Credit markets, insurance and risk

In terms of informational requirements necessary for efficient free market operation and low transaction costs, one of the most problematic of all markets is the intertemporal trade in funds.

Here information is usually asymmetric, and lenders face the risk of both voluntary and involuntary default [Kehoe and Levine (1993)]. Voluntary default is strategic default by borrowers who judge the expected rewards of repayment to be lower than those of not repaying the loan. Involuntary default occurs when ex post returns are insufficient to cover total loans.Facing these risks, a standard response of lenders is to make use of collateral [Kiyotaki and Moore (1997)]. But the poor lack collateral almost by definition; as a result they are credit constrained. Credit constraints in turn restrict participation by the poor in activities with substantial set up costs, as well as those needing large amounts of working capital. For the poor, then, the range of feasible income-generating activities is reduced. Thus, the vicious circle of poverty: Income determines wealth and low wealth restricts collateral. This trap is discussed in Section 6.1.61

The market for insurance is similar to the market for credit, in that information is asymmetric and transaction costs are high. This can lead to poverty traps in several ways. In Section 6.2, we study a model where poor agents, lacking access to insurance or credit, choose low risk strategies at the cost of low mean income. These choices reinforce their poverty.

In Section 6.3 we review Matsuyama’s (2004) world economy model, where all countries must compete for funds in a global financial market. On one hand, diminishing returns imply that rewards to investment in the poor countries are large. High returns attract funds and investment, and high investment provides a force for convergence.

On the other hand, credit markets are imperfect, and rich countries have more collateral. This puts them in a strong position vis-a-vis the poor when competing for capital. The inability of the poor to guarantee returns with collateral is a force for divergence.6.1. Credit markets and human capital

Consider an economy producing only one good and facing a risk free world interest rate of zero. Agents live for one period. Each has one and only one child. From their parent, the child receives a bequest x. At the beginning of life, each agent chooses between two occupations. The first is to work using a constant returns technology Y = wL, where Y is output, L is total labor input in this sector, and Ub is a productivity parameter. The agent supplies all of his or her labor endowment lt, and we define wt := Ublt as the return to this choice of occupation. We admit the possibility that lt varies stochastically, so wt may be random.

Alternatively, the agent may set up a project at cost F. The gross payoff from the project is equal to Qt. Agents with wealth xt < F may borrow to cover the costs of the project beyond which they are able to self-finance. They face interest rate i > 0, where the excess of the borrowing rate over the risk free rate reflects a credit market imperfection. In this case we have in mind costs imposed on lenders due to the need for supervision and contract enforcement [cf., e.g., Galor and Zeira (1993, p. 39)]. These costs are then passed on to the borrower.

The two stochastic productivity parameters wt and Qt are draws from joint distribution φ. We assume that Eft = 1, and that Ewt = Uj < EQt — F. Thus, the net return to setting up the project is higher on average than the wage. However, the agent may still choose to work at wage rate wt if his or her income is relatively low. The reason is that

61 See also Tsiddon (1992) for a poverty trap model connected to the market for credit.

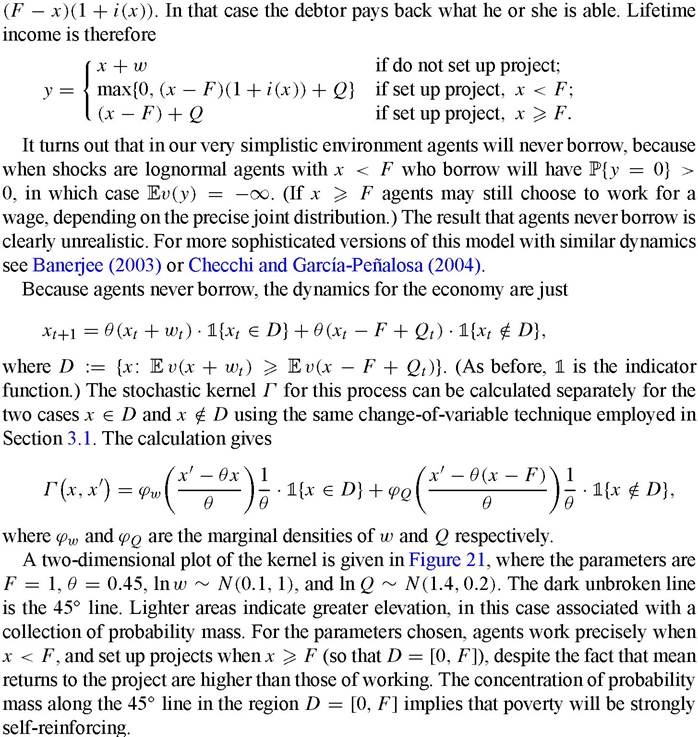

In his model, asymmetric information leads to a moral hazard problem, which restricts the ability of investors to raise money. The market solution involves quantity constraints on loans, the severity of which depends on the level of income. for the poor setting up a project requires finance at the borrowing rate i > 0, which may offset the differential return between the two occupations.Consider the employment decisions and wealth dynamics for each dynasty. Omitting time subscripts, an agent with bequest x has

