Nonconvexities, complementarities and imperfect competition

Increasing returns production under imperfect competition is a natural framework to think about multiple equilibria. Imperfect competition leads directly to externalities transmitted through the price system, because monopolists themselves, rather than Walrasian auctioneers, set prices, and presumably they do so with their own profit in mind.

At the same time, their pricing and production decisions impinge on other agents. These general equilibrium effects can be a source of multiplicity.Section 5.1 illustrates this idea using the big push model of Murphy, Shleifer and Vishny (1989); a model which formalizes an earlier discussion in Rosenstein-Rodan (1943). Rosenstein-Rodan argued that modern industrial technology is freely available to poor countries, but has not been adopted because the domestic market is too small to justify the fixed costs it requires. If all sectors industrialize simultaneously, however, the market may potentially be expanded to the extent that investment in modern technology is profitable.

Thus the big push model of Section 5.1 helps to clarify the potential challenges posed by coordination for the industrialization process. We shall see that the major coordination problem facing monopolists cannot be resolved by the given market structure. In this situation, the ability of a society to successfully coordinate entrepreneurial activity - and thereby realize the social benefits available in modern production technologies - will depend in general on such structures as its institutions, political organizations, the legal framework, and social and business conventions.

In countries such as South Korea, the state has been very active in attempting to overcome coordination problems associated with industrialization. In Western Europe, the state was typically much less active, and the role of the private sector was correspondingly larger.

For example, Da Rin and Hellmann (2002) have recently emphasized the important role played by banks in coordinating industrialization. Section 5.2 reviews their model.A theme of this survey is traps that prevent economies as a whole from adopting modern production technologies. One aspect of this transformation to modernity is the need for human capital. If investment in human capital has a high economic payoff then a skilled work-force should spontaneously arise. Put differently, if the poor are found to invest little in schooling or training then this suggests to us that returns to these investments are relatively low. Section 5.3 reviews Kremer’s (1993) matching model, where low investment in schooling sustains itself in a self-reinforcing trap.

Finally, Section 5.4 gives references to notable omissions on the topic of increasing returns.

5.1. Increasing returns and imperfect competition

Murphy, Shleifer and Vishny’s (1989) formalization of Rosenstein-Rodan’s (1943) big push is something of a watershed in development economics. Their model turns on demand spillovers which create complementarities to investment. They point out that for the economy to generate multiple equilibria, it must be the case that investment simultaneously (i) increases the size of other firms’ markets, or otherwise improves the profitability of investment; and (ii) has negative net present value. This means that profits alone cannot be the direct source of the market size effects; otherwise (i) and (ii) would be contradictory.

In the first model they present, higher wages in the modern sector are the channel through which demand spillovers increase market size. Although investment is not individually profitable, it raises labor income, which in turn raises the demand for other products. If the spillovers are large enough, multiple equilibria will occur. In their second model, investment in the modern technology changes the composition of aggregate demand across time. In the first period, the single monopolistic firm in each sector decides whether to invest or not.

Doing so incurs a fixed cost F in the first period, and yields output ωL in the second, where ω > 1 is a parameter and L is labor input. The cost in the second period is just L, as wages are the numeraire. If, on the other hand, the monopolist chooses not to invest, production in that sector will take place in a “competitive fringe” of atomistic firms using constant returns to scale technology. For these firms, one unit of labor input yields one unit of output. The price for each unit so produced is unity.All wages and profits accrue to a representative consumer, who supplies L units of labor in both periods, and maximizes the undiscounted utility of his consumption, that is,

52 To simplify the exposition we assume that consumers can neither save nor dissave from current income. For the moment we also abstract from the existence of a financial sector. Firms which invest simply pay all wages in the second period at a zero rate of interest. See the original for a more explicitly general equilibrium formulation.

