A richer model and the allocation of resources

The simple model given in the previous section provides several of the key insights of idea-based growth models, but it is too simple to provide others. In particular, the final implication in the basic Idea Diagram related to the problems a competitive equilibrium has in allocating resources has not been discussed.

In this section, we remedy this shortcoming and discuss explicitly several mechanisms for allocating resources in an economy in which ideas play a crucial role. In addition, we augment the simple model with the addition of physical capital, human capital, and the Dixit-Stiglitz love of variety approach that has proven to be quite useful in modeling growth.The model presented in this section is developed in a way that has become a de facto standard in macroeconomics. First, the economic environment - the collection of production technologies, resource constraints, and utility functions - is laid out. Any method of allocating resources is constrained by the economic environment. Next, we present several different ways in which resources can be allocated in this economy and derive results for each allocation. The first allocation is the simplest: a rule-of-thumb allocation analogous to the constant saving rate assumption of Solow (1956). The second allocation is the optimal one, i.e. the allocation that maximizes utility subject to the constraints imposed by the economic environment. These first two are very natural allocations to consider. One then immediately is led to ask the question of whether a decentralized equilibrium allocation, that is one in which markets allocate resources rather than a planner, can replicate the optimal allocation. In general, the answer to this question is that it depends on the nature of the institutions that govern the equilibrium. We will solve explicitly for one of these equilibrium allocations in Section 4.4 and then discuss several alternative institutions that might be used to allocate resources in this model.

4.1. Theeconomicenvironment

The economic environment for this new model consists of a set of production functions, a set of resource constraints, and preferences. These will be described in turn.

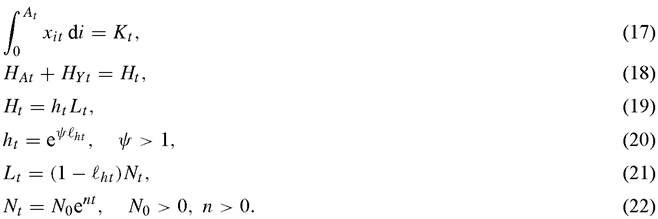

First, the basic production functions are these:

Equation (14) is the production function for the final output good. Final output Y is produced using human capital Hy and a collection of intermediate capital goods χi. A represents the measure of these intermediate goods that are available at any point in time. These intermediate goods enter the production function through a CES aggregator function, and the elasticity of substitution between intermediate goods is 1/(1 - θ ) > 1.

Notice that there are constant returns to scale in Hy and these intermediate goods in producing output for a given A. However, there are increasing returns to scale once A is treated as a variable. The sense in which this is true will be made precise below.

Equation (15) is a standard accumulation equation for physical capital.

Equation (16) is the production function for new ideas. In this economy, ideas have a very precise meaning - they represent new varieties of intermediate goods that can be used in the production of final output. New ideas are produced with a Cobb-Douglas function of human capital and the existing stock of knowledge.[12] * * As in the simple model, the parameter φ measures the way in which the current stock of knowledge affects the production of new ideas. It nets out the standing on shoulders effect and the fishing out effect. The parameter λ represents the elasticity of new idea production with respect to the number of researchers. A value of λ = 1 implies that doubling the number of researchers doubles the production of new ideas at a point in time for a given stock of knowledge. On the other hand, one imagines that doubling the number of researchers might less than double the number of new ideas because of duplication, suggesting λ < 1.

Next, the resource constraints for the economy are given by

Breaking slightly from my taxonomy, Equation (17) involves a production function as well as a resource constraint. In particular, one unit of raw capital can be transformed instantaneously into one unit of any intermediate good for which a design has been discovered. Equation (17) then is the resource constraint that says that the total quantity of intermediate goods produced cannot exceed the amount of raw capital in the economy.