It follows that dynamics for each dynasty’s wealth in this economy are given by the transition rule

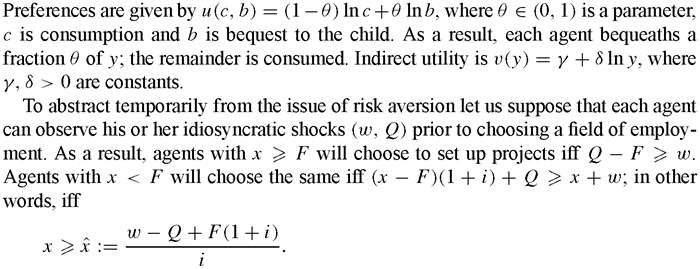

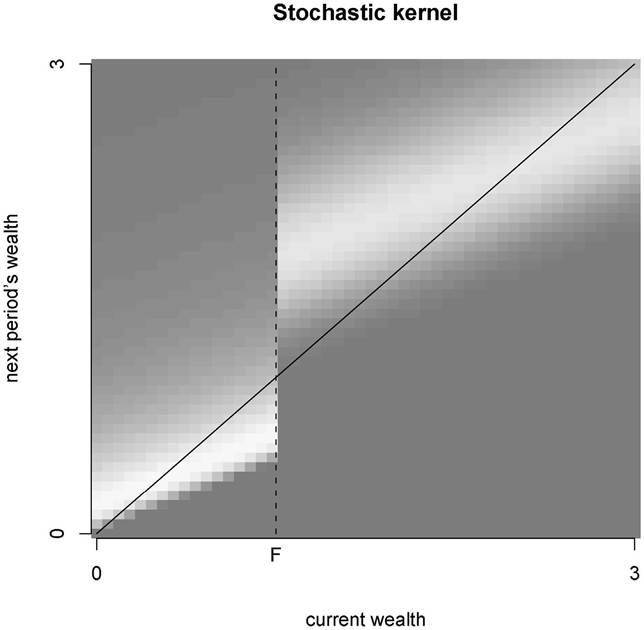

Figure 19 illustrates a transition rule S and hence the dynamics of this economy when the two rates of return are constant and equal to their means.[245] For this particular parameterization there are multiple equilibria. Agents with initial wealth less than the critical value xb will converge to the lower attractor, while those with greater wealth will converge to the high attractor. Given any initial distribution ψ0 of wealth in the economy, the fraction of agents converging to the lower attractor will be /^b dψ0. If this fraction is large, average long run income in the economy will be small.

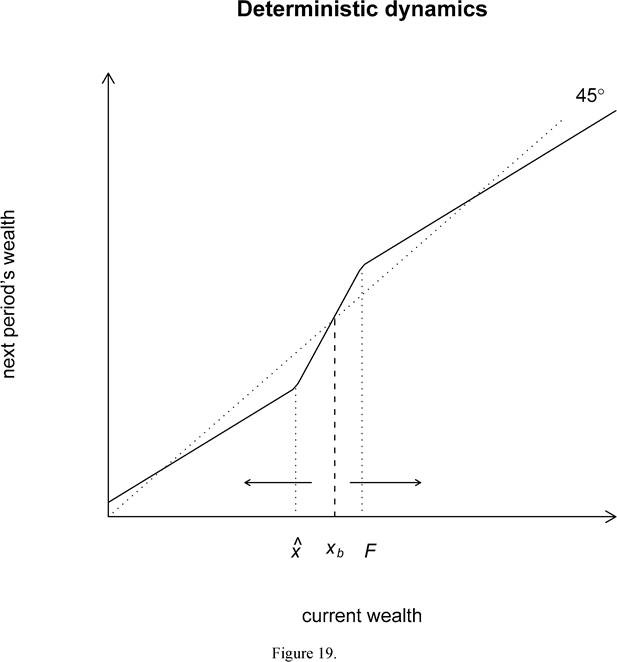

A more realistic picture can be obtained if the productivity parameters are permitted to vary stochastically around their means. This will allow at least some degree of income mobility - perhaps very small - which we tend to observe over time in almost all societies. To this end, suppose that for each agent and at each point in time the parameters wt and Qt are drawn independently across time and agents from a bivariate lognormal distribution.