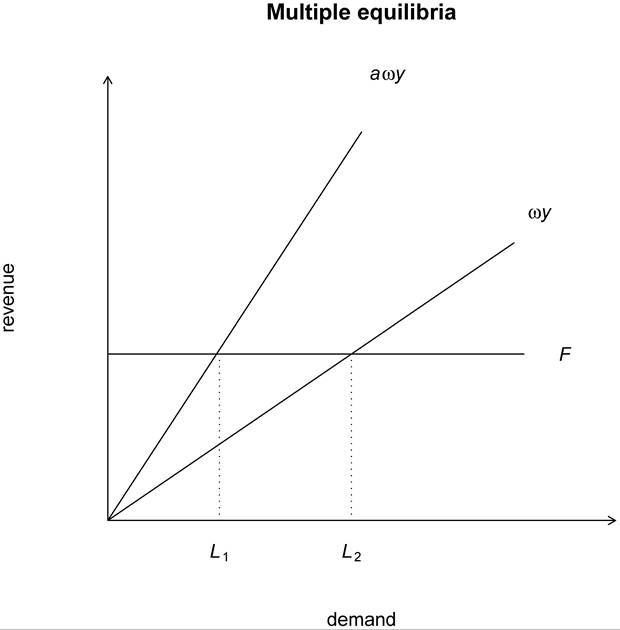

Figure 18.

Consider profitability when all entrepreneurs corresponding to sectors [0, α] decide to invest. (The number α can also be thought of as the fraction of the total number of monopolists who invest.) It turns out that for some parameter values both α = 0 and α = 1 are equilibria. To see this, consider first the case α = 0, so that y1 = y2 = L. It is not profitable for a firm acting alone to invest if π = aL — F ≤ 0. On the other hand, if α = 1, then y1 = L — F and y2 = ωL, so monopolists make positive profits when aωL — F 0. Multiple equilibria exist if these inequalities hold simultaneously. In Figure 18 multiple equilibria obtain for all L ∈ [L1, L2].

As was mentioned in the introduction, coordination problems and other mechanisms that reinforce the status quo can interact with each other and magnify their individual impact. Murphy, Shleifer and Vishny (1989) provide a simple example of this in the context of the model outlined above. They point out that the coordination problem for the monopolists is compounded if industrialization requires widespread development of infrastructure and intermediate inputs, such as railways, road networks, port facilities and electricity grids. All of these projects will themselves need to be coordinated with industrialization.

For example, suppose that n infrastructure projects must be undertaken in the first period to permit industrialization in the second. Each project has a fixed cost Rn, and operates in the second period at zero marginal cost. Leaving aside the issue of how the spoils of industrialization will be divided among the owners of the projects and the continuum of monopolists, it is clear that industrialization has the potential to be profitable for all only when aωL — F,the profits of the monopolists when α = 1, exceed total infrastructure costs ∑"=1 Ri.

If the condition aL — F ≤ 0 continues to hold, however, individual monopolists investing alone will be certain to lose money. Realizing this, investors in infrastructure face extrinsic uncertainty as to whether or not industrialization will actually take place. Given their subjective evaluation, they may choose not to start their infrastructure projects. In turn, the monopolists are aware that investors in infrastructure face uncertainty, and may themselves refrain from starting projects. This makes monopolists even more uncertain as to whether or not the conditions for successful industrialization will eventuate. The fixed point of this infinite regression of beliefs may well be inaction. In either case, the addition of more actors adds to the difficulty of achieving coordination.

5.2. The financial sector and coordination

As Da Rin and Hellmann (2002) have recently emphasized, one candidate within the private sector for successfully coordinating a big push type industrialization is the banks. Banks are the source of entrepreneurs’ funds, and shape the terms and conditions under which capital may be raised. In addition, banks interact directly with many entrepreneurs. Finally, banks can potentially profit from coordinating industrialization if their market power is large.

Da Rin and Hellmann find that the structure and legal framework of the banking sector are important determinants of its ability to coordinate successful industrialization. To illustrate their ideas, consider again the big push model of Section 5.1. In order to make matters a little easier, let us simply define the second period return of monopolists (entrepreneurs) to be f(α), where α is the fraction of entrepreneurs who decide to set up firms and the function f: [0, 1] → R is strictly increasing. As before, there is a fixed cost F to be paid in the first period, which we set equal to 1. The future is not discounted.

