Linking growth to IO: innovate to escape competition

One particularly unappealing feature of the basic Schumpeterian model outlined in Section 2 is the prediction that product market competition is unambiguously detrimental to growth because it reduces the monopoly rents that reward successful innovators and

Ch.

2: Growth with Quality-Improving Innovations: An Integrated Framework 85thereby discourages R&D investments. Not only does this prediction contradict a common wisdom that goes back to Adam Smith, but it has also been shown to be (partly) counterfactual [e.g., by Geroski (1995), Nickell (1996), and Blundell et al. (1999)].20

However, as we argue in this section, a simple modification reconciles the Schumpeterian paradigm with the evidence on product market competition and innovation, and also generates new empirical predictions that can be tested with firm- and industrylevel data. In this respect the paradigm can meet the challenge of seriously putting IO into growth theory. The theory developed in this section is based on Aghion, Harris and Vickers (1997) and Aghion et al. (2001), but cast in the discrete-time framework introduced above.

4.1. Thetheory

We start by considering an isolated country in a variant of the technology-transfer model of the previous section. This variant allows technology spillovers to occur across sectors as well as across national borders. Thus there is a global technological frontier that is common to all sectors, and which is drawn on by all innovations. The model takes as given the growth rate of this global frontier, so that the frontier At at the end of period t obeys:

where γ > 1.

In each country, the general good is produced using the same kind of technology as in the previous sections, but here for simplicity we assume a continuum of intermediate inputs and we normalize the labor supply at L = 1, so that:

20 We refer the reader to the second part of this section where we confront theory and empirics on the relationship between competition/entry and innovation/productivity growth. incumbent firm in any sector at the end of period t, will depend upon the technological position of that firm with regard to the technological frontier at the end of the period.

Between the beginning and the end of the current period t, the incumbent firm in any sector i has the possibility of innovating with positive probability. Innovations occur step-by-step: in any sector an innovation moves productivity upward by the same factor γ. Incumbent firms can affect the probability of an innovation by investing more  reflects a knowledge externality from more advanced sectors which limits the maximum distance of any sector to the technological frontier.

reflects a knowledge externality from more advanced sectors which limits the maximum distance of any sector to the technological frontier.

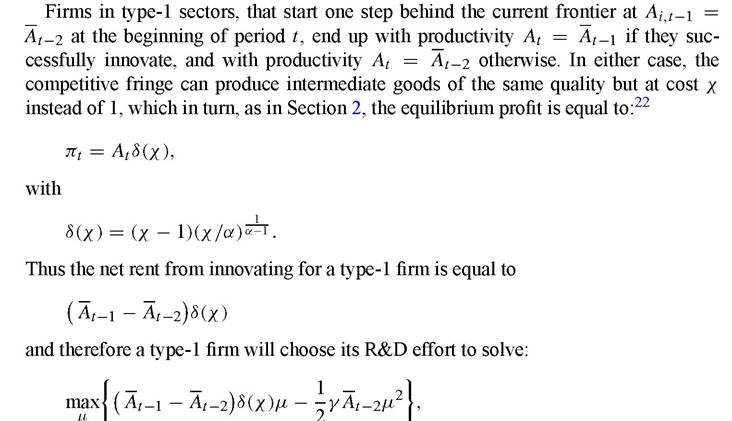

Now, consider the R&D incentives of incumbent firms in the different types of sectors at the beginning of period t. Firms in type-2 sectors have no incentive to invest in R&D since innovation is automatic in such sectors. Thus  where μj is the equilibrium R&D choice in sector j.

where μj is the equilibrium R&D choice in sector j.

21 We thus depart slightly from our formulation in the previous sections: here we take the probability of innovation, not the R&D effort, as the optimization variable. However the two formulations are equivalent: that the innovation probability f(n) = μ is a concave function of the effort n, is equivalent to saying that the effort is a convex function of the probability.

22 Imitation does not destroy the rents of non-innovating firms. We assume nevertheless that the firm ignores any continuation value in its R&D decision.

which yields

In particular an increase in product market competition, measured as an reduction in the unit cost χ of the competitive fringe, will reduce the innovation incentives of a type-1 firm. This we refer to as the Schumpeterian effect of product market competition: competition reduces innovation incentives and therefore productivity growth by reducing the rents from innovations of type-1 firms that start below the technological frontier. This is the dominant effect, both in IO models of product differentiation and entry, and in basic endogenous growth models as the one analyzed in the previous sections. Note that type-1 firms cannot escape the fringe by innovating: whether they innovate or not, these firms face competitors that can produce the same quality as theirs at cost χ. As we shall now see, things become different in the case of type-0 firms.

