The previous chapter described a world where a financial accelerator first generates a lending driven boom and then its inevitable collapse.

But that collapse contains within itself the seeds of a new boom; and so the economy continues, bouncing from boom to crisis and back.

The evidence, described in the previous chapter, from GVL (2001), is primarily about what happens when a lending boom collapses.

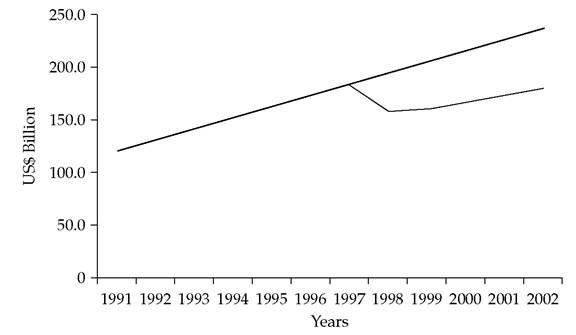

As we saw it fits well with what happens in our model. It does not however say very much about the recovery; in particular they have nothing to say about whether the economy actually bounces back all the way. The concern that this may not always be the case comes from the finding, reported in GVL (2001) that lending booms tend to increase the probability of a currency crisis,[16] combined with the evidence that after currency crises countries do not go back to the pre-crisis trend. Figure 5.1, taken from Griffith- Jones (2004) illustrates this point for the case of Indonesia. By extrapolating the preexisting trend in GDP and comparing with post-crisis outcomes, Griffith-Jones estimates that between 1995 and 2002 (admittedly a period when crises where both very damaging and very frequent), the annual cost of crises for Argentina, Brazil, Indonesia, Korea, Malaysia, Mexico, Thailand, and Turkey combined reached the very large estimated amount of US$ 150 billion (in 2002 US$). Eichengreen (2004) looks at a longer period and estimates the cost of currency crises at 0.7% of developing country emerging market GDP per year, equivalent to an annual amount of US$ 107 billion, or to put it differently, over the last quarter century, currency and banking crises have reduced incomes of developing countries by around 25%.

Fig. 5.1 Indonesia: potential and actual GDP.

Note: Projected output for the years 1997-2002 based on output trend over the 1991-6 period. Values are in US$ 1989 billion.

Data source: World Bank data base.Source: Griffith-Jones (2004), figure 1.

In this chapter we present a highly stylized model, based, as in previous chapters, on limited access to credit,* [17] that can explain why an economy that is carrying a large amount of foreign currency debt might be vulnerable to currency crises, which leave it with a depreciated currency and GDP that remains lower than the pre-crisis trend for some time into the future. We are about to argue that, in a monetary economy with standard price rigidities, credit constraints together with pecuniary externalities working through the nominal exchange rate are sufficient to generate currency crises.

There is, of course, a long tradition of models aimed at helping us understand currency crises. Thus, a first generation of models[18] took the view that currency crises resulted from large budget deficits. While this explanation could fit the case of Latin American countries in the 1980s, it can hardly account for why currency crises occurred in East and South-east Asia in the late 1990s, since governments in this region were all running budget surpluses. A second generation[19] attributes the occurrence of currency crises to credibility problems faced by governments with the conflicting objectives of maintaining a fixed exchange rate parity and reducing unemployment. While this could explain the collapse of the European Monetary System in the early 1990s, the unemployment rates in the Asian economies of the 1990s were among the lowest in the world, and it is hard to believe that reducing unemployment was a priority for these governments. Our view of the crisis falls into the class of “third generation"theories: These are theories which locate the proximate source of the crisis in the private sector rather than in the government.[20]

The basic mechanism that generates crises is simply summarized as follows: if nominal prices are rigid in the short run, a currency depreciation leads to an increase in the foreign currency debt repayment obligations of firms.

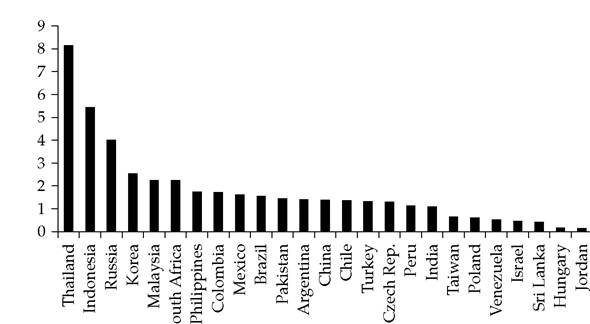

In a setting where the firm sector has a large outstanding foreign debt, for example because of a lending boom in the preceding few years, this can have a very substantial impact on profits and the net worth of the firm sector.[21] This in turn limits the firms' ability to borrow and therefore may result in less investment and lower output in the next period. The resulting fall in the demand for money will cause the currency to depreciate in the next period. But arbitrage in the foreign exchange market then implies that the currency must depreciate in the current period as well. In other words, if people believe that the currency will depreciate, it may indeed depreciate. In other words, when the firm sector is carrying a large amount of foreign currency debt, there are multiple short-run equilibria in the market for foreign exchange. What we call currency crises are shifts between "good" equilibria and "bad" equilibria, triggered by a change in expectations or a real shock to the economy.This story of currency crises has the significant advantage that it is based on two well-known facts: first, the countries most likely to go into a crisis were those in which firms held a lot of foreign currency denominated debt. For example, Figure 5.2 shows the ratio of claims to liabilities with respect to BIS banks; since these transactions are mostly in foreign currency, this ratio is a measure of aggregate foreign currency exposure. It is striking that all the countries that had a ratio higher than 1.5 have experienced a serious crisis in the 1990s. In the next section, we discuss possible rationales for firms to hold foreign currency debt.

The second fact is that there are substantial and persistent deviations from purchasing power parity following an exchange rate shock: Engel (1993) decribes this evidence in some detail. In a recent important paper Burstein et al. (2004) have shown that in the case of large devaluations, this is mainly driven by the

Fig.

5.2 Ratio of liabilities to claims with respect to foreign banks 1997. Source: Aghion et al. (2001), figure 1.94 The Third Generation Approach to Currency Crises nonadjustment of the prices of nontradables; this filters into the price of tradables in part because of distribution costs and in part because people move to cheaper, less traded, goods.[22]

This means that for our story to go through, the firms producing nontraded goods must be carrying foreign currency debt. The same evidence shows that a very large part of GDP is effectively nontraded which makes this more likely. For example, there is no reason why foreign currency debt is more likely to be held by a firm that produces a tradable, than by the firm that builds or owns warehouses that store the tradable good. While there are many very small firms in the nontraded sector, there are also many very large firms, especially in construction and distribution.

Our credit-based approach to currency crises also has the advantage of being consistent with the observation that countries with less developed financial systems are more likely to experience an output decline during a crisis.[23] Second, it makes it clear why a currency crisis can also happen under a flexible exchange rate or without any significant decline in foreign exchange reserves. Third, crises may occur even in countries that are conventionally well-behaved, in the sense of having low unemployment rates and conservative fiscal and monetray policies.

It still remains that public policy variables such as fiscal deficits, influence whether a currency crisis occurs, as stressed by the existing literature on the subject. However, in contrast to first- and second generation models, in the world described in this chapter a deterioration of fiscal balances will lead to a crisis mainly through its impact on private firms' balance sheets rather than through simple money demand adjustments as in the previous models.[24] Moreover, the presence of public sector debt may exacerbate the problems of private sector debt, especially if a large fraction of public sector debt is in foreign currency.

This result is insharp contrast with the previous literature that argues that foreign currency (public) debt should have a stabilizing effect.

Another advantage of our model is that it lends itself very naturally to the analysis of monetary policy. There has been an important debate on the stance of monetary policy in the context of currency crises; one side in this debate emphasizes the importance of past government failures and advocates monetary tightening, in part to signal the government's commitment to restraint.[25] [26] The other side blames shifts in expectations and bad luck (the multiple equilibrium view) and sees no reason why we should punish the already battered firm sector even more by tightening monetary policy.11 Strikingly, though our model is of the multiple equilibrium kind, as long as the credit multiplier only depends on real interest rates and prices adjust relatively quickly, a restrictive monetary policy is the optimal response to the risk of a currency crisis. This is because the shift in exchange rates generated by tightening remains the best way to help the beleagured firm sector. However, we also show that this conclusion may cease to hold when credit supply is affected by the nominal interest rate and/or when price adjustment takes longer than it takes to discharge the inherited debt obligations of the firm sector. The rest of the chapter is organized as follows. Section 5.1 lays out the basic model. Section 5.2 shows that this model naturally gives itself to graphical analysis. Using this graphical apparatus we examine the occurrence of currency crises and demonstrate the possibility of multiple equilibria. Section 5.3 analyzes the policy implications of the model, and Section 5.4 concludes. 5.1