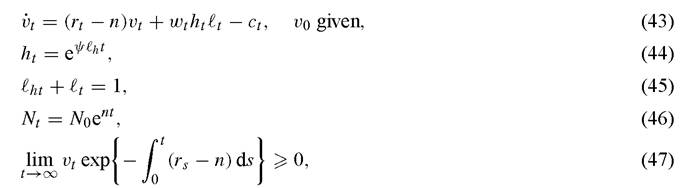

Equation (18) says that the amount of human capital used in the production of goods and ideas equals the total amount of human capital available in the economy. Equation (19) states the identity that this total quantity of human capital is equal to human capital per person h times the total labor force L (all labor is identical). An individual’s human capital is related by the Mincerian exponential to the amount of time spent accumulating human capital, lh, in Equation (20). We simplify the model by assuming there are no dynamics associated with human capital accumulation.10 Equation (21) defines the labor force to be the population multiplied by the amount of time that people are not accumulating human capital, and Equation (22) describes exogenous population growth at rate n.

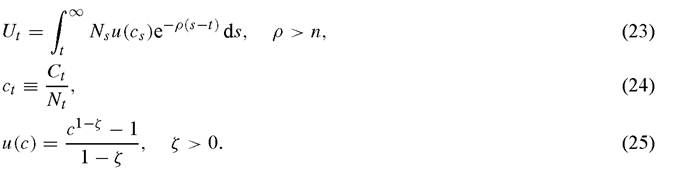

Finally, preferences in this economy take the usual form:11

4.2. Allocating resources with a rule of thumb

Given this economic environment, we can now consider various ways in which resources may be allocated. The primary allocative decisions that need to be made are relatively few. At each point in time, we need to determine the amount of time spent gaining human capital lh, the amount of consumption c, the amount of human capital allocated to research Ha, and the split of the raw capital into the various varieties ⅛}.

Once these allocative decisions have been made, the twelve equations in (14) to (25) above, combined with these four allocations pin down all of the quantities in the model.12The simplest way to begin allocating resources in just about any model is with a “rule of thumb”. That is, the modeler specifies some simple, exogenous rules for allocating resources. This is useful for a number of reasons. First, it forces us to be clear from

the beginning about exactly what allocation decisions need to be made. Second, it reveals how key endogenous variables depend on the allocations themselves. This is nice because the subsequent results will hold along a balanced growth path even if other mechanisms are used to allocated resources.

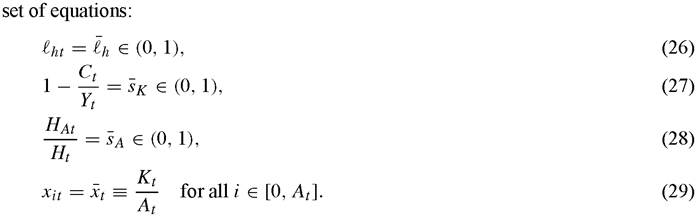

Definition 4.1. A rule of thumb allocation in this economy consists of the following

As is obvious from the definition, our rule of thumb allocation involves agents in the economy allocating a constant fraction of time to the accumulation of human capital, a constant fraction of output for investment in physical capital, a constant division of human capital into research, and allocating the raw capital symmetrically in the production of the intermediate capital goods.

With this allocation chosen, one can now in principle solve the model for all of the endogenous variables at each point in time. For our purposes, it will be enough to solve for a few key results along the balanced growth path of the economy, which is defined as follows:

Definition 4.2. A balanced growth path in this economy is a situation in which all variables grow at constant exponential rates (possibly zero) and in which this constant growth could continue forever.

The following notation will also prove useful in what follows. Let y ? Y/N denote final output per capita and let k ? K/N represent capital per person.

We will use an asterisk superscript to denote variables along a balanced growth path. And finally, gx will be used to denote the exponential growth rate of some variable x along a balanced growth path.With this notation, we can now provide a number of useful results for this model.