In this case the transition law is itself random, and varies for each agent at each point in time.Figure 20 shows a simulated sequence of transition rules facing a given agent starting at t = 1. At t = 2 a negative shock to the project return Q causes the high level attractor

to disappear. A series of such negative shocks would cause a rich dynasty to loose its wealth. In this case, however, the shocks are iid and such an outcome is unlikely. It turns out that the time 3 shocks are strongly positive.

If the number of agents is large, then the sequence of cross-sectional distributions for wealth over time can be identified with the sequence of marginal probability laws (ψt)t≥0 generated by the Markov process xt+1 = St(xt). It is not difficult to prove that this Markov process is ergodic. The intuition and the dynamics are more or less the same as for the nonconvex growth model of Section 3.3.63 We postpone further details on dynamics until the next section, which treats another version of the same model.

There are several interpretations of the two sector story with fixed costs described above. One is to take the notion of a project or business literally, in which case F is

63 As we discussed at length in that section, it would be a mistake to claim that this ergodicity result in some way overturns the poverty trap found in the deterministic version.

Figure 20.

the cost of set up and working capital which must be paid up before the return is received. Alternatively F might be the cost of schooling, and Q is the payoff to working for skilled individuals.[246] As emphasized by Loury (1981) and others, human capital is particularly problematic for collateral-backed financing, because assets produced by investment in human capital cannot easily be bonded over to cover the risk of default.

Whatever the precise interpretation, the “project” represents an opportunity for the poor to lift themselves out of poverty, while the fixed cost F and the credit market imperfection captured here by i constitute a barrier to taking it. Microeconometric studies suggests that the effects of this phenomenon are substantial. For example, Barrett, Bezuneh and Aboud (2001) analyze the effects of a large devaluation of the local currency that occurred in Cote d’Ivoire in 1994 on rural households. They find that “A macro policy shock like an exchange rate devaluation seems to create real income opportunities in the rural sector. But the chronically poor are structurally impeded from seizing these opportunities due to poor endowments and liquidity constraints that restrict their capacity to overcome the bad starting hand they have been dealt.” [Barrett etal. (2001, p. 12)]

The same authors also study a local policy shock associated with food aid distribution in Keyna. According to this study, “The wealthy are able to access higher-return niches in the non-farm sector, increasing their wealth and reinforcing their superior access to strategies offering better returns. Those with weaker endowments ex ante are, by contrast, unable to surmount liquidity barriers to entry into or expansion of skilled nonfarm activities and so remain trapped in lower return... livelihood strategies.” [Barrett etal. (2001, p. 15)]

6.2. Risk

For the poor another possible source of historical self-reinforcement is risk. In the absence of well-functioning insurance and credit markets, the poor find ways to mitigate adverse shocks and to smooth out their consumption. One way to limit exposure is to pass up opportunities which might seem on balance profitable but are thought to be too risky. Another strategy is to diversify activities; and yet another is to keep relatively large amounts of assets in easily disposable form, rather than investing in ventures where mean return is high.

All of these responses of the poor to risk have in common the fact that they tend to lower mean income and reinforce long run poverty.A simple variation of the model from the previous section illustrates these ideas.[247] Let the framework of the problem be the same, but current shocks are no longer assumed to be previsible. In other words, each agent must decide his or her career path before observing the shocks wt and Qt which determine individual returns in each sector. Given that preferences are risk averse (indirect utility is υ(y) = γ + S ln y), the agent makes these decisions as a function not only of mean return but of the whole joint distribution. Regarding this distribution, we assume that both shocks are lognormal and may be correlated.

Lenders also cannot observe these variables at the start of time t, and hence the borrowing rate i = i(x ) reflects the risk of default, which in turn depends on the wealth x of the agent. Inparticular, default occurs when Qt is less than the debtor’s total obligations

65

Nevertheless, lognormal shocks give poor individuals a non-zero probability of becoming rich at every transition; and the rich can eventually become poor, although it might take a sequence of negative shocks. The rate of mixing depends on the parameters that make up the law of motion and the variance of the shock. Usually some small degree of mixing is a more natural assumption than none. The mixing causes the corresponding Markov chain to be ergodic. This is the case regardless of how small the tails of the shocks are made.[248] For more details on ergodicity see Appendix A.