It is convenient to think of the number of entrepreneurs as some large but finite number N.[238] In addition to these N entrepreneurs, there is now a financial sector, members of whom are referred to as either “banks” or “investors”. There are B ∈ N banks, the first B — 1 of which have an intermediation cost of r per unit of investment. The last

In other words, a ∈ Ω(σ) if, given the set of offers σ and the belief on the part of all firms that the fraction of firms entering will be a, exactly a ? 100% of firms find it optimal to enter.

Beliefs are required to be consistent in the sense that αen(σ) ∈ Ω(σ) for all σ and all n. Beliefs are called optimistic if αen = αopt for all n, where αopt(σ) := maxΩ(σ) for all σ ∈ Σ.

In other words, all agents believe that as many firms will enter as are consistent with offer σ, and this is true for every σ ∈ Σ. Beliefs are defined to be pessimistic if the opposite is true; that is, if αen = αpes for all n, where αpes (σ) := min Ω(σ) for all σ ∈ Σ.Da Rin and Hellmann first observe that if f = 0, then the outcome of the game will be determined by beliefs. In particular, if beliefs are pessimistic, then the low equilibrium α = 0 will obtain. If beliefs are optimistic, then the high equilibrium α = 1 will obtain. The interpretation is that when f = 0, so that the market for financial services is entirely competitive (in the sense of Bertrand competition with identical unit costs described above), the existence of the financial sector will not alter the primary role of beliefs in determining whether industrialization will take place.

Let us verify this observation in the case of pessimistic beliefs. To do so, it is sufficient to show that if σ ∈ Σ is optimal, then 0 ∈ Ω(σ). The reason is that if 0 ∈ Ω(σ), then by (20) we have π(0, mn(σ)) < 0 for all n. Also, beliefs are pessimistic, so αen(σ) = min Ω(σ ) = 0. Inthis case no firms enter by (19).

To see that 0 ∈ Ω(σ) for all optimal σ, suppose to the contrary that σ ∈ Σ is optimal, but 0 / Ω(σ). Then π(0, mk(σ)) '≥ 0 for some k, in which case (18) implies that mk(σ) < r. Because firms only accept contracts at rates less than r (that is, mn(σ) ≤ r for all n), it follows from (16) that the bank which lent to k looses money, and σ is not optimal. The intuition is that no bank has market power, and cannot recoup losses sustained when encouraging firms to enter by offering low interest rates.

More interesting is the case where the last bank B has market power. With sufficient market power, B will induce industrialization (the high equilibrium where α = 1) even when beliefs are pessimistic:

Proposition 5.1 (Da Rin and Hellmann). Suppose beliefs are pessimistic. In this case, there exists an α ∈ [0, 1] depending on r and f such that industrialization will occur whenever I, the market power of B, satisfies l/N f α.

The result shows that rather than relying on spontaneous coordination of beliefs, financial intermediaries may instead be the source of coordination. The key intuition is that a financial intermediary may have a profit motive for inducing industrialization. But to achieve this, two things are necessary: size and market power. Size (as captured by f) is necessary to induce a critical mass of entrepreneurs to invest. Market power (as captured by the cost advantage r) is necessary to recoup the costs of mobilizing that critical mass. We sketch Da Rin and Hellmann’s proof in Appendix A.

Until now we have considered only the possibility that the banks offer pure debt contracts. Da Rin and Hellmann also study the case where the banks may hold equity as well (i.e., universal banking). They show that in this case the threshold level at which the lead bank B has sufficient market power to mobilize the critical mass is lower. Industrialization is unambiguously more likely to occur. The reason is that equity permits B to partake in the ex post profits of the critical mass, who benefit from low interest rates on one hand and complete entry (α = 1) on the other. With a lower cost of mobilizing firms, B requires less market power to recoup these losses. In Da Rin and Hellmann’s words,

Our model provides a rationale for why a bank may want to hold equity that has nothing to do with the standard reasons of providing incentives for monitoring. Instead, equity allows a bank to participate in the gains that it creates when inducing a higher equilibrium.