Result 1. With constant allocations of the form given above, this model yields the following results:

(a) Because of the symmetric use of intermediate capital goods, the production function for final output can be written as

(b) Along a balanced growth path, output per capita y depends on the total stock of ideas, as in

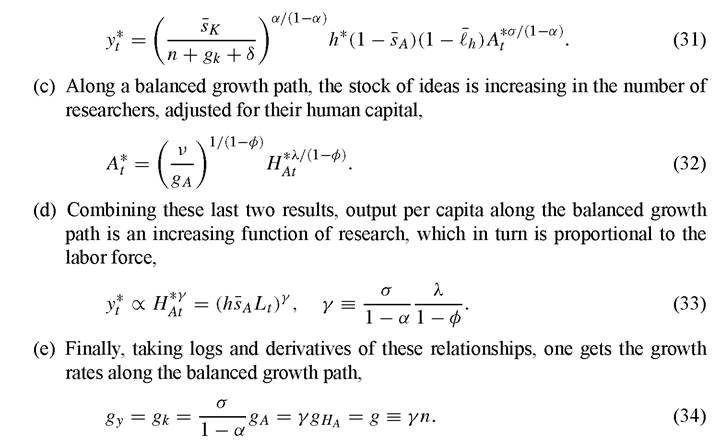

In general, these results show how the simple model given in the previous section extends when a much richer framework is considered. Result 1(a) shows that this Dixit- Stiglitz technology reduces to a familiar-looking production function when the various capital goods are used symmetrically. Result 1(b) derives the level of output per capita along a balanced growth path, obtaining a solution that is closely related to what one would find in a Solow model. The first term on the right-hand side is simply the capitaloutput ratio in steady state, the second term adjusts for human capital, the third term adjusts for the fraction of the labor force working to produce goods, and the fourth term adjusts for labor force participation. The final term shows, as in the simple model, that per capita output along a balanced growth path is proportional to the total stock of knowledge (raised to some power).

Result 1(c) provides the analogous expression for the other main production function in the model, the production of ideas. The stock of ideas along a balanced growth path is proportional to the level of the research input (labor adjusted for human capital), again raised to some power.

More researchers ultimately mean more ideas in the economy.Result 1(d) combines these last two expressions to show that per capita output is proportional to the level of research input, which, since human capital per worker is ultimately constant, means that per capita output is proportional to the size of the labor force.[13] The exponent γ essentially measures the total degree of increasing returns to scale in this economy. Notice that it depends on the parameters of both the goods production function and the idea production function, both of which may involve increasing returns.

Finally, Result 1(e) takes logs and derivatives of the relevant “levels” solutions to derive the growth rates of several variables. Output per worker and capital per worker both grow at the same rate. This rate is proportional to the growth rate of the stock of knowledge, which in turn is proportional to the growth rate of the effective level of research. The growth rate of research is ultimately pinned down by the growth rate of population. This last equality parallels the result in the simple model: the fundamental growth rate in the economy is a product of the degree of increasing returns and the rate of population growth. An interesting feature of this result is that the long-run growth rate does not depend on the allocations in this model. Notice that sA, for example, does not enter the expression for the long-run growth rate. Changes in the allocation of human capital to research have “level effects”, as shown in Result 1(b), but they do not affect the long-run growth rate. This aspect of the model will turn out to be a relatively robust prediction of a class of idea-based growth models.[14]

Pausing to consider the key equations that make up Result 1, the reader might naturally wonder about the restrictive link between the growth rate of human capital and the growth rate of the labor force that has been assumed. For example, in considering Result 1(d), one might accept that per capita output is proportional to research labor adjusted for its human capital, but wonder whether one can get more “action” on the growth side by letting human capital per researcher grow endogenously (in contrast, it is constant in this model).

The answer is that it depends on how one models human capital accumulation. There are many richer specifications of human capital accumulation that deliver results that ultimately resemble those in Result 1. One example is given in footnote 10. Another is given in Chapter 6 of Jones (2002a). In this latter example, an individual’s human capital represents the measure of ideas that the individual knows how to work with, which grows over time along a balanced growth path paralleling the growth in knowledge.

An example in which one gets endogenous growth in human capital per worker occurs when one specifies an accumulation equation that is linear in the stock of human capital itself h = βeψthh, reminiscent of Lucas (1988). For reasons discussed in Section 6.2, this approach is unsatisfactory, at least in my view.

4.3. The optimal allocation of resources

The next allocation we will consider is the optimal allocation. That is, we seek to solve for the allocation of resources that maximizes welfare. Because this model is based on a representative agent, this is a straightforward objective, and the optimal allocation is relatively easy to solve for.