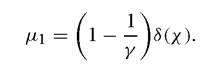

In particular an increase in product market competition, i.e. a reduction in χ, will now have a fostering effect on R&D and innovation. This, we refer to as the escape competition effect: competition reduces pre-innovation rents of type-0 incumbent firms, but not their post-innovation rents since by innovating these firms have escaped the fringe. This in turn induces those firms to innovate in order to escape competition with the fringe.

The combination of these two effects can explain the non-monotonicity of the relationship between competition and growth that we find in the data.

4.1. Empirical predictions

The above analysis generates interesting predictions:

1. Innovation in sectors in which firms are close to the technology frontier, react positively to an increase in product market competition;

2.

Innovation reacts less positively, or negatively, in sectors in which firms are further below the technological frontier.These predictions have been confronted by Aghion et al. (2002) with UK firm level data on competition and patenting, and we briefly summarize their findings in the next subsection.

4.2. Empirical evidence and relationship to literature

Most innovation-based growth models - including the quality improvement model developed in the above two sections - would predict that product market competition is detrimental to growth as it reduces the monopoly rents that reward successful innovators (we refer to this as the Schumpeterian effect of competition). However, an increasing number of empirical studies have cast doubt on this prediction. The empirical IO literature on competition and innovation starts with the pioneering work of Scherer (1967), followed by Cohen and Levin (1989), and more recently by Geroski (1995). All these papers point to a positive correlation between competition and growth. However, competition is often measured by the inverse of market concentration, an indicator which Boone (2000) and others have shown to be problematic: namely, higher competition between firms with different unit costs may actually result in a higher equilibrium market share for the low cost firm! More recently, Nickell (1996) and Blundell et al. (1999) have made further steps by conducting cross-industry analyses over longer time periods and by proposing several alternative measures of competition, in particular the inverse of the Lerner index (defined as the ratio of rents over value added) or by the number of competitors for each firm in the survey. However, none of these studies would uncover the reason(s) why competition can be growth-enhancing or why the Schumpeterian effect does not seem to operate.

It is by merging the Schumpeterian growth paradigm with previous patent race models (in which each of two incumbent firms would both, compete on the product market and innovate to acquire a lead over its competitor), that Aghion, Harris and Vickers (1997), henceforth AHV, and Aghion et al.

(2001), henceforth AHHV, have developed new models of competition and growth with step-by-step innovations that reconcile theory and evidence on the effects of competition and growth: by introducing the possibility that innovations be made by incumbent firms that compete “neck-and-neck”, these extensions of the Schumpeterian growth framework show the existence of an “escape competition” effect that counteracts the Schumpeterian effect described above. What facilitated this merger between the Schumpeterian growth approach and the patent race models, is that: (i) both featured quality-improving innovations; (ii) models with vertical innovations in turn were particularly convenient to formalize the notion of technological distance and that of “neck-and-neck” competition. A main prediction of this new vintage of endogenous growth models, is that competition should be most growth-enhancing in sectors in which incumbent firms are close to the technological frontier and/or compete “neck-and-neck” with one another, as it is in those sectors that the “escape competition” effect should be the strongest.These models in turn have provided a new pair of glasses for deeper empirical analyses of the relationship between competition/entry and innovation/growth. The two studies we briefly mention in the remaining part of this section have not only produce interesting new findings; they also suggested a whole new way of confronting endogenous growth theories with data, one that is more directly grounded on serious microeconometric analyses based on detailed firm/industry panels.

The paper by Aghion et al. (2002), henceforth ABBGH, takes a new look at the effects of product market competition on innovation, by confronting the main predictions of the AHV and AHHV models to firm level data. The prediction we want to emphasize here as it is very much in tune with our theoretical discussion in the previous subsections, is that the escape competition effect should be strongest in industries in which firms are closest to the technological frontier.

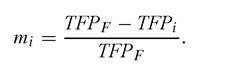

ABBGH considers a UK panel of individual companies during the period 19681997. This panel includes all companies quoted on the London Stock Exchange over that period, and whose names begin with a letter from A to L. To compute competition measures, the study uses firm level accounting data from Datastream; product market competition is in turn measured by one minus the Lerner index (ratio of operating profits minus financial costs over sales), controlling for capital depreciation, advertising expenditures, and firm size. Furthermore, to control for the possibility that variations in the Lerner index be mostly due to variations in fixed costs, we use policy instruments such as the implementation of the Single Market Program or lagged values of the Lerner index as instrumental variables. Innovation activities, in turn, are measured both, by the number of patents weighted by citations, and by R&D spending. Patenting information comes from the U.S. Patent Office where most firms that engage in international trade register their patents; in particular, this includes 461 companies on the London Stock Exchange with names starting by A to L, for which we already had detailed accounting data. Finally, technological frontier is measured as follows: suppose a UK firm (call it i) belongs to some industry A; then we measure technological distance by the difference between the maximum TFP in industry A across all OECD countries (we call it TFPf, where the subscript “F ” refers to the technological frontier) and the TFP of the UK firm, divided by the former:

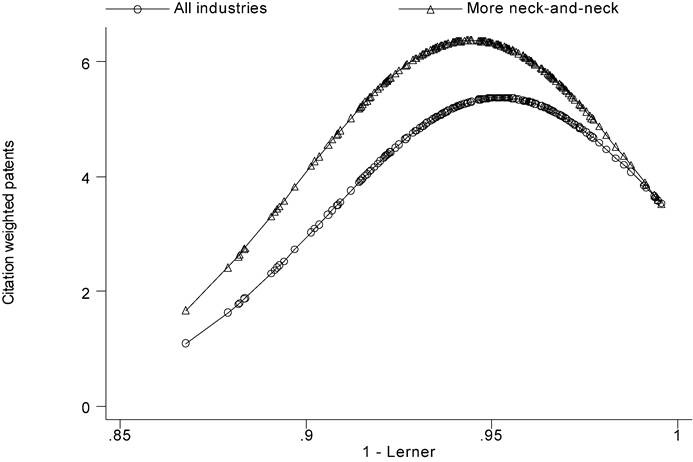

Figure 1 summarizes our main findings. Each point on this figure corresponds to one firm in a given year. The upper curve considers only those firms in industries where the average distance to the technological frontier is less than the median distance across all industries, whereas the lower curve includes firms in all industries.

Figure 1. Inovation and competention: The neck and neck split. The figure plots a measure of competition on the x-axis again citation weighted patents on the y-axis. Each point represents an industry-year. The circles show the exponential quadratic curve that is reported in column (2) of Table 1. The triangles show the exponential quadratic curve estimated only on neck-and-neck industires that is reported in column (4) of Table 1.

We clearly see that the effect of product market competition on innovation is all the more positive that firms are closer to the technological frontier (or equivalently are more “neck-and-neck”). Another interesting finding that comes out of the figure, is that the Schumpeterian effect is also at work, and that it dominates at high initial levels of product market competition. This in turn reflects the “composition effect” pointed out in the previous subsection: namely, as competition increases and neck-and-neck firms therefore engage in more intense innovation to escape competition, the equilibrium fraction of neck-and-neck industries tends to decrease (equivalently, any individual firm spends less time in neck-and-neck competition with its main rivals) and therefore the average impact of the escape competition effect decreases at the expense of the counteracting Schumpeterian effect. The ABBGH paper indeed shows that the average distance to the technological distance increases with the degree of product market competition. The Schumpeterian effect was missed by previous empirical studies, mainly as a result of their being confined to linear estimations. Instead, more in line with the Poisson technology that governs the arrival of innovations both, in Schumpeterian and in patent race models, ABBGH use a semi-parametric estimation method in which the expected flow of innovations is a piecewise polynomial function of the Lerner index.

4.3. A remark on inequality and growth

Our discussion of the effects of competition on growth also sheds light on the current debate on the effects of income or wealth inequality on growth. A recent literature[28] has emphasized the idea that in an economy with credit-constraints, where the poor do not have full access to efficient investment opportunities, redistribution may enhance investment by the poor more than it reduces incentives for the rich, thereby resulting in higher aggregate productive efficiency in steady-state and higher rate of capital accumulation on the transition path to the steady-state. Our discussion of the effects of competition on innovation and growth hints at yet another negative effect of excessive wealth concentration on growth: to the extent that innovative activities tend to be more intense in sectors in which firms or individuals compete “neck-and-neck”, taxing further capital gains by firms that are already well ahead of their rivals in the same sector may enhance the aggregate rate of innovation by shifting the overall distribution of technological gaps in the economy towards a higher fraction of neck-and-neck sectors in steady-state.

More generally, having too many sectors in which technological knowledge and/or wealth are highly concentrated, may inhibit growth as it both, discourages laggard firms or potential entrants, and reduces the leader’s incentives to innovate in order to escape competition given that the competitive threat coming from laggards or potential entrants is weak; the leader may actually prefer to invest her wealth into entry deterrence activities. These considerations may in turn explain why, following a high growth period during the industrial revolution in the 19th century, growth slowed down at the turn of the 20th century in France or England at the same time wealth distribution became highly concentrated: the high concentration of wealth that resulted from the industrial revolution, turned the innovators of the mid 19th century into entrenched incumbents with the power to protect their dominant position against competition by new potential entrants.[29]

5.