume. The economy ends up experiencing permanent fluctuations of the kind described in the previous section.

We should stress that the dynamics in Figure 4.9 occurs only for intermediate levels of financial development. As we argued in Section 4.2, with a large μ there is no volatility in an open economy, as it is the third segment of the curve that cuts the 45o line. When μ = 1, financial opening will not help investment and no capital inflow will occur, so there will be no upward pressure on the price of the country-specific input.[14] The above example therefore suggests that it might be desirable for a country to increase its μ, that is, to develop its domestic financial sector before fully opening up to foreign lending.

4.4.2 Foreign direct investment

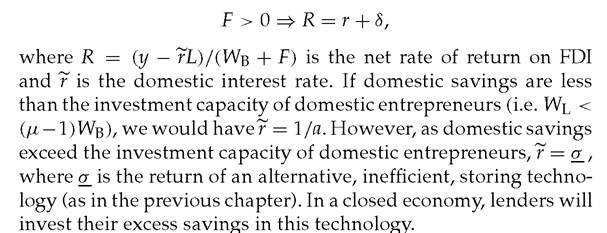

Whilst a full liberalization to foreign lending can have destabilizing effects on economies with intermediate levels of financial development, those economies are unlikely to become volatile as a result of opening up to foreign direct investment alone. We distinguish FDI from other financial flows by assuming that it is part of firms' equity.8 Furthermore, we first concentrate on the benchmark case where the supply of FDI is infinitely elastic at some fixed price greater than the world interest rate, say equal to r + δ.9

Starting from a situation in which domestic cash flows are small so that domestic investment cannot fully absorb the supply of country-specific factors, foreign direct investors are likely to enter in order to profit from the low price of the country-specific factors.

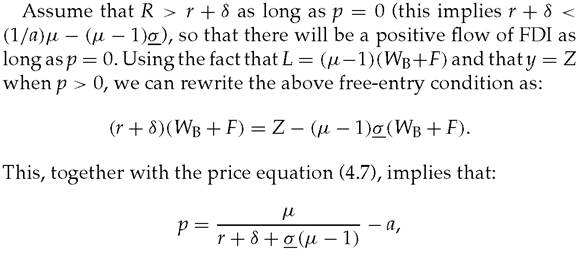

This price will eventually increase and may even fluctuate as a result of FDI. But these price fluctuations will only affect the distribution of profits between domestic and foreign investors, not aggregate output. For example, in the Leontief case with FDI, aggregate output will stabilize at a level equal to the supply of factor resources Z, whereas the same economy may end up being destabilized if fully open to foreign portfolio investment (i.e. to foreign lending).Consider a closed Leontief economy open to FDI only. Assume also that Wl is large enough so that firms can still borrow their desired amount domestically (otherwise investment is still constrained by savings and the scope for fluctuations is much smaller). Then FDI will flow into the economy as long as the rate of return on that investment remains greater than or equal to r + δ. Thus, if F denotes the net inflow of direct investment, in equilibrium we obtain the free-entry condition:

8Typically, measured FDI implies participations of more than 10% in a firm's capital so this appears to be a reasonable assumption. Razin et al. (1998) make a similar distinction about FDI.

9This, in turn, implies that in our model FDI is a substitute to domestic investment. The effects of FDI on macroeconomic volatility when domestic and foreign investments are complementary, are discussed at the end of this section.

which in turn defines gives a stable value for p. Thus, even though FDI leads to a price increase it does not generate price and output volatility.

Consider now an economy which has already been opened up to foreign borrowing and lending at rate r, that is to foreign portfolio flows only, and which, as a result has become volatile as in the example depicted in Figure 4.9. What will happen if this economy is now also opening up to FDI? By the same reasoning as before, opening up to FDI will stabilize the price of the country-specific factor at level p* such that:

This again will eliminate investment and output volatility in this economy (assuming that initially the country is attracting FDI).

In other words, if there are no limitations on FDI inflows and outflows (and FDI involves complete information on domestic firms), the price of the country-specific factor and therefore aggregate domestic GDP or GNP will remain constant in equilibrium.The reason why FDI acts as a stabilizing force is again that, unlike foreign lending, it does not depend on the creditworthiness of the domestic firms, and furthermore it is precisely during slumps that foreign direct investors may prefer to come in so as to benefit from the low price of the country-specific factor.

What happens if FDI is complementary to domestic direct investment, that is, to Wb? Such complementarity may be due to legal restrictions whereby the total amount of FDI cannot be greater than a fixed fraction x of domestic investors' wealth Wb, or it may stem from the need for local investors to enforce dividend payments or to help exert control. Aghion et al. show that FDI subject to complementarity requirements of the form F ≤ r¾ may sometimes de-stabilize an emerging market economy. Indeed, in contrast to the unrestricted FDI case analyzed above, such direct investments ultimately will fall during slumps, that is, when investors' wealth WB+1 is experiencing a downturn. Downturns will also typically be deeper than in the absence of FDI since, by amplifying the increase in pt during booms, FDI increases production costs and thus accentuates the credit-crunch induced on firms. Thus, while unrestricted FDI has a stabilizing effect on an open emerging market economy, opening such an economy to restricted FDI may actually have the opposite effect.

4.3

More on the topic Financial liberalization and instability:

- THE GREAT DEBATE AS TO DETERMINATION OF MONEY SUPPLY IN INDIA

- Methods of integration

- The “dramatic circumstances” and the origins of the U.S. constitutional order

- Implementation Issues for the 2008 Constitution

- Appendix B: Variables in cross-country growth regressions

- Widening and deepening in the shadow of the Cold War

- Comparative Reflections and Tentative Evaluation