Definition 4.3. The optimal allocation of resources in this economy consists of time paths {ct, lht, $At, {xit}}∞0 that maximize utility Ut at each point in time given the economic environment, i.e. given Equations (14)-(25), where sAt ? HAt/Ht.

This last equation incorporates the fact that because of symmetry, the optimal allocation of resources requires the capital goods to be employed in equal quantities.

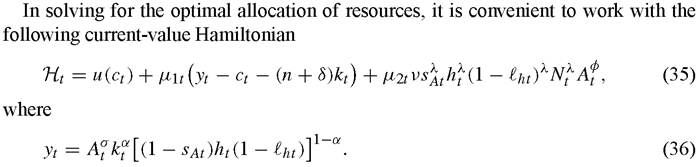

The current-value Hamiltonian Ht reflects the utility value of what gets produced at time t: the consumption, the net investment, and the new ideas. As suggested by Weitzman (1976), it is the utility equivalent of net domestic product. The necessary first-order conditions for an optimal allocation can then be written as a set of three control conditions ∂Ht /∂mt = 0, where m is a placeholder for c, sA and lh and two arbitrage-like equations

Result 2. In this economy with the optimal allocation of resources, we have the following results:

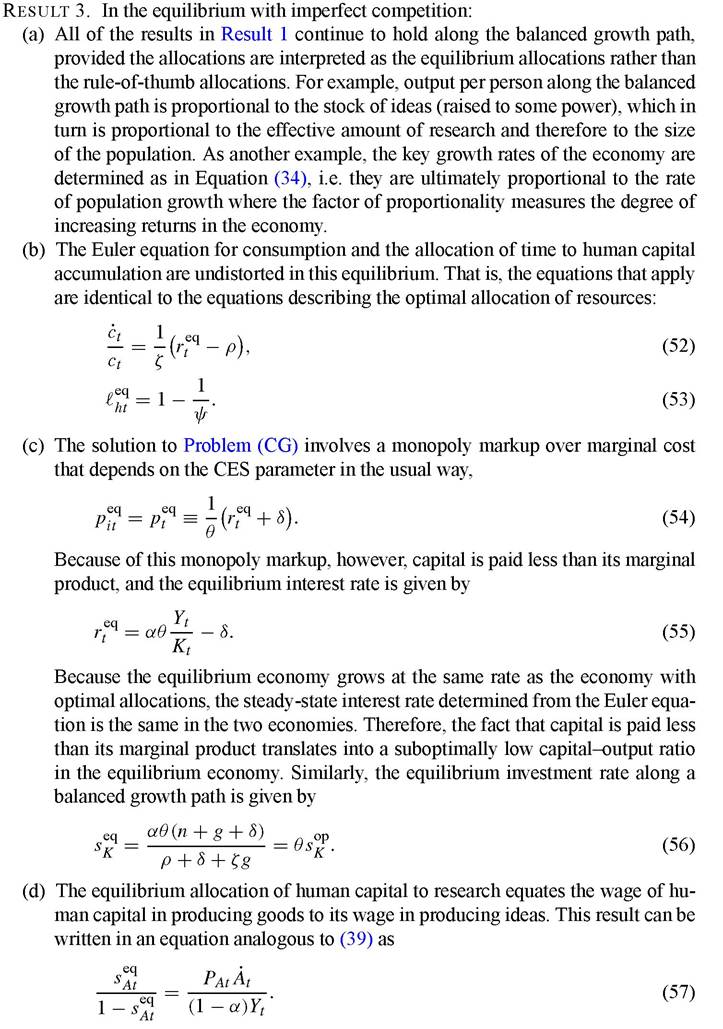

(a) All of the results in Result 1 continue to hold, provided the allocations are interpreted as the optimal allocations rather than the rule-of-thumb allocations. For example, output per person along the balanced growth path is proportional to the stock of ideas (raised to some power), which in turn is proportional to the effective amount of research and therefore to the size of the population. As another example, the key growth rates of the economy are determined as in Equation (34),

i. e. they are ultimately proportional to the rate of population growth where the factor of proportionality measures the degree of increasing returns in the economy.