In summary, the theory suggests that large universal banks with a high degree of market power can play a central role in the process of industrialization. This theory is consistent with the evidence from countries such as Belgium, Germany and Italy, where a few oligopolist banks with strong market positions played a pivotal role. Some were pioneers of universal banking, and many directly coordinated activity across sectors by participation in management. The theory may also explain why other countries, such as Russia, failed to achieve significant industrialization in the 19th Century. There banks were small and dispersed, their market power severely restricted by the state.

5.3. Matching

The next model we consider is due to Kremer (1993), and has the following features. A production process consists of n distinct tasks, organized within a firm. For our purposes n can be regarded as exogenous. The tasks are undertaken by n different workers, all of whom have their own given skill level hi ∈ [0, 1]. Here the skill level will be thought of as the probability that the worker performs his or her task successfully. We imagine that if one worker fails in their task the entire process is ruined and output is zero. If all are successful, the outcome of the process is n units of the product.[239] That is,

Consider an economy with a unit mass of workers. The distribution of skills across workers is endogenous, and will be discussed at length below. Kremer’s first point is that in equilibrium, firms will match workers of equal skill together to perform the process. The intuition is that (i) firms will not wish to pair a work-force of otherwise skilled employees with one relatively unskilled worker, who may ruin the whole process; and (ii) firms with a skilled work-force will be able to bid more for skilled workers, because the marginal value of increasing the last worker’s skill is increasing in the skill of the other workers. Thus, for each firm,

The first thing to notice about this technology is that the expected marginal return to skill is increasing. As a result, small differences in skill can have relatively large effects on output. This may go some way to explaining the extraordinarily large wage differentials between countries. Moreover, for economies with such technology, positive feedback dynamics of the kind considered in Section 3.3 may result, even if the technology for creating human capital is concave.

Another channel for positive feedbacks occurs when matching is imperfect, perhaps because it is costly or the population is finite. Exact matches may not be possible. In that case, there are potentially returns to agglomeration: Skilled people clustering together will decrease the cost of matching, and increase the likelihood of good matches. Also, an initial distribution of skills will tend to persist, because workers will choose skills so as to be where the distribution is thickest. This maximizes their chances of finding good matches. But this is self-reinforcing: Their choices perpetuate the current shape of the distribution.

There is yet another channel that Kremer suggests may lead to multiple equilibrium distributions of skill. This is the situation where skill levels are imperfectly observed. We present a simple (and rather extremist) version of Kremer’s model. In the first period, workers decide whether to undertake “schooling” or not. This education involves a common cost c ∈ (0, 1). In the second, firms match workers, produce, and pay out wages. Both goods and labor markets are competitive, and total wages exhaust revenue. Specifically, it is assumed that each worker’s wage w is (1∕n)th of firm’s output.

Not all of those who undertake schooling become skilled. We assume that the educated receive a skill level h = 1 with probability p > 1∕2 and h = 0 with probability 1 - p. Those who do not undertake schooling have the skill level h = 0. Further, h is not observable, even for workers. Instead, all workers take a test, which indicates their true skill with probability p and the reverse with probability 1 - p.55 That is,

55

We are using the same p as before just to simplify notation.