To summarize, the poor are not wealthy enough to self-insure, and as a result choose income streams that minimize risk at the expense of mean earnings. The effect is to

Figure 21.

reinforce poverty. A number of country studies provide evidence of this behavior.[249] Dercon (2003) finds that the effects on mean income are substantial. In a review of the theoretical and empirical literature, he estimates that incomes of the poor could be 2550% higher on average if they had the same protection against shocks that the rich had as a result of their wealth [Dercon (2003, p. 14)].

A more sophisticated model of the relationship between risk and development is Acemoglu and Zilibotti (1997). In their study, indivisibilities in technology imply that diversification possibilities are tied to income. An increase in investment raises output, which then improves the extent of diversification. Since agents are risk averse, greater diversification encourages more investment. In the decentralized outcome investment is too small, because agents do not take into account the effect of their investment on the diversification opportunities of others.

67

capital

Figure 22.

Deterministic dynamics

current capital

Figure 23.

Figure 24.

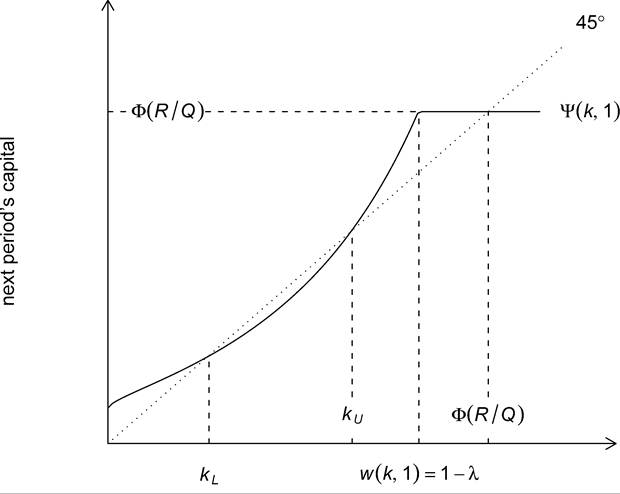

collateral, which alleviates the borrowing constraint. This in turn permits more domestic investment, which increases collateral, and so on. Individual agents do not take into account the effect of their actions on the borrowing constraint.

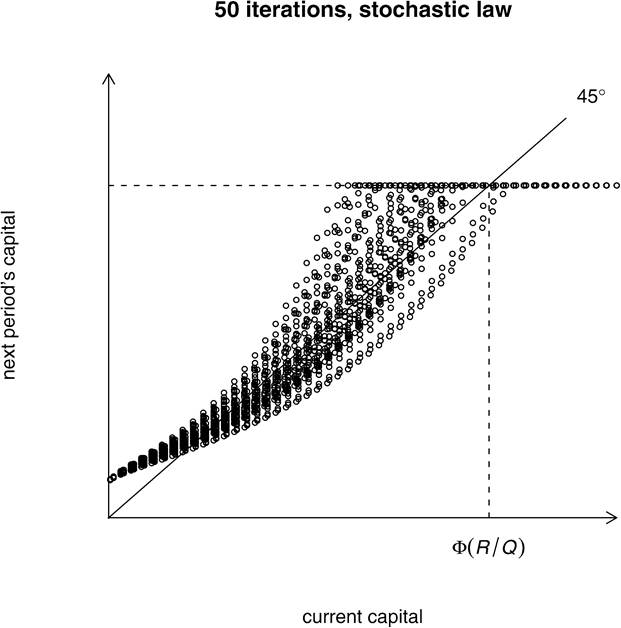

Figure 23 shows the law of motion when ξt ? 1. As drawn, there is a poverty trap at kL and another attractor at Φ(R∕Q). Countries with kt > ku tend to Φ(R∕Q), while those with kt < ku tend to kL. Figure 24 shows stochastic dynamics by superimposing the first 50 laws of motion from a simulation on the 45o diagram. The shocks (ξt)t≥0 are independent and identically distributed.[250] Notice that for particularly good shocks the lower attractor kL disappears, while for particularly bad shocks the higher attractor at Φ(R∕Q) vanishes.

Figure 25.