(b) The optimal allocation of consumption satisfies the standard Euler equation

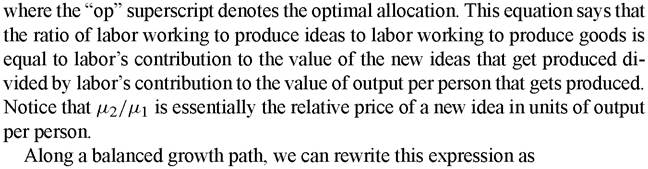

(c) The optimal allocation of labor to research equates the value of the marginal product of labor in producing goods to the value of the marginal product of labor in producing new ideas. One way of writing this equation is

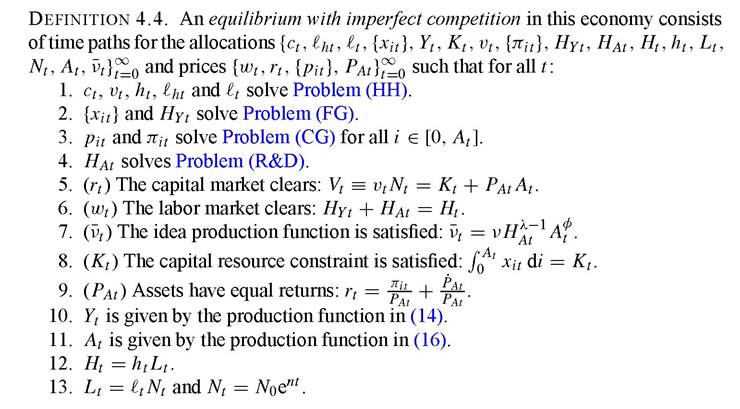

4.4. A Romer-style equilibrium with imperfect competition

A natural question to ask at this point is whether some kind of market equilibrium can reproduce the optimal allocation of resources. The discussion at the beginning of this chapter made clear the kind of problems that an equilibrium allocation will have to face: the economy is characterized by increasing returns and therefore a standard competitive equilibrium will generally not exist and will certainly not generate the optimal allocation of resources. We are forced to depart from a perfectly competitive economy with no externalities, and therefore one will not be surprised to learn in this section that the equilibrium economy, in the absence of some kind of policy intervention, does not generally reproduce the optimal allocation of resources.

In this section, we study the equilibrium with imperfect competition first described for a model like this by Romer (1990). Romer built on the analysis by Ethier (1982), who extended the consumer variety approach to imperfect competition of Spence (1976) and Dixit and Stiglitz (1977) to the production side of the economy. The economic environment (potentially) involves departures from constant returns in two places, the production function for the consumption-output good and the production function for ideas. We deal with these departures by introducing imperfect competition for the former and externalities for the latter.

Briefly, the economy consists of three sectors. A final goods sector produces the consumption-capital-output good using labor and a collection of capital goods. The capital goods sector produces a variety of different capital goods using ideas and raw capital. Finally, the research sector employs human capital in order to produce new ideas, which in this model are represented by new kinds of capital goods. The final goods sector and the research sector are perfectly competitive and characterized by free entry, while the capital goods sector is the place where imperfect competition is introduced. When a new design for a capital good is discovered, the design is awarded an infinitely-lived patent. The owner of the patent has the exclusive right to produce and sell the particular capital good and therefore acts as a monopolist in competition with the producers of other kinds of capital goods. The monopoly profits that flow to this producer ultimately constitute the compensation to the researchers who discovered the new design in the first place.

As is usually the case, defining the equilibrium allocation of resources in a growth model is more complicated than defining the optimal allocation of resources (if for no other reason than that we have to specify markets and prices). We will begin by stating the key decision problems that have to be solved by the various agents in the economy and then we will put these together in our formal definition of equilibrium.

Problem (HH). Households solve a standard optimization problem, choosing a time path of consumption and an allocation of time. That is, taking the time path of {wt, rt} as given, they solve

subject to

where vt is the financial wealth of an individual, wt is the wage rate per unit of human capital, and rt is the interest rate.

