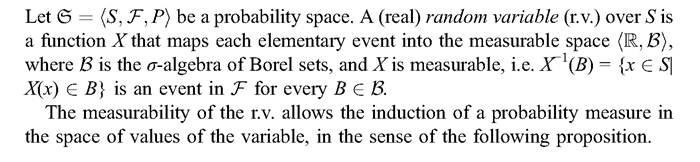

Random variables

A random variable over a probability space is a function that associates to every elementary event of the space a certain numerical result. If S is the set of all the

possible outcomes of throwing simultaneously two dice, an example of a random variable would be the function that assigns to each elementary event the payoff that turns out for the player if that event happens (provided that the function assigns the same payoff to all the different ways in which the event happens).

For instance, as we saw above, the event “seven turns out” is represented as

But the casino must pay the same amount to the player no matter how the event comes up, and so a random variable X representing the rule of paying an established amount m to seven must map every element of A into a number representing that amount of money: X(x) = m for every x 2 A. In general, in economic situations in which utility depends upon chance, it will turn out that the utility function is a random variable. This motivates the relevance of the following definition.

12.5.1 Definition

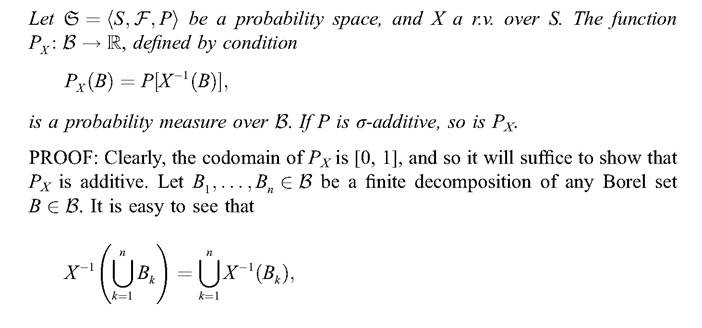

12.5.2 Theorem

fis called the probability density of F. There are examples of r.v.s that are continuous but lack a probability density. Nevertheless, econometric theory considers only those that do have it.

12.6