is, P{hi = 0} = 1. It follows that expected output and wage are zero. Since c > 0, it is optimal to avoid schooling.[240] [241] [242] Now consider the agent’s problem when α = 1. In the second period, the agent will be matched with other workers having the same test score. In either case, computing expected wages is a signal extraction problem. First, using the fact that agents in the pool of potential co-workers have chosen schooling with probability one, the agent can calculate probable skills of a co-worker chosen at random from the population, given their test score: What are the sources of multiple equilibria in the model? The first is pecuniary externalities in the labor market: When more agents become educated, the probability that the marginal worker can successful match with a skilled co-worker increases. In turn, this increases the returns to education.58 Second, there is imperfect information: Skilled workers cannot readily match with other skilled workers. Instead, matching is probabilistic, and depends on the overall distribution of skills. Finally, the increasing expected marginal reward for skill inherent in the production function means that the wage spillovers from the decisions of other agents are potentially large. Another important model of human capital investment with multiple equilibria is Acemoglu (1997). He shows how labor market frictions can induce a situation where technology adoption is restricted by a lack of appropriately skilled workers. Low adoption in turn reduces the expected return to training, further exacerbating the scarcity of workers who are trained. In other words, poor technology adoption and low capital investment are self-reinforcing, because they cause the very shortage of skilled workers necessary to make such investments profitable. 5.3. Other studies of increasing returns Young’s (1928) famous paper on increasing returns notes that not only does the degree of specialization depend on the size of the market, but the size of the market also depends on the degree of specialization. In other words, there are efficiency gains from greater division of labor, primarily due to application of machines. Greater specialization increases productivity, which then expands the market, leading back into more specialization, and so on. As a result, there are complementarities in investment. These complementarities can be the source of poverty traps. A detailed discussion of this process is omitted from the present survey, but only because excellent surveys already exist. See in particular Matsuyama (1995) and Matsuyama (1997). Other references include Matsuyama and Ciccone (1996), Rodriguez-Clare (1996) and Rodrik (1996). Increasing returns are also associated with geographical agglomeration. Starrett (1978) points out that agglomerations cannot form as the equilibria of perfectly competitive economies set in a homogeneous space. Thus all agglomerations must be caused either by exogenous geographical features or by some market imperfection. An obvious candidate is increasing returns. (It is difficult to see what geographical features could explain the extent of concentration witnessed in places such as Tokyo or Hong Kong.) This survey does not treat geography and its possible connections with poverty traps in much detail. Interested readers might start with the review of Ottaviano and Thisse (2004).[243] Another source of complementarities partly related to geography is positive network externalities in technology adoption. These are often thought to arise from social learning: Local experience with a technology allows the cost of adoption to decrease as the number of adopters in some network gets larger. As well as information spillovers, more adopters of a given technology may lead to the growth of local supply networks for intermediate inputs, repairs and servicing, skilled labor and so on. See, for example, Beath, Katsoulacos and Ulph (1995), Bandiera and Rasul (2003), Conley and Udry (2003), and Baker (2004). Finally, an area that we have not treated substantially in this survey is optimal growth under nonconvexities, as opposed to the fixed savings rate model considered in Section 3.3. In other words, how do economies evolve when (i) agents choose investment optimally by dynamic programming, given a set of intertemporal preferences; and (ii) the aggregate production function is nonconvex? There are two main cases. One is that increasing returns are taken to be external, perhaps as a feedback from aggregate capital stock to the productivity residual, and agents perceive the aggregate production function to be convex. In this case there is a subtle issue: In order to optimize, agents must have a belief about how the productivity residual evolves. This may or may not coincide with its actual evolution as a result of their choices. An equilibrium transition rule is a specification of savings and investment behavior such that (a) agents choose this rule given their beliefs; and (b) those choices cause aggregate outcomes to meet their expectations. Existence of such an equilibrium is far from assured. See Mirman, Morand and Reffett (2004) and references therein. Dynamics are still actively being investigated. The second case is where increasing returns are internal, and agents perceive aggregate production possibilities exactly as they are. These models generate similar poverty traps as were found for fixed savings rates in Section 3.3. The literature is large. An early investigation is Skiba (1978). See also Dechert and Nishimura (1983), who consider a per capita production function k → f(k) which is convex over a lower region of the state space (capital per worker), and concave over the remainder; and Amir, Mirman and Perkins (1991), who study the same problem using lattice programming. Majumdar, Mitra and Nyarko (1989) study optimal growth for stochastic nonconvex models, as do Nishimura and Stachurski (2004). Dimaria and Le Van (2002) analyze the dynamics of deterministic models with R&D and corruption.[244] 6.