Problem (FG). A perfectly competitive final goods sector takes the variety of capital goods in existence as given and uses the production technology in Equation (14) to produce output. That is, at each point in time t, taking the wage rate wt, the measure of capital goods At, and the prices of the capital goods pit as given, the representative firm solves

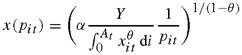

Problem (CG). Each variety of capital good is produced by a monopolist who owns a patent for the good, purchased at a one-time price PAt. As discussed in describing the economic environment, one unit of the capital good can be produced with one unit of raw capital. The monopolist sees a downward-sloping demand curve for her product from the final goods sector and chooses a price to maximize profits. That is, at each point in time and for each capital good i, a monopolist solves

where χ(pit ) is the demand from the final goods sector for intermediate good i if the price is pit. This demand curve comes from a first-order condition in Problem (FG). The monopoly profits are the revenue from sales of the capital goods less the cost of the capital need to produce the capital goods (including depreciation). The monopolist is small relative to the economy and therefore takes aggregate variables and the interest rate rt as given.15

15 To be more specific, the demand curve x(pi) is given by

We assume the monopolist is small relative to the aggregate so that it takes the price elasticity to be -1/(1 -θ).

Problem (R&D). The research sector produces ideas according to the production function in Equation (16). However, each individual researcher is small and takes the productivity of the idea production function as given. In particular, each researcher assumes that the idea production function is

That is, the duplication effects associated with λ and the knowledge spillovers associated with φ in Equation (16) are assumed to be external to the individual researcher. In this perfectly competitive research sector, the representative research firm solves

taking the price of ideas PAt, research productivity νt, and the wage rate wt as given.

Now that these decision problems have been described, we are ready to define an equilibrium with imperfect competition for this economy.

Notice that, roughly speaking, there are twenty equilibrium objects that are part of the definition of equilibrium and there are twenty equations described in the conditions for equilibrium that determine these objects at each point in time.16 Not surprisingly, one cannot solve in general for the equilibrium outside of the balanced growth path, but along a balanced growth path the solution is relatively straightforward, and we have the following results.

The ratio of the share of human capital working to produce ideas to that working to produce goods is equal to the value of the output of new ideas divided by labor’s share of the value of final goods.

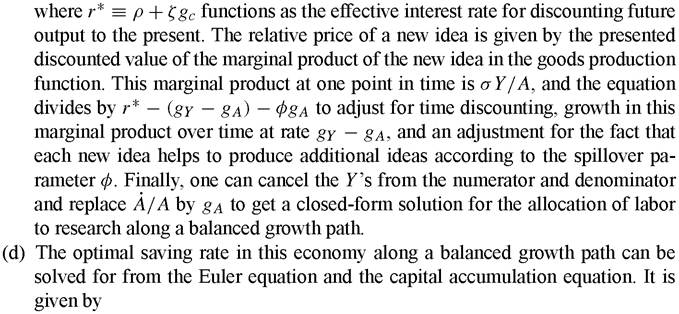

Along the balanced growth path, we can rewrite this expression as

which is directly comparable to the optimal allocation in Equation (40). In comparing these two equations, we see three differences. The first two differences reflect the externalities in the idea production function. The true marginal product of human capital in research is lower by a factor of λ < 1 than the equilibrium economy recognizes because of the congestion/duplication externality, which tends to lead the equilibrium to overinvest in research. On the other hand, the equilibrium allocation ignores the fact that the discovery of new ideas may raise the future productivity of research if φ > 0. This changes the effective rate at which the flow of future ideas is discounted, potentially causing the equilibrium to underinvest in research. Finally, the third difference reflects the appropriability of returns. A new idea raises the current level of output in the final goods sector according to the marginal product σY∕A. However, the research sector appropriates only the fraction θ < 1 of this marginal product. The reason is familiar from the standard monopoly diagram in undergraduate classes: the profits appropriated by a monopolist are strictly lower than the consumer surplus created by that monopolist. This appropriability effect works to cause the equilibrium allocation of human capital to research to be too low. Overall, these three distortions do not all work in the same direction, so that theory cannot tell us whether the equilibrium allocation to research is too high or too low.

4.5. Discussion

Let us step back for a moment to take stock of what we learn from the developments in this section. The most important finding is Result 1, together with the fact that it carries over into the other allocations as Result 2(a) and Result 3(a). This result is simply a confirmation of the basic results from the simple model in Section 3. Because of the nonrivalrous nature of ideas, output per person depends on the total stock of ideas in the economy instead of the per capita stock of ideas. This is a direct implication of the fact that nonrivalry leads to increasing returns to scale. In turn, it implies that output per capita, in the long run, is an increasing function of the total amount of research, which in turn is an increasing function of the scale of the economy, measured by the size of its total population. Log-differencing this statement, we see that the growth rate of output per worker ultimately depends on the growth rate of the number of researchers and therefore on the growth rate of population. This has been analyzed and discussed extensively in a number of recent papers; these will be reviewed in detail in Section 5.

The second main finding from models like this is that the equilibrium allocation of resources is not generally optimal, at least not in the absence of some kind of policy intervention. Here, the allocation of resources to the production of new ideas can be either too high or too low, as discussed above.[17] In addition, investment rates are too low in equilibrium, reflecting the fact that capital is paid less than its marginal product so that some resources are available to compensate inventive effort.

In this equilibrium, the suboptimal allocation of resources is easily remedied. A subsidy to capital accumulation and a subsidy or tax on research can be financed with lump sum taxes in order to generate the optimal allocation of resources. A useful exercise is to solve for the equilibrium in the presence of such taxes in order to determine the optimal tax rates along a balanced growth path.

Given the simplicity of this economic environment, there exist alternative institutions that are equally effective in getting optimal allocations. For example, consider a perfectly competitive economy in which all research is publicly-funded. The government raises revenue with lump-sum taxes and uses these taxes to hire researchers that produce new ideas. These new ideas are then released into the public domain where anyone can use them to produce capital goods in perfect competition.[18]

In practice of course, one suspects that obtaining the optimal allocation of resources is more difficult than either the world of imperfect competition with taxes and subsidies or the perfectly-competitive world with public funding of research suggest. There are many different directions for research, many different kinds of labor (different skill levels and talents), and individual effort choices that are unobserved by the government. Indeed, the available evidence suggests that the allocation of resources to research falls short of the optimal level. Jones and Williams (1998) take advantage of a large body of empirical work in the productivity literature to conclude that the social rate of return to research substantially exceeds the private rate of return, suggesting that research effort falls short of the optimum.

The implication of this is that there is no reason to think that we have found the best institutions for generating the optimal allocation of resources to research. Institutions like the patent system or the Small Business Innovative Research (SBIR) grants program are themselves ideas. These institutions have evolved over time to promote an efficient allocation of resources, but it is almost surely the case that better institutions - better ideas - are out there to be discovered.

Interestingly, this result can be illustrated within the model itself. Notice how much easier it is to define the optimal allocation than it is to define the equilibrium allocation. The equilibrium with imperfect competition requires the modeler to be “clever” and to come up with the right institutions (e.g., a patent system, monopolistic competition, and the appropriate taxes and subsidies) to make everything work out. In reality, society must invent and implement these institutions.

Three recent papers deserve mention in this context. Romer (2000) argues that subsidizing the key input into the production of ideas - human capital in the form of college graduates with degrees in engineering and the natural sciences - is preferable to government subsidies downstream like the SBIR program. Kremer (1998) notes the large ex-post monopoly distortions associated with patents in the pharmaceutical industry and elsewhere and proposes a new mechanism for encouraging innovation. In particular, he suggests that the government (or other altruistic organizations such as charitable foundations) should consider purchasing the patents for particular innovations and releasing them into the public domain to eliminate the monopoly distortion. Boldrin and Levine (2002), in a controversial paper, are even more critical of existing patent and copyright systems and propose restricting them severely or even eliminating them altogether.[19] They argue that first-mover advantages, secrecy, and imitation delays provide ample protection for innovators and that an economy without patent and copyright systems would have a better allocation of resources than the current regime in which copyright protection is essentially indefinite and patents are used as a weapon to discourage innovation. Each of these papers makes a useful contribution by attempting to create new institutions that might improve the allocation of resources.

5.