A Stealth Market

In the last century, the idea of the invisible hand was repeated too often. The idea emerged of the market becoming transparent i.e., visible to all participants. However, the real market is never transparent.

As the power law works, the environment is undergoing modifications everywhere. Instead of the traditional equilibrium price, equilibrium may be regarded as convergence towards a stable distribution like the Pareto-Levy distribution. This is a decisive difference between traditional economics and econophysics.5.2.1 The Invisible Organization of Finance

There are some decisive institutional settings in the stealth market. The securitization of property rights including loans is a system of reassurance, which in itself is an old technique dating back to feudal times. It may be virtually a debt bond swap, making the system even more complex. The financial commodities issued initially by investment partnerships are invisible to the general public. Financial intermediation thus becomes deeper and more complex. We therefore introduce some basic ideas from complex science, such as logical depth, to support analysis.

5.2.1.1 Devastating Financial Forces Equivalent to Large Earthquakes

The similarities between financial crises and large earthquakes are often discussed, and there are even some econophysicists who were formerly seismologists. For example, the sources or causes are seldom fully explored. The widespread nature of the effects are often unseen. The same frequencies and magnitudes do not necessarily cause the same effects. The initial shock is sometimes accompanied by a second disaster. Aseismic measures are required. Both earthquakes and financial crises are often seen as very difficult to predict in both size and location. In recent crises, the expansion of the shadow banking system (SBS) is seen as significant (Issing et al.

2012). The investment partnership issuing the debt bond swap at the initial stage will unilaterally dominate the information around its reassurance. The regulator can favor a particular group or type of investors. These effects are in many cases achieved behind the scenes, so that the public do not know about the risks around these financial commodities.5.2.1.2 Risk Management of the Classical Futures Market

In the classical financial market, double-check management in the futures market is always assured by two rules:

Mark to the market: The sessions accumulate the position until the end of the day.

The mark to the market settles the balances between participants every night as if the day looked like the final contract.

Margin requirement: The futures exchange institution must act as intermediary and minimize the risk of default by either party. The exchange therefore requires both parties to put up an initial amount of cash, the margin or margin call.

These rules were fully implemented in the Japanese futures market from its inception in 1730. However, the options market did not impose the rule of “mark to the market”, and therefore lost sight of the current positions of a whole market. The option may be regarded as a secondary construction. The sell and buy of “Call” in the option trade assumes the short position. On the other hand, the sell and buy of “Put” does the long position. However, this system cannot work well without any normal operation of the futures market. The crash of the tulip bubble in the Netherlands was a failure of the options market. To complement the lack of the mark to the market, computer risk management was added from the 1970s in the US.

5.2.1.3 Massive Sell Orders from Erroneous Human Operations

Before HFT became dominant, the market experienced several cases of erroneous human operations. There were two particularly famous cases in Japan.[58]

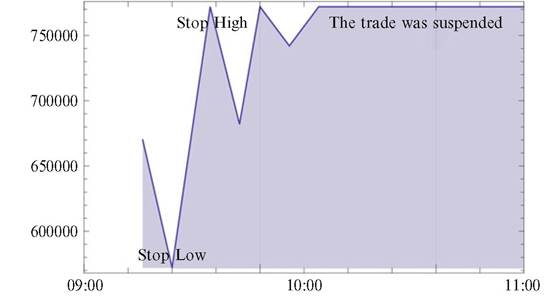

Dentsu in 2001: During the initial public offering of advertising giant Dentsu, in December 2001 a trader at UBS Warburg, the Swiss investment bank, sent an order to sell 610,000 shares in this company at ¥ 1 each, when he intended to sell one share at ¥610,000.

The bank lost £71 million.J-COM in 2005: During the initial public offering of J-COM, on December 8,2005, an employee at Mizuho Securities Co., Ltd. mistakenly typed an order to sell 600,000 shares at ¥ 1, instead of an order to sell one share at ¥600,000. Mizuho failed to catch the error; the Tokyo Stock Exchange initially blocked attempts to cancel the order, resulting in a net loss of US $347 million shared between the exchange and Mizuho.[59]

At the aftermath of the J-COM case, both companies undertook to try to deal with their troubles: lack of error checking, safeguards, reliability, transparency, testing, and loss of both confidence and profit. On December 11, 2005, the Tokyo Stock Exchange acknowledged that its system was at fault in the Mizuho trade.[60]

Collapses may happen in spite of renovations. In a traditional auction, cancelation is essential for efficient transactions. In high-frequency trades, however,

Fig. 5.9 The price fluctuations of J-COM stock. Note: The initial opening price was ¥670,000. The vertical axis is measured in Japanese Yen

cancelation will be limited to algorithm agents and given a special strategic role. As the market structure becomes more hierarchical, we must look again at the conventional definitions of trade tools. The rule of stop high and stop low will no longer exercise the same control of the range of price movements. In millisecond transactions, a traditional guideline cannot work effectively, and it will be difficult to prevent flash crashes. New trade tools must be developed to re-domain the market (Fig. 5.9).

The gigantic expansion of the market in size and complexity is closely connected with the evolution of algorithmic transactions and the speeding-up of both processing and order strategies, i.e., the creation of an artificial intelligence-dominant economy. This evolution has resulted in some hidden and unmeasurable destructive power in the invisible market, quite similar to large earthquakes.

This is particularly observed as a rapid development of SBSs. In these situations, humans must co-evolve with artificial intelligence, otherwise they will be dominated by it.5.2.1.4 Implementation of Relaxed Static Stability in the Financial Market

Shadow Computer control made possible a new generation of military aircraft designed to be inherently unstable, i.e., in technology jargon, to have relaxed static stability. This gave an advantage. Just as you can maneuver an unstable bicycle more easily than a stable tricycle, you can maneuver an inherently unstable aircraft more easily than a stable one. The new controls act to stabilize the aircraft much as a cyclist stabilizes a bicycle by offsetting its instabilities with countering motions. A human pilot could not react quickly enough to do this; under the earlier manual technology, an inherently unstable aircraft would be unflyable (Arthur 2009, p. 73).

5.3