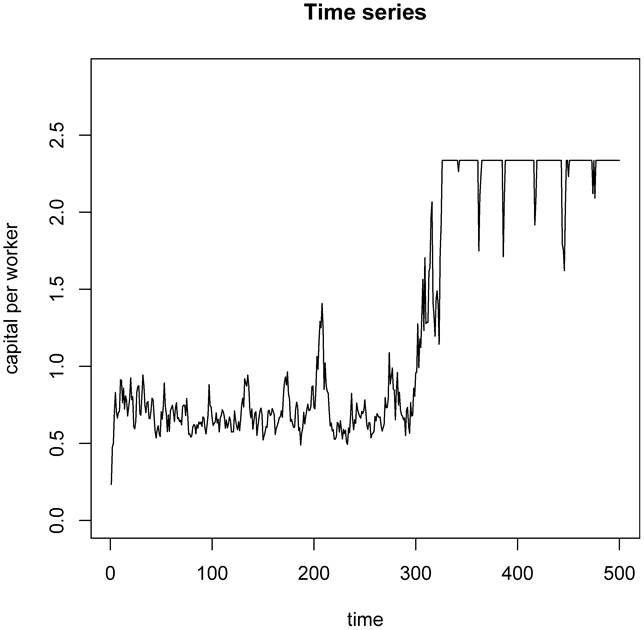

Figure 25 shows a simulated time series for the same parameters as Figure 24 over 500 periods. At around t = 300 the economy begins a transition to the higher attractor Φ(R∕Q). Subsequent fluctuations away from this equilibrium are due to shocks so negative that Φ(R∕Q) ceases to be an attractor (see Figure 24).

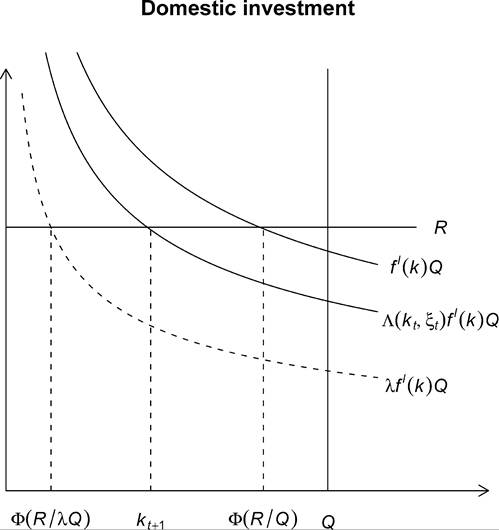

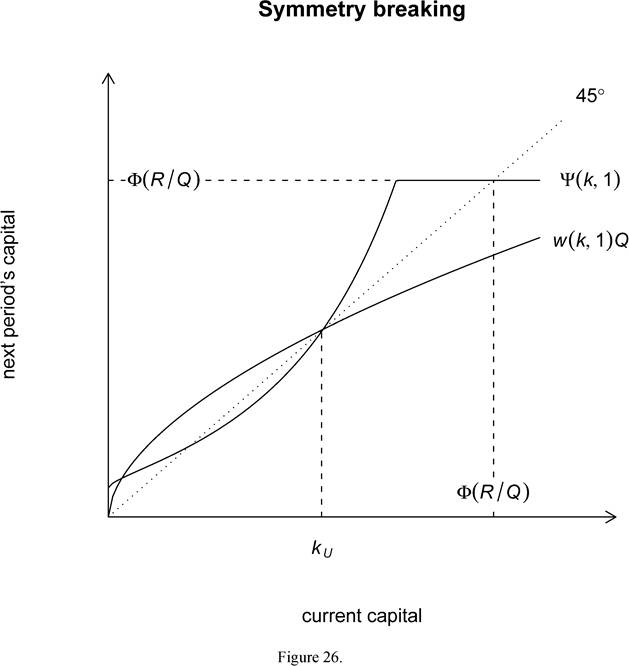

The story does not end here. What is particularly interesting about Matsuyama's study is his analysis of symmetry-breaking. He shows the following for a large range of parameter values: For a world economy consisting of a continuum of such countries, the deterministic steady state for autarky, which is k* defined by k* = w(k*, 1)Q, is precisely ku, the unstable steady state for each country under open international financial markets and a world interest rate that has adjusted to equate world savings and investment. Figure 26 illustrates the situation.

Thus, the symmetric steady state after liberalization, where each country has capital stock k*, is unstable and cannot be maintained under any perturbation. The reason is that countries which suffer from bad (resp., good) shocks are weakened (resp., strengthened)

in terms of their ability to guarantee returns on loans, and therefore to compete in the world financial market. This leads to a downward (resp. upward) spiral. Under these dynamics the world economy is polarized endogenously into rich and poor countries.

7.

More on the topic Credit markets, insurance and risk:

- Article 4.12 Asian credit markets expand at a record pace

- Modeling Credit Markets

- REAL-WORLD AND RISK-NEUTRAL EXPECTATIONS OF MARKETS

- CREDIT EXPOSURE SYSTEMIC RISK

- CREDIT EXPOSURE CONCENTRATION RISK

- USE AT DEFAULT

- Local Markets

- Voluntary Replication

- 10 Repairing and Insurance Obligations